Disc: Recently sold out all holding. 100+PE for 20% growth just doesn’t justify these valuations.Sensible inorganic growth will be very difficult in current times. Looking to re-enter if Neuland Labs scenario plays out

Sundar Ramaswamy, Senior Vice President & Head CoE - Digital Process Automation,

Happiest Minds said, “Happiest Minds has been delivering Automation Services to ensure

our clients realize the full potential from their Digital Transformation initiatives. We have 500+

Happiest Minds delivering $30Mn+ automation solutions annually in the areas of Process,

Infrastructure, Security, and Test automation. Through our investments in the Digital Process

Automation CoE, we will continue to lead efforts in building automation solutions that drive

sustainable business impact for our clients.”

Microsoft has recognized the company’s RPA work in the automation space. Recently, Mr.

Satya Nadella, CEO of Microsoft, highlighted Happiest Minds’ work at Coca Cola Bottling

United at his Inspire Opening speech.

to watch Inspire Open show (Happiest

Minds mention timestamp 20:10). The detailed case study of Coca Cola Bottling Unit is

published on the Microsoft customer portal as well.

Digital Process Automation practice - 500+ resources, $30M+ annual run rate - A quarter of Happiest mind revenue ? !!!

Attrition has shown an uptick and we have moved slightly up to 14.7% on a trailing 12-month basis compared to the 12.4% that we had disclosed in the earlier quarter. Better than other players like Mastek.

As we have been disclosing earlier, we have very healthy free cash flows. We continued to have that at about 99% of EBITDA, and that’s about ₹ 66 crores for the quarter. We ended the quarter with cash and equivalent balances of about ₹ 607 crores.

We see that the important thing is we also don’t want overdependence on the top five accounts in that sense. And if you see that percentage, for us it’s come down from 14.5% to 13.1% in this quarter as compared to the whole of last year. And this is in spite of a very healthy growth even in the larger accounts.

Regarding IMS,DBS & PES, the takeaway from these numbers is that actually we have got steady growth from all of the three business units contributing exceedingly well, to in a sense, our overall targets and it is not going to be driven by just one deal. Every one of them has a good pipeline. Everyone has a good potential and everyone at varying times continues to do a higher percentage growth than the other.

Subcontractor costs increases on back of middle eastern onsite business needs and covid induced travel restrictions.

Medium term visibility (investments should continue) only from management on numbers currently that we have are sustainable or if things open up, should we expect a decline in revenues coming from the Edutech vertical.

1 More quarter before work from office resumes more openly

Strong EBITDA margins of 26%. Management has never been more optimistic about technology then now

4000+ employees and 225 people joined. Attrition a industry wide concerned. Strong deal wins

20% Growth over next few year though not a formal guidance. Automation as % is report to show the amount of automation % project that they take in robotics, process etc. It does not increase/decrease margins, just that it opens up upsell opportunities and new logos (business).

Working on multiple levers to maintain margins including talent management & rate hikes and utilization.

Confident of sustaining the margins

22-24% EBITDA margins is something that can be sustained, till the time office open up. Wont sacrifice margins for growth

Supply side focus on lateral side. Visiting campus and hiring from there. 500 people planned in next nine months

Shift in customer mix from $5m-$10m and in lower buckets is due to run rate method of calculation of revenues against TTM, which gives skewed picture. Nothing of major concern. Look at annual snapshot

Investment to continue in newer & emerging technologies as market demands including that of metaverse to build CoE

Taxation base have now normalized. All benefits from previous quarters exhausted

Discl: Not Invested. Tracking closely. Please feel free to add to the notes. Will be happy to collaborate. Happy Learning !

Long term aspirations of $1B revenue by 2031, they will close FY 22 around 1000 cr+, that’s 8 times in 10 year. Will need 24%+ run rate to get there and will include inorganic part, mgmt discussions on same towards end of interview

Yes, it’s possible, infact Ishmohit clearly mentioned here that Happiest Minds is claiming(or at least aspiring) 100% digital services business. In comparison, EPAM already has ~100% digital services and it’s an already established global player trying to enter India and LATAM region.

Since last post, I am glad that I booked profits at right time. No change in business, growing at 40% but still seems quite expensive.

Since this thread is new due to recent listing, maybe we can post each quarter’s cc growth for this business. This will serve a purpose similiar to milestones. CC is one of the most important metric which actually matters and isn’t diluted due to currency movements. I have never seen cc growth history in other IT business companies threads and maybe this one can be the torchbearer.

Will try to add cc growths for all quarters till now and maybe others can also contribute the same.

Additionally, if someone is aware of any other place where this data is readily available, please provide the link or source here.

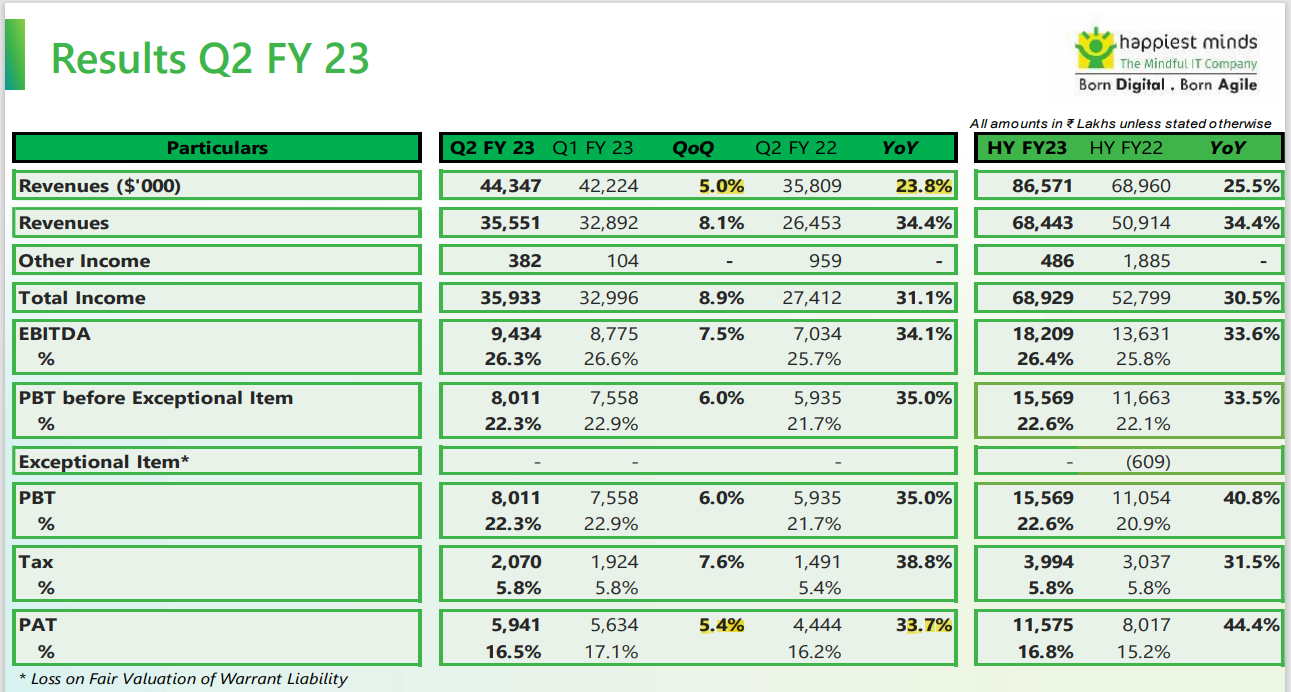

Financial highlights:

• Operating Revenues in US$ stood at $44.3 million (growth of 5.0 % q-o-q: 23.8% y-o-y)

• Total Income of ₹ 35,933 lakhs (growth of 8.9% q-o-q; 31.1% y-o-y)

• EBITDA of ₹ 9,434 lakhs, % 26.3 of Total Income (growth of 7.5% q-o-q; 34.1% y-o-y)

• PAT of ₹ 5,941 lakhs (growth of 5.4% q-o-q; 33.7% y-o-y)

• Free cash flows of ₹ 8,580 lacs

• EPS (diluted) for the quarter of ₹ 4.09 (growth of 5.4% q-o-q; 33.7% y-o-y)

Is it the okay/reasonable price to get into Happiest Minds for long term or do you think the price is still high considering growth forecast (25%) in the recent concall vis-a-vis other midcap IT space in the similar field? Appreciate if anyone can help me out on this. Thanks.

@saghOS01 - If you are asking from technical point of view alone, I believe a better entry point was Rs. 790 that the price action gave on 28-29 Mar 2023. You ask “WHY”. The answer is - this is 62% retracement of the run-up from Rs. 300 to Rs. 1600. I believe the price is now discounting multiple negatives that exist for overall IT sector. Please note, the US$ is showing bullish intent versus INR, and if that pans out, I believe many IT companies will experience temporary tailwinds for the coming quarter. So start nibbling some share every month. Don’t worry for best price point, if long term investment is your calling.