Update on new organizational structure and strategic initiatives

The company has announced major organizational and strategic initiatives during the quarter.

Happiest Minds has incorporated a new segment that is Generative AI business units (GBS) to

capitalize on the transformative impact of Gen AI.

Additionally, the existing Product Engineering Services (PES) and Digital business solution (DBS) segments will be combined into PDES business unit and there will be no change in Infrastructure Management and Security Services (IMSS). Going ahead, the company will have 3 business units: GBS, PDES and IMSS. The company continues to make progress in Gen AI and engaging with multiple customers for their transformation and enhancing efficiency.

Overview: Happiest Minds Technologies Limited, a ‘Born Digital . Born Agile’ IT company, proudly announces its inclusion in the 100 Best Companies for Women in India (BCWI) list released by Avtar and Seramount. This recognition reflects the company’s commitment to equity and inclusion in the workplace.

Press Release Highlights:

1. Recognition Details:

Awarded by Avtar and Seramount based on the BCWI study.

Happiest Minds secured a position in the 100 Best Companies for Women in India list.

2. Selection Criteria:

Companies with high-order granularity on diversity representation.

Recognition for programs and policies ensuring gender inclusion at the workplace.

3. Statement from Happiest Minds:

Joseph Anantharaju, Executive Vice Chairman, expresses ecstasy and emphasizes the importance of embracing diversity and fostering inclusion.

The ‘Happiest Minds Diversity Council’ focuses on building and sustaining a strong, diverse, equitable & inclusive culture.

4. Commitment to Diversity and Inclusion:

Sachin Khurana, Senior Vice President & Chief People Officer, highlights celebrating diversity and inclusion as a fundamental value enriching the workplace.

Recognition seen as a testament to the commitment to creating a more inclusive future.

5. Efforts in Diversity-Focused Hiring:

Mention of diversity-focused hiring drives for candidates like women on a long break and People with Special Abilities.

Recognition not just as an award but as a fundamental value.

6. Recognition History:

Happiest Minds has received multiple recognitions, including Top 100 India’s Best Companies to Work for 2023, Best Workplaces in Asia™ 2022, Top 50 India’s Best Workplaces™ for Women 2021 and 2022, India’s Best Companies to Work for 2021 and 2022, and more.

Proof of ceaseless efforts in creating a culture of happiness, wellness, and inclusivity.

Happiest Mind have fallen to a PE multiple of 47 because of the IT sector correction. With the revenue guidance of 12% growth per year and IT sector headwinds, what does the group here thinks about it’s valuations?

12% growth is just organic growth guidance, with a lot of cash on it’s book, they would go for acquisition as well which would have a multiplier effect on there growth guidance. One of the positive things about this headwind in IT sector is they could get cheap valuations for acquisition which would play out well for Happiest Mind in the long term.

Posting my detailed analysis for the first time, would love to hear thoughts/feedback from this group about my views.

Q2 FY 2024 and Q3 FY 2024 Notes:

Happiest Mind changed the outlook for the year from 25% to 12%. Interesting thing is they have mentioned 12% as the organic growth only and they are having weekly/bi-weekly discussions about acquisitions with list of candidates. So, if any acquisition happens, it will add on to the revenue growth, however, for FY2024, even if the acquisition happens tomorrow, there wouldn’t be any substantial revenue addition for FY2024, so 12% growth should be the guidance.

Created a new vertical called Gen AI Business Unit (GBS) which would take advantage of the current AI boom that IT industry is seeing. Currently, in talks with multiple clients for AI use cases in their respective company. No targets for revenue has been set for this vertical for current year, this should start picking up in next financial year, so they will report numbers from thei vertical from next financial year.

Due to delay in interest rate cut by Feds and high inflation scenario, there clients are cautious while spending money and are taking time in making decisions.

In order to meet 12% growth guidance for this year, they still need to have a good next quarter and they are confident they should be able to do it.

After the creation os new Business Unit, they have 3 divisions now. TBD: Revenue from all 3 divisions?

Product and Digital Engineering Services (PDES)

Infrastructure & Management Security Services.

Generative AI Business Unit (GBS)

Whenever the industry goes back to normal, they are greatly poised to take advantage of it.

Happiest Mind have still increased there headcount even after this uncertainity, they got around ~230 college hires and also gave pay hikes to there employees when some of the other Indian IT companies have not done that.

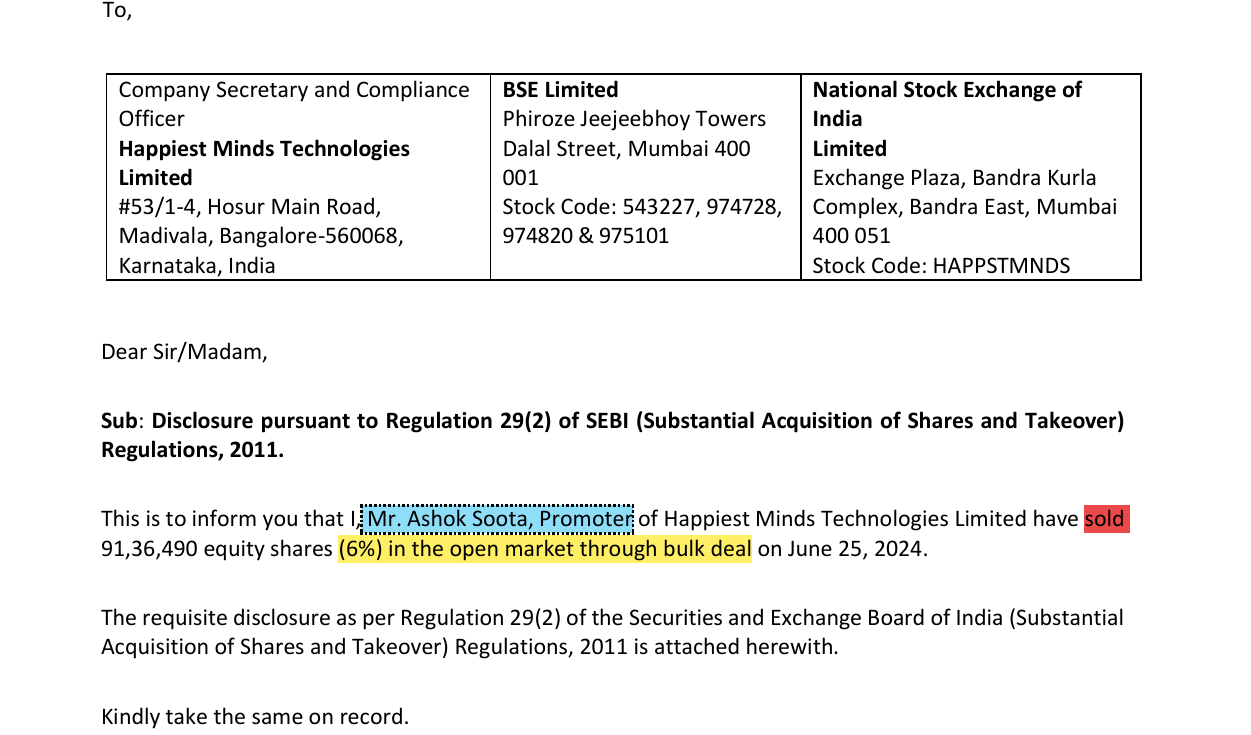

Ashok Soota has sold a small amount of stake to fund his charitable organization.

They are still confident about there margin guidance of 22%-24%.

They will be hiring sales head for US to boost sales growth from US.

In order to understand more about the demand outlook for Happiest Mind, I looked at EPAM earnings call and this is what EPAM CEO said. “Because of our ability to adapt to new client demands and market conditions, we are optimistic about the opportunities ahead of us toward the end of 2024. Demand to build postponed during the last two years should rebound, driven by long-term pressures for legacy modernizations, by needs for advanced customer-centric solutions, and by the massive interest to understand how to apply GenAI and general AI capabilities to build new platforms and solutions”

He expects the demand outlook to return to 2022 levels by H2 2024.

My viewpoints for Happiest Mind:

Happiest Mind revenue will struggle for atleast next couple of quarters due to demand outlook, however, demand should rebound in late 2024 or early 2025 because of the factors that EPAM CEO mentioned as well as Fed interest rate cuts which should be on the cards.

Ashok Soota has already seen these circumstances a lot in his career during dot com bubble, 2008 crash, etc, so he knows how to recover from it. His guidance would be helpful for the management.

I expect the future growth to come from GBS unit which most of the companies are looking to adopt. It is not new for Happiest Mind to work on new technologies since they adopted IoT technology much early in Indian IT space in 2015, so I expect them to grow substantially on this space.

PE ratio of 46 does not make sense for a company with 12% growth outlook and future outlook being unknown. So, valuation becomes a key to get long term profit here.

Happiest Mind management in one of the interviews was confident about 25% growth outlook even after EPAM cuts its growth guidance, however, in next quarter concall, they slashed the revenue guidance. So this tells me the management does not have visibility for atleast couple of quarters. However, I got the same feeling when I heard EPAM earnings call, so it seems like all the industry participants does not have visibility for next couple of quarters.

Conclusion:

With good management running the show and they working on newer technologies like Gen AI, it seems they are rightly placed to gain market share in digitization and GBS unit which should boost there revenues once demand outlook stabilizes. However, PE of 46 is a bit high for long term entry position. EPAM has a PE of ~30 but with there high base they might not be able to grow as rapidly as Happiest Mind. What does thie group think the right valuation is for Happiest Mind?

Disc: Have a small tracking position in Happiest Mind but want to add more at right levels.

Revenue growth of PureSoftware is strong, last year they closed at $45 million. (351 cr topline last year on consolidated basis. )

This acquisition will be EPS accretive from Day 1.

Margins are not given yet for PureSoftware but it’s a reasonable good margin and healthy business. Long standing margins guidance 22-24% still intact with this acquisition. There is room for further margin improvements with efficiencies that will come with integration in next 3-4 quarters.

BFSI and Healthcare → 50% comes from both of it. Addition 1200 employees.

Focus is to keep growing not at cost of profitability.

144 crores is still deferred based on them achieving certain revenue and margin targets by end of 2024.

Happiest Mind has a USD 200 million dollar revenue currently, with this acquisition, top line would be increased by USD 245 million and BFSI and Healthcare would increase to USD 52.5 million for both.

Post this acquisition 600 crores would be left on book.

Any reason for this selling? I remember at the time or IPO Ashok Soota sir had said that he wants to retain 51% or the company to retain the ownership and avoid any hostile takeover that happened with Mindtree.

Ashok Soota has sold due to his other commitments like NGO and Happiest Health, his target is to drop his holding to 40% after which he wouldn’t sell, currently he is at ~44%. Expect some more selling maybe in coming years, but the guy deserves it. Nothing wrong with the company.

I think the results are aleady factored in the stock price, as its quite beaten up already, but definitely good RR.

Challenges: Dollar weakning as FED cuts interest rate. margin will have a little impact.

But I see more upside if they are correectly able to ride this AI wave.

What happens after Mr Soota, passes. It is a tough and sad question to ask but very important regarding the future aspects of the company. What happens to 40% if it goes to a trust. There aren’t many promoter less companies that we know of that work well in India. In Us it is common practice but here without a promoter it is generally like a ship without a captain. Except L&T I do not know of any spectacular successes. Any appointed successors, anything that anybody knows about this.

I love the company’s profile, business model, it being ambitious and almost comparing itself to Globant etc, but for a long term investment (8-10 years holding period), we need to know about the future leadership of the company.

There are better companies in market to invest than Happiest Minds. Its just not promising enough to put your money on. They werent able to give any returns for past 3 years. Infact I am in 30% loss. And as soon as stock tried to take stance at 900 Rs price, the Founder sold the stock and pushed it to 700s.

i think in 2 years the stock may again reach to 1000 and by then it will be time for Soota to sell another portion of its stock as stated by him. And boom! back to 700s. So for a good half decade this stock is going to give returns less than inflation.

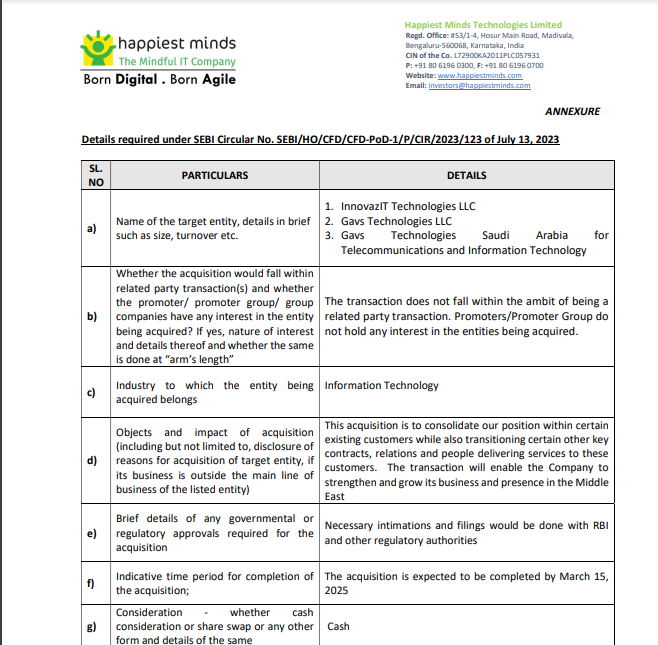

Happiest Minds will acquire a 100% stake in InnovazIT Technologies (Dubai), Gavs Technologies (Oman), and Gavs Technologies (Saudi Arabia) for $1.7 million (₹14.73 crore).

This acquisition aims to strengthen the company’s Middle East presence by consolidating customer relationships, contracts, and the delivery team.

The acquired entities specialize in Application Development, Maintenance, and Infrastructure Support services, primarily catering to large enterprises in the BFSI sector across the Middle East.