2021 CY Performance Review and Monthly Portfolio Note - December 2021

Gratitude! Gratitude! Gratitude! That’s the top of mind thought and expression which comes to mind when I look back at the past 1 year. Just getting through 2021 with a healthy body and sound mind is an achievement in itself to be thankful for. A year which started with great optimism about mankind’s ability to fight this pandemic through safe and effective vaccines has seen one too many unpredictable topsy-turvy events culminating with another new super contagious variant of the virus. This has meant governments continue to enforce severe restrictions on a number of non-essential businesses and another stop-start year for India’s economy. I suppose this is how we define the “new normal”. However, I still have hope this will all end in the next 24 months and we will resume a majority of our pre-Covid ways of living again.

Amidst all this turbulence, fast changing global macros, high inflation, supply side constraints, risk of Fed rate lift-off, Indian equities have done exceedingly well despite the massive FII selling over the last 9 months. As they say “bull markets climb the wall of worry”. Also, with more and more index constituents (metals, mining, PSU) showing decent earnings / cash flows and a very supportive liquidity environment, Nifty / Sensex continue to trade at reasonable valuations according to me. I remain quite bullish over the next 12-24 months even with the concerns around inflation / hike in interest rates. I’ve posted a thread on Twitter about the inter play of interest rates and equity market valuations and why I continue to remain bullish.

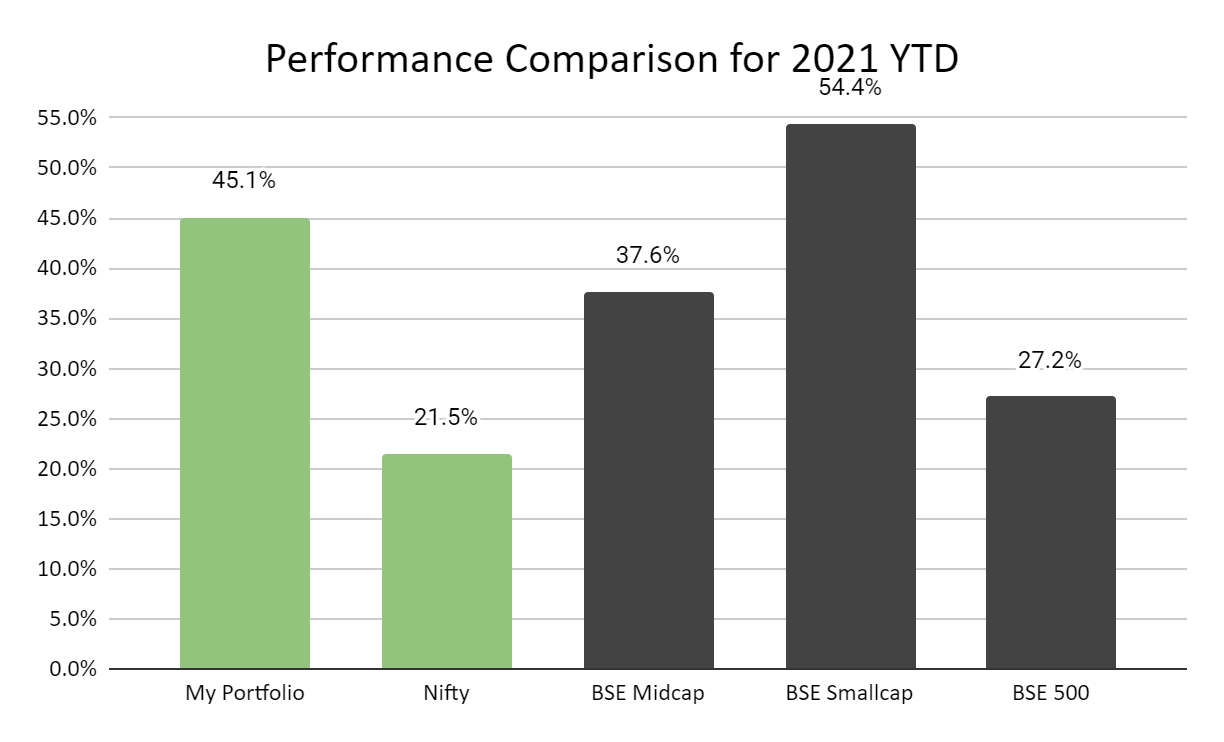

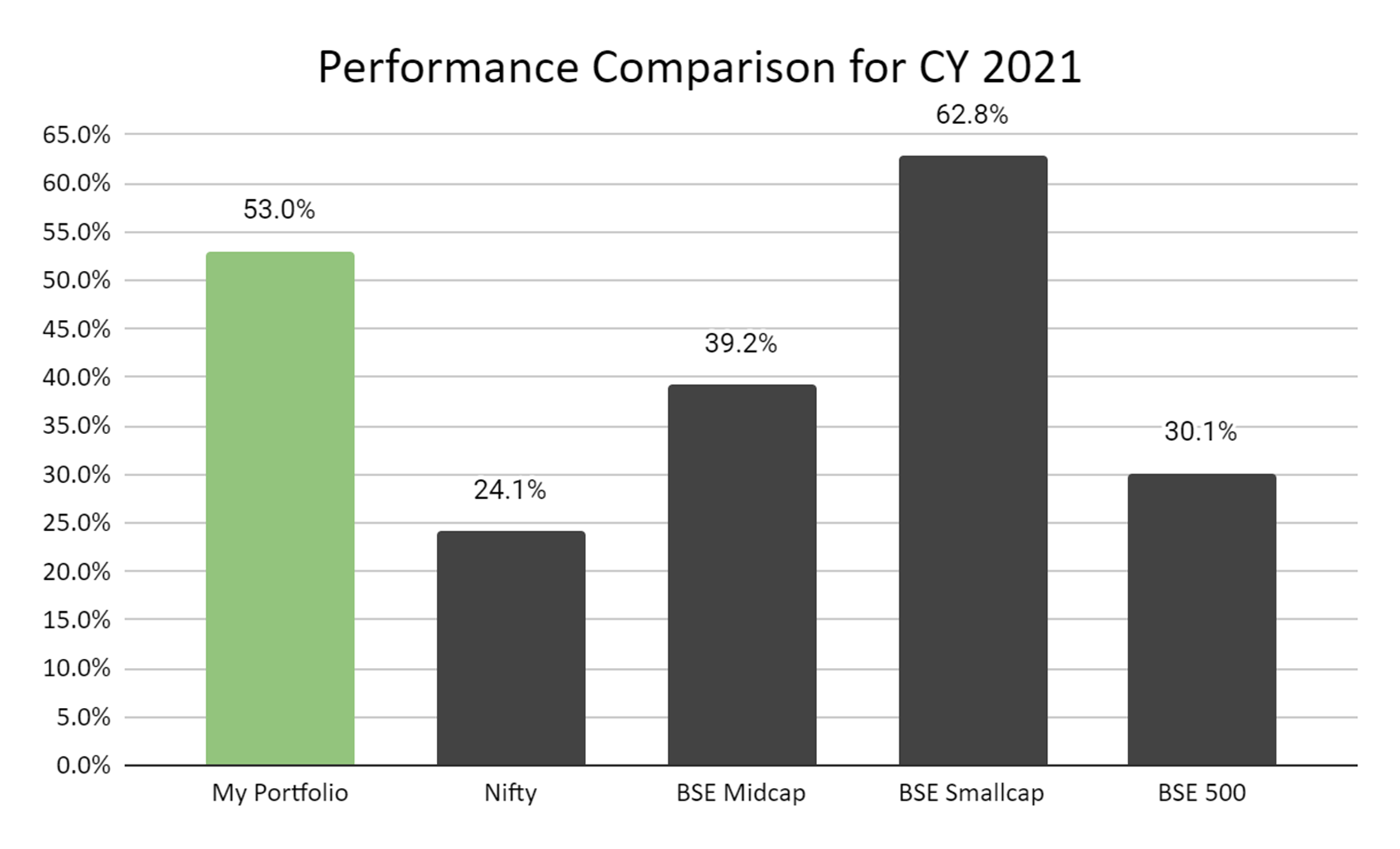

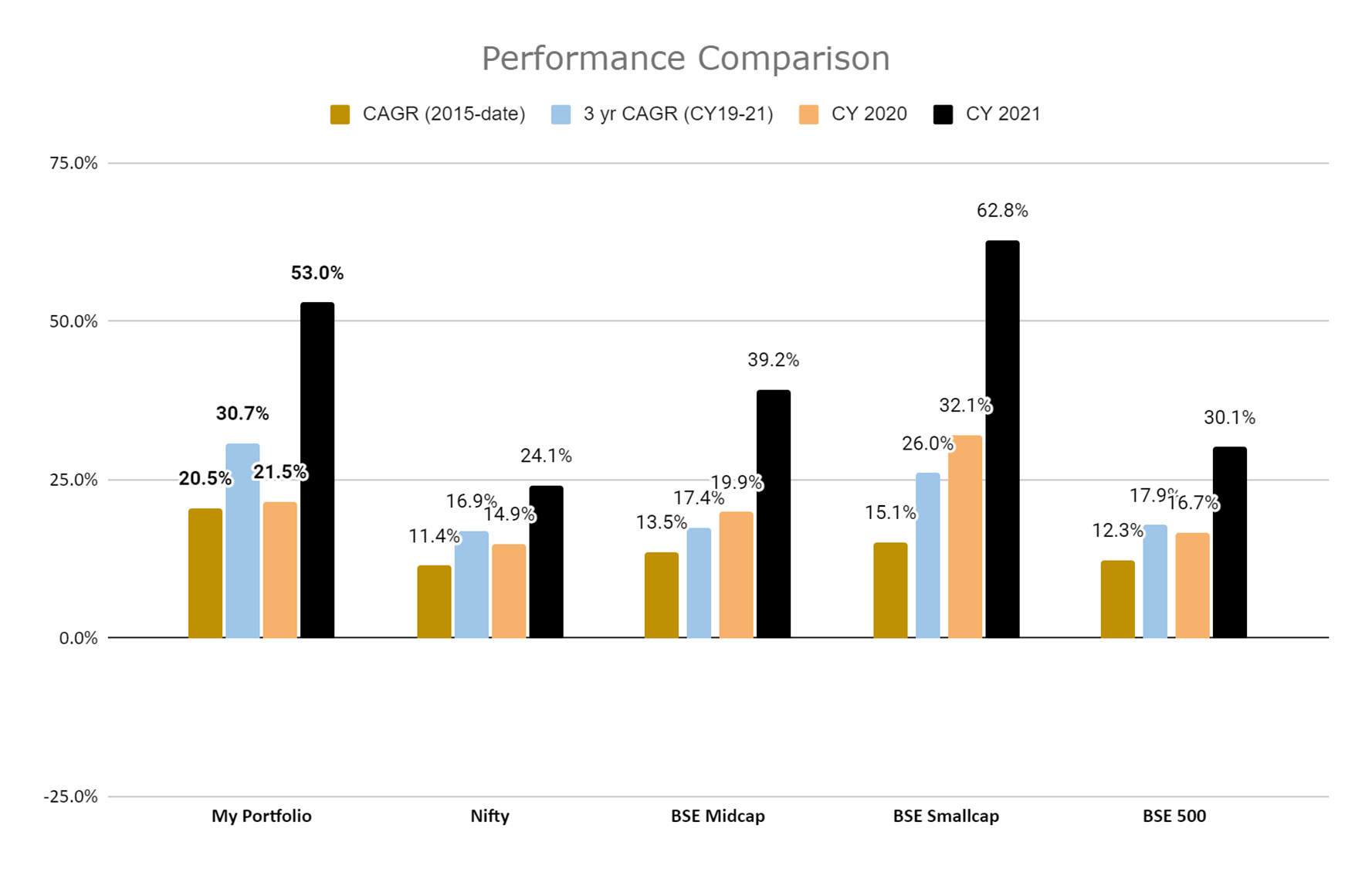

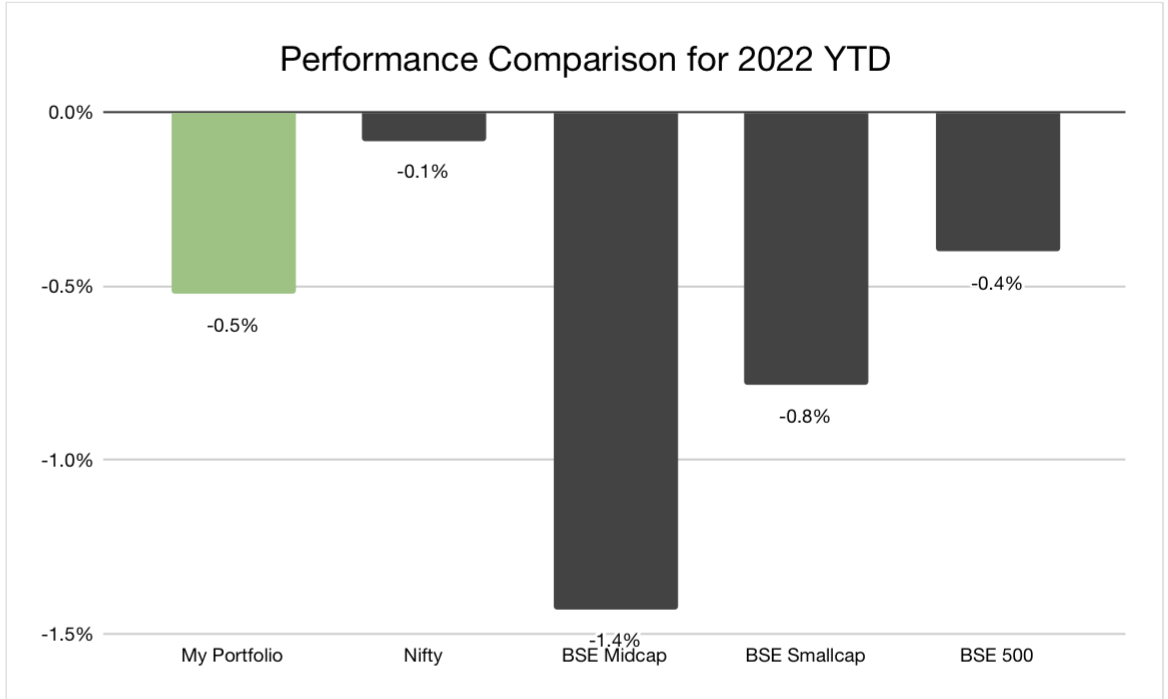

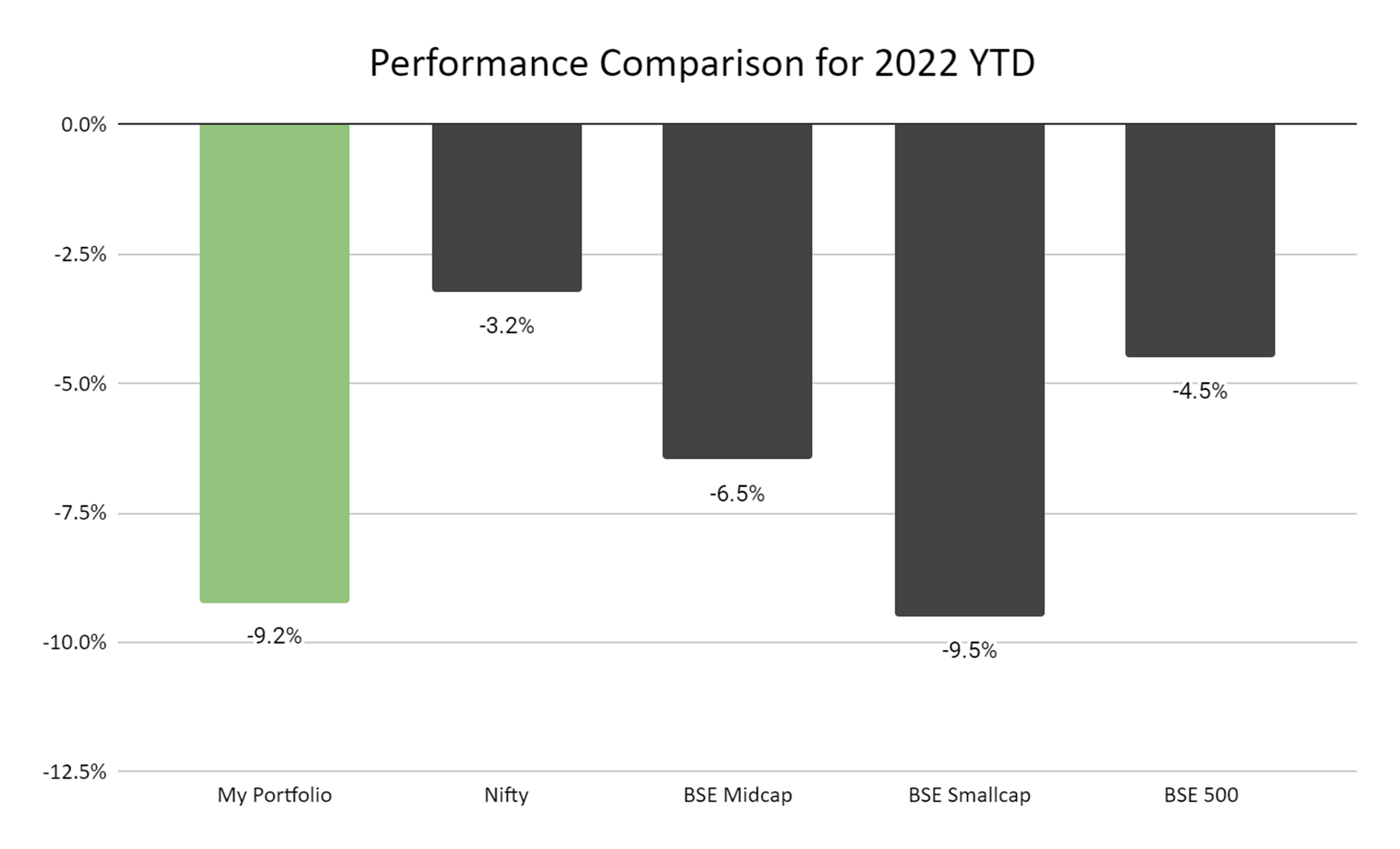

Now, coming to my portfolio performance for 2021 - the graph below speaks for itself, I really can’t ask for much more! Finally, I’ve gotten a taste of what all the hallowed folks on this forum experienced in the 2013-14 bull run. The rewards of investing in good quality small/micro cap businesses are almost unjustified in my view. DII/FII’s lust for high growth businesses has taken the valuations of a lot of small businesses to really heady levels. Only a consistent high rate of earnings growth can be the savior from now on for the next couple of years. So it’s a great time to do a portfolio review and only stick to the high conviction bets which are expected to show consistent / high earnings growth and dump the mediocre growth ones as valuations could come off fast!

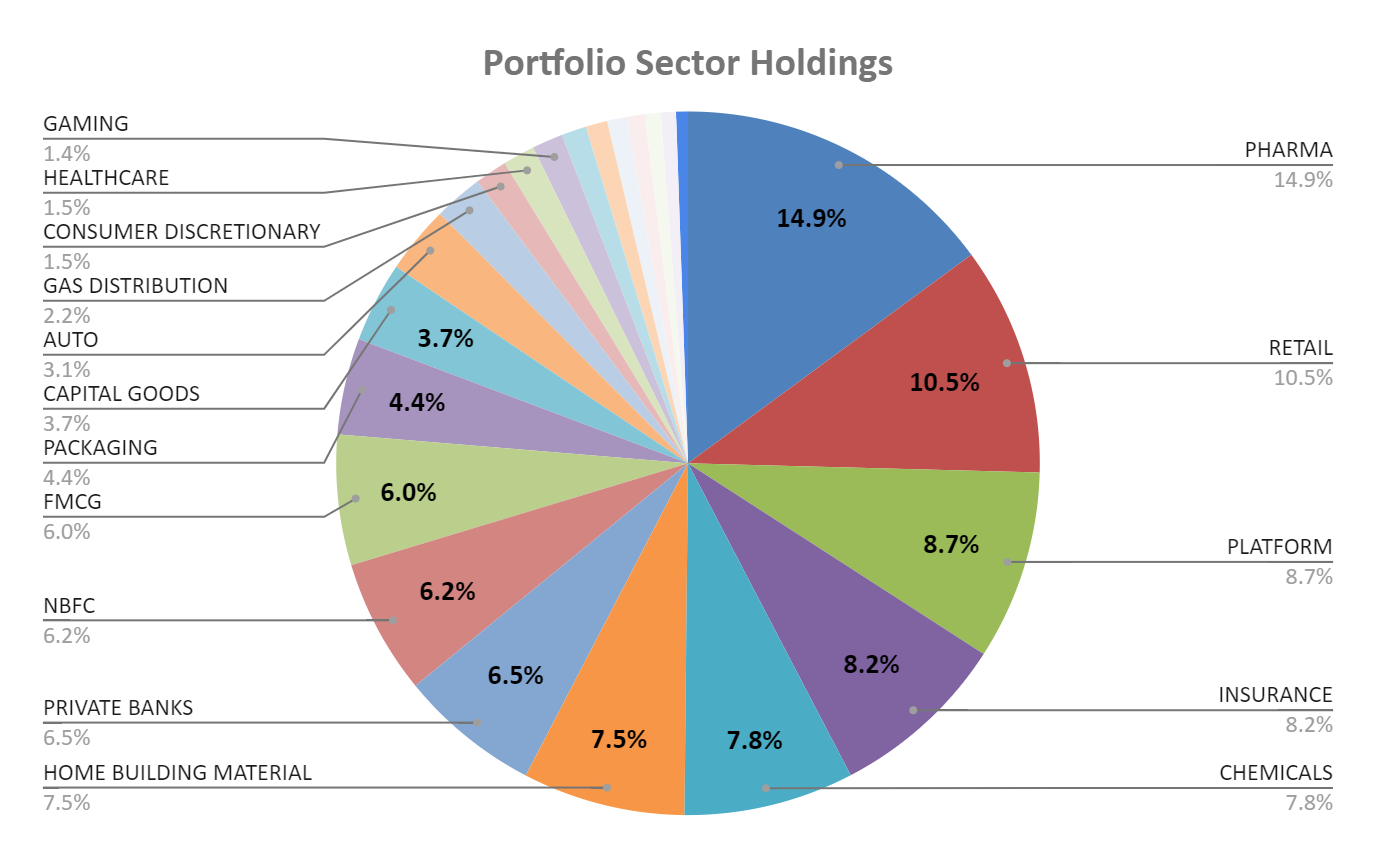

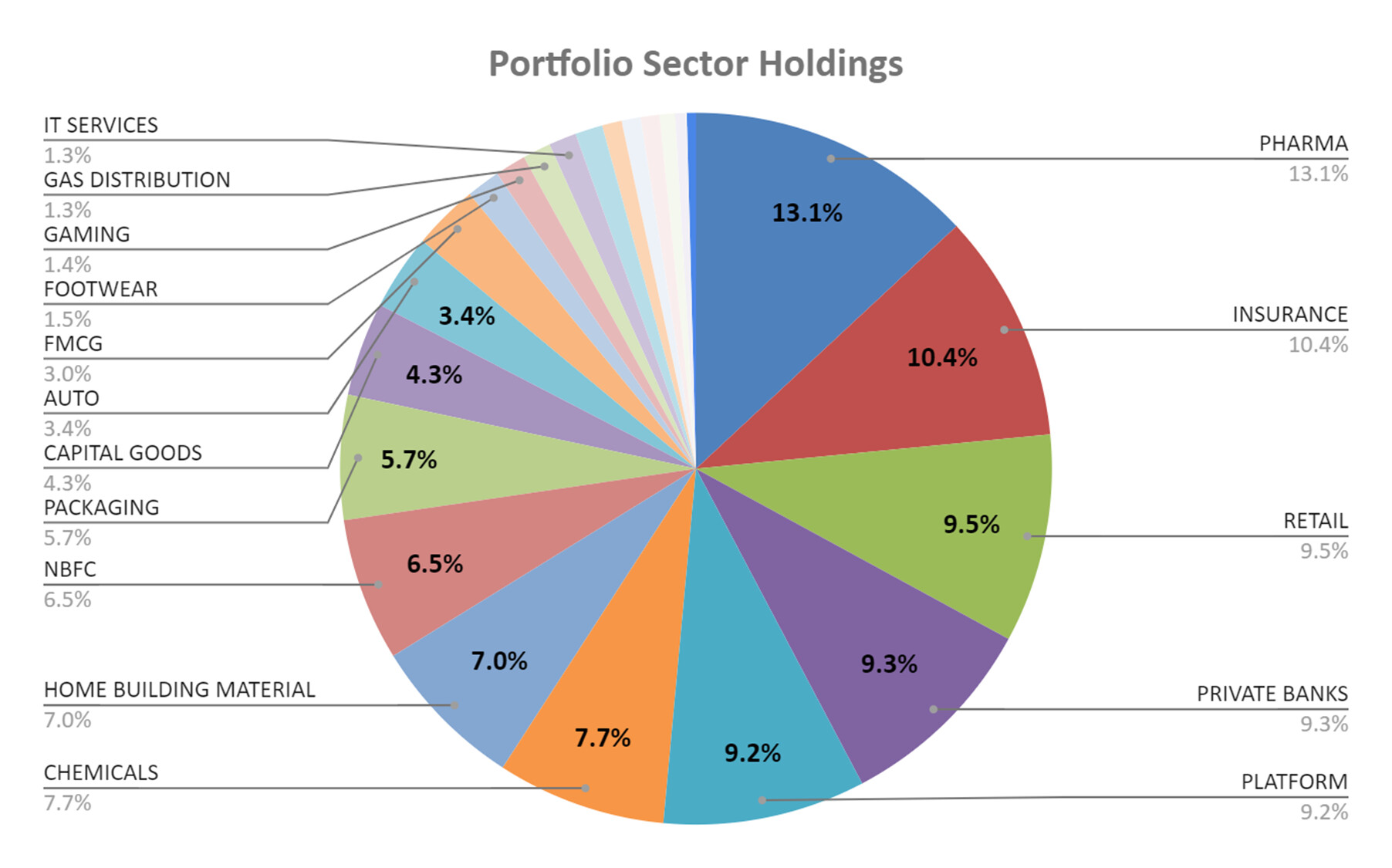

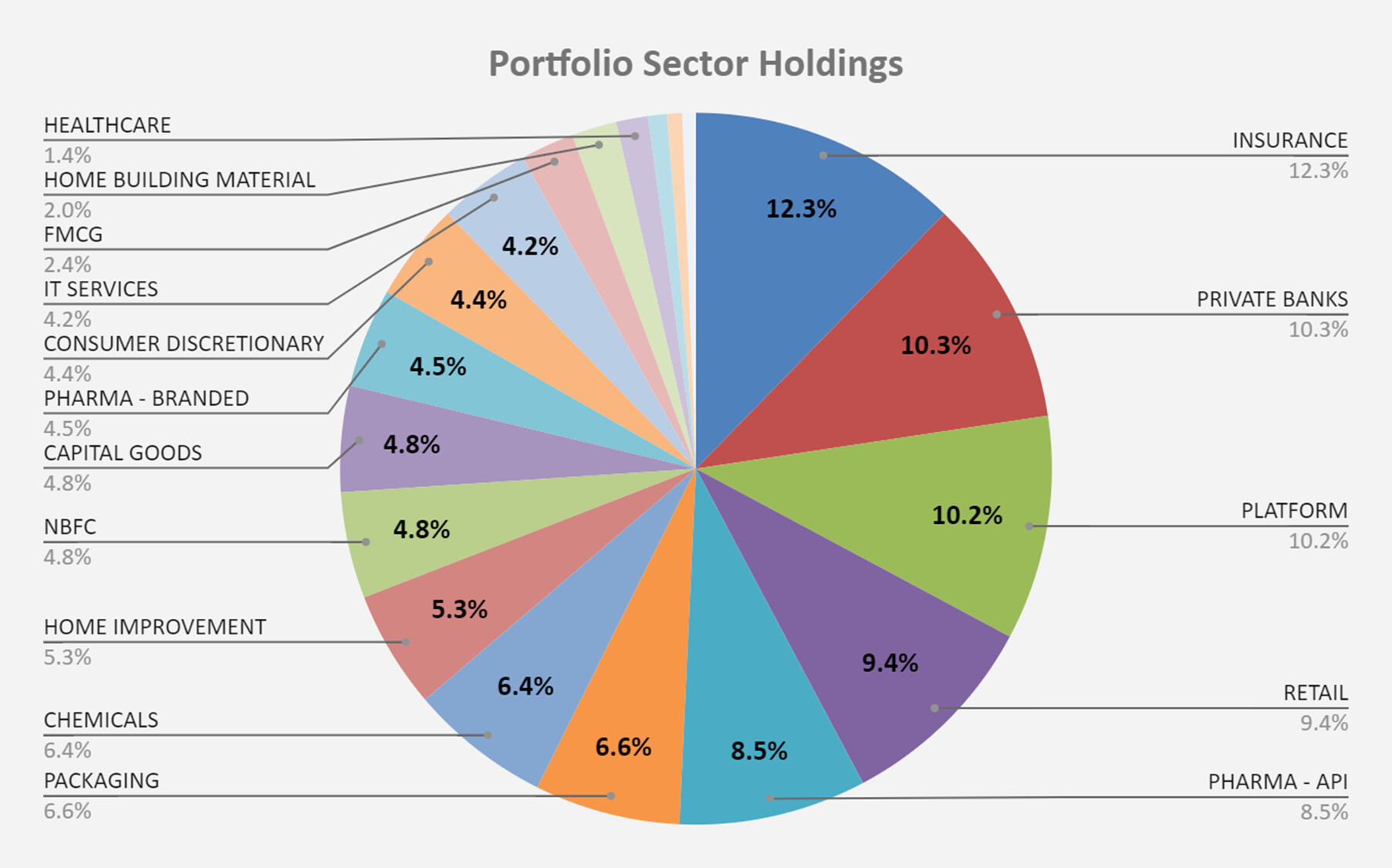

Beta Drugs, RACL Geartech, Acrysil, Goldiam, Tips, Macpower, Rajshree, TCI Express, IRCTC, CAMS have been some of my big winners this year and it helped to get out of some of them at the opportune moments. The month of December had much higher volatility than I expected with sharp cuts and recovery in a matter of days. However, my satellite portfolio (mostly small / micro caps) again helped deliver handsome gains this month for me. I’ve been piling onto financial services businesses over the last couple of months and 25% of my portfolio is now in private banks, insurance, NBFCs, etc.

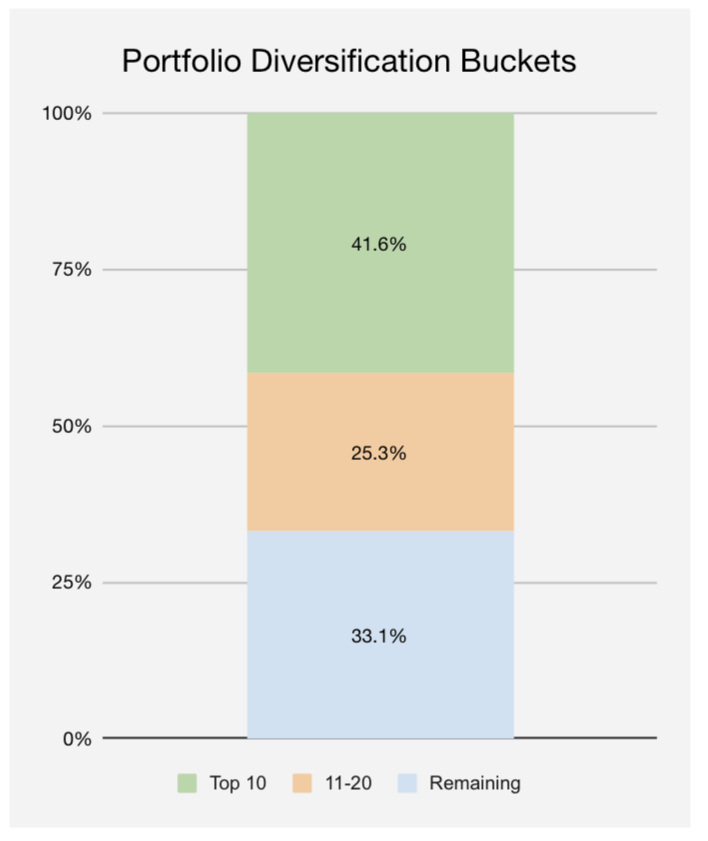

I’ve cut down my portfolio positions by 30% and still have a portfolio of 50+ companies. However, as the year has gone by, I’ve started allocating a lot more to high conviction bets and so now more than 50% of PF is in the top 15 positions and I’ve been piling into financials (banks, insurers, etc.) over the past few weeks.

Portfolio Exits

Strides, ITC, Godrej Agrovet, Britannia, Poly Medicure, Ice Make, Insecticides India - Apart from Strides, nothing major wrong with these businesses except re-allocation to higher growth/conviction bets majorly financials. Poly Medicure is a true coffee can / consistent compounder business in my view with great management - however valuations don’t seem to offer much margin of safety for good compounding. Watching this one like a hawk to buy back on dips.

Portfolio Entry

Mirza International - A consumer discretionary brand play at extremely cheap valuations of 1.5x sales. Demerger of branded Red Tape business (annual turnover 675 cr and 35-40cr PAT) announced from parent entity Mirza International. Metro Brands does 28% EBITDA margins with 1200 cr revenues, assuming Red Tape can do 1000 cr turnover in FY25 with 25% EBITDA margin - can do 150cr PAT and 25x multiple for consumer facing brand - it can be 3750cr valuation with other private label business also doing 20cr annual profit - 200-300cr valuation. So total business valuation of 4000 cr. Demerger ratio of 1:1 - 1 share of Red Tape for every 1 share of Mirza International. “The promoters’ have experience of around 40 years in the leather industry, during which time the company achieved significant market position in the domestic leather footwear market. The company has diversified presence across multiple channels, including company-owned retail stores, franchisee-based retail stores, established multi brand retail stores (such as Shoppers Stop and Lifestyle) and ecommerce websites (such as Amazon and Flipkart). MIL sells footwear, apparel and accessories, majorly under the Red Tape, Mode and Bond Street brands in the domestic market. Also, it undertakes make-to-order contracts for various reputed brands in the overseas market. Vulnerability to fluctuations in foreign exchange (forex) rates: The business operations of MIL involve importing raw materials, such as cow hide, which is not available in India, and other hides during temporary interruptions in its tannery (for example during the Kumbh Mela).” Source Crisil

Allocation Changes

Increase - All ICICI group companies in portfolio, HDFC Bank, HDFC Life, Kotak Bank, MAS Financial, Valiant Organics, Neuland, Macpower, Goldiam (offered a sweet little buyback 50% above CMP).

Decrease - IGL, Shivalik Rasayan, Vaibhav Global.

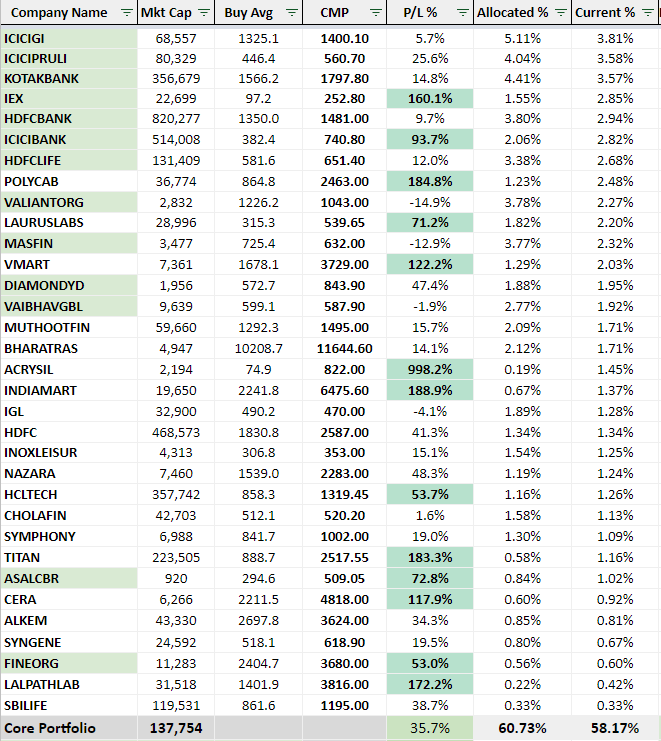

Core Portfolio

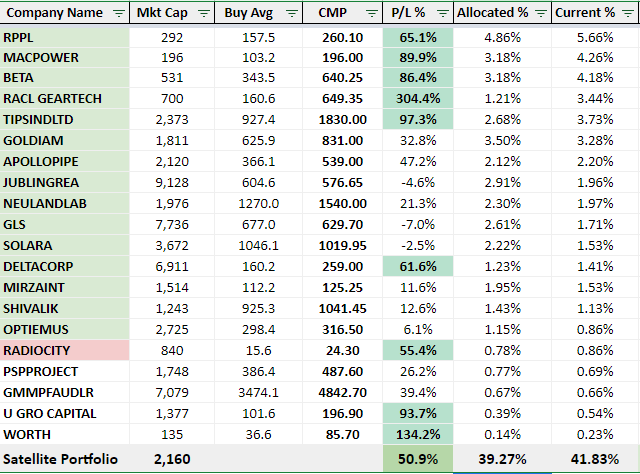

Satellite Portfolio

Sector-wise Portfolio

It’s been a fantastic rewarding year much more than I wished for or even imagined! Here’s hoping and wishing the new year brings the same and more for everyone!

PS: I’m not sure if I’ll be keeping up the monthly portfolio updates in 2022, but will definitely try and post as regularly as I can. Always happy to discuss and answer any questions though