Thanks chaitu.

Ur analysis and info is good enough. Even from today’s level…gulshan can be a doubler…logical reasons are. All client to who it supplies are in a growing segment. If u read the annual report of their clients… Most are growing steadily. Gulshan is bound to grow as its sales is dependent on these key clients.

It is obvious to watch out this company for long term. I especially like it because of its synergy between segments and Identified grain based liquor business as a future prospect. In the long run, grain based liquor companies will play an important role in this industry as molasses price are increasing because of its allied industry requirement. United spirits also now turning its premium brands in to grain based which in trun a positive demand pull. Also, chemical sector is in the 3rd position in terms of sector growth after pharma and food. A lot of inititive is done from goverment side “make in india” to premote this sector and improve export. As a leader in this sector, gulshan will benifit a lot.

Can anyone clarify why the tax rate is so low historically, unable to understand. @Chaitu_1614

@atishay1, Company is paying MAT as Company has tax free income from its captive power plants.

1 Like

CK Jain latest interview in CNBC

Key Points:

- Key projects (grain processing, desi liquor )completion by Q1 2016. Starch processing, Sorbitol capacity expansion to completed by 2017 March and company plans to deploy 150 crore for the same.

- Grain processing plant in UP started contribution to sales from Q2.

- Ability to pass on raw material price hike to customers in next quarter (HUL,Dabur,Coalgate etc.)

- Sorbitol domestic consumption estimated growth is 10% where as less margins for exports.

plans to increase the sorbitol capacity expansion 20% by 2017. - Paper plants has to adopt onsite ppc plant for reducing the cost and ease of maintenance, either today or 2 years down in the line. GPL is the only company to do so in India.

- Aim to reach 800+ crore sales by 2018 March, considering immense market potential in PCC, Sorbitol, Liquor and other business.

2 Likes

excellent write-up chaitu - this is a very good one that gives us all a sense of the business

I have a few questions

-

what happened post FY 11 - EBITDA margins plummeted 700 bps from FY 10 to FY11. would you know why ? margins over a 10 year period have ranged from 27 % to 14 %

-

how difficult a product is calcium carbonate to make and how critical is it to the end product - that will give us an indication of the pricing power ?

-

would you have a sense of how much agri commodities like corn are a function of the RM costs in total

-

Until 2011, GPL’s product portfolio is very limited. Business inflection started by way of expansion since 2011 and the benefits are seeing now. For completion of these expansion projects debt levels are increased certainly(credit rating A1+ by CARE) , but without these expansion i didn’t see the future growth.

-

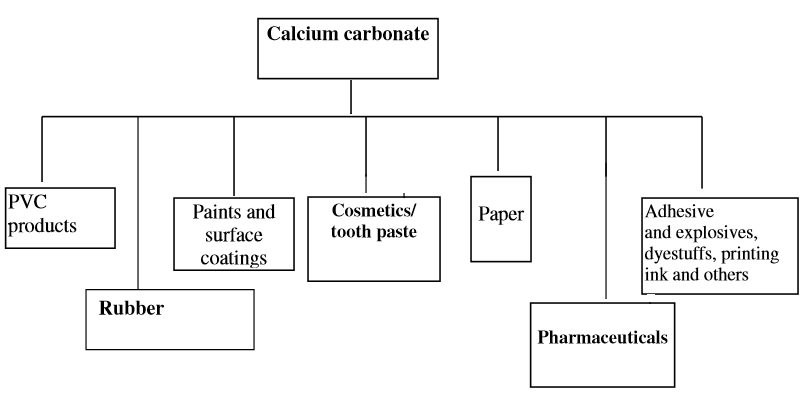

The source for CACO3 i.e Limestone availability is abundant in India. An installed capacity of more than 2Lakh tonnes exist in India. Players like Asian paints is fully acquiring it from domestic players such as GPL. Here i am giving end use applications of the same, i personally feel lot more un-captured market for GPL considering current annual sales of 430+ crores.

-

The same point i raised to management in Q1 itself and their answer is follows.

Question: Raw material prices are jumped from 32.4cr(35%) to 44.44cr(40%) on comparing last year Q1. Any plans to tackle this situation or creating hedge position on some key raw material prices going forwards.

Reply: Raw material % to sales has gone up due to product mix as we have started commercial production of starch derivatives. The volume of starch derivatives is more in this quarter as compared to the previous year quarter

My Opinion: As informed during the interview regarding Ability to pass on raw material price hike to customers in next quarter (HUL,Dabur,Coalgate etc.) gives more idea about the pricing power as well.

4 Likes

On ValuePickr I believe we discuss business and fundamentals and not price … at least not only price … Going thru thread will give you enough information for you to decide.

Hello All,

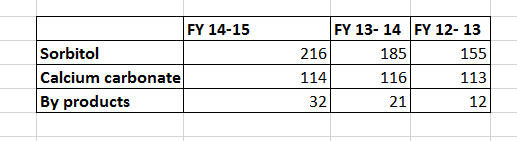

Below is the segment wise revenue for the last 3 years (Taken from ARs). Any idea why Calcium carbonate not showing growth ?

Note: Not included IMFL as it recently started and others are miniscule

Regards,

Kiran

@kkvinvestor

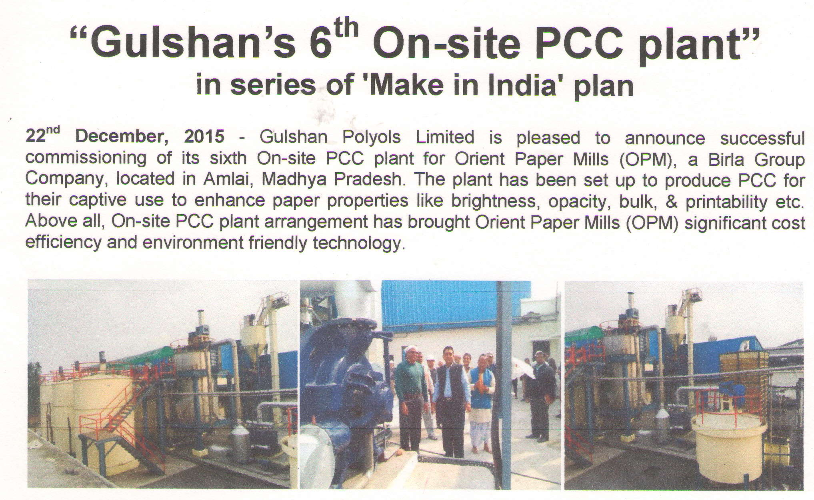

Looks like company has recently expanded its Calcium Carbonate or PCC

- On site PCC & WGCC plants in Bangladesh commenced commercial operations.

- On-site project with Orient Paper Mill, MP has started & production is expected by 31-Dec-15

(source - q2fy16 press release)

therefore it will reasonable to conclude that we may see PCC growth in this or next quarter.

Hi Chaitu,

Do you know if the onsite PCC plant provides a continuous revenue stream for maintenance or if majority of revenues get realized during the installation ?

Disc: Not invested, tracking.

GPL successfully commissioned 6th PCC plant, expecting better quarterly results in the current quarter.

Company made exchange disclosure about the same today.

Regarding Onsite PCC concept

No wonder just like many other companies in commodity chemical this also turned into a multibagger but my concerns are why is Gulshan Polyol’s Return on capital employed is low compared to its peers. PE wise valuations look reasonable even for fresh entry today provided they have clear strategy to scale up their bottom line. @Chaitu_1614 as you mentioned they have 4 divisions , so which division is hampering the bottom lines ? as @aveekmitra mentioned IFB Argo is one loss making unit they got rid off, what else is dragging their profits ?

Some of my operational / business understandings i will put here.

-

As long as Market players think GPL as a Commodity chemical value will exist in this counter. Once the market perception changes towards GPL by way of PE re-rating, i will be the first player to exit this counter.

-

Though it is having 4 Divisions, Animal Feed and IMFL divisions are in budding stage. What ever the growth coming from these 2 divisions will be added to bottom line going/growing forward.

-

I don’t see any Exact competitor to GPL, which is catering to wide range of segments / companies

FMCG - Colgate, Wipro, Dabur

Paints - Asian Paints, Berger, Nerolac, Shalimer, Pidilite

Food - Brandico, Yahoo, Candico

Pharma - Cadila, IPCA, Pfizer, Glenmark, AstraZeneca, Cipla, Ranbaxy, Novartis

Footwear - Paragon, Relaxo, Bata, Lakhani

Plastics - Sintex, Apollo, Supreme, Polyplast, Ashirwad

Paper - ITC, Century, TNPL, Orient

If you feel any nearest competitor, please let me know. -

For the last 15 months, CACO3 division is stagnant, considering the same management gone for capacity expansion. I am with management view that, all the Paper companies will look for onsite PCC plant setup. The logic is simple, saving the cost and easy maintenance, hence everybody will adopt it. It is a matter of time for all the paper companies setting up the same.

-

Management aim to reach 800+ crores sales by 2018 (i feel they will cross these figures). Even if they do conservative estimation of 700 crore sales, which will be translated to 60 crores net profit and translating to an EPS of 62rs. Which is more than 100% growth in the bottom line in next 2 years.

1 Like

Company in the press release mentioned that

PCC area installed under lease agreement in the premises of its end user.

What I could make out is

- The land is owned by the paper mill not GPL.

- The plant is operated by the GPL.

but the statement had so many questions to be answered

- Who pay for the capital cost of PCC machines and equipment?

- Who hires and pay the employees?

- How is GPL payed by the paper mill?

Any help from community will be appreciated.

Yes, GPL will get running and maintenance cost from Oriental Paper Mills (OPM).

Onsite plant has been leased out to OPM and OPM will pay lease rentals. This will provide steady revenue to the company.

The company is not minority shareholder friendly and can be said to have corporate governance issues.

In 2014-15, company issued 4.35L equity shares and 5L convertible warrants to foreign portfolio investor. Company has total preference share @8% at 10.25L. The original issued shares are 84.48L.

So while calculating ratios, we need to consider total number of shares as - 104.08L.

The TTM NP is 30.05Cr. EPS comes to around - 28.87. So P/E ratio comes to - 15.7 @CMP of 453.7.

FY15 net worth of the company is 211.86Cr. That gives book value of - 203.55. At CMP of 453.7, P/BV works out to 2.23.

Why dilute equity when CFO seems good enough and business does not really need money? Why not do block deals?

Disc - Not Invested

@rupeshtatiya,

After sailing the company as a retail shareholder for last 3 years, i don’t see any problem w.r.t investor friendliness or Corporate governance. If any such issue exists surely it will impact at one stage.

When the FII allotment happens share price is nearly 160rs with capacity expansion in plan.

If you see their corporate actions they always giving importance to retail investors.

- They brought additional funds to company and FII to shareholding to improve the confidence.

- They increased dividend payout ratio last year onwards.

- They listed on NSE to improve the liquidity

- They brought Reliance mutual fund to board to give confidence further regarding the transparency.

Market is recognizing the same and it will take sometime to get re-rating according to me.

1 Like

Preference dividend was 0.82cr (10.25L shares) and equity dividend was 3.11cr (88.5L shares), the difference between the per share dividend is there for everyone to see.

They have credit rating of A+ and hence they could have taken loan instead of issuing preference shares, loan interest rate could still have been more than 8% but that would be minority shareholder friendly decision.

I still need to dig out that preferred@8% were allocated to promoters.

Another problem with small/mid cap space is non-current investments. I am learning to ignore it while valuing companies in this space.

GPL has 4.79Cr in non-current investments (2Cr in HDFC MF, 2Cr in ICICI MF and some investments in Tata Steel, NMDC and local Gujarat projects etc.)

Long term loans and advances are 5.5cr.

This ~10cr money is 3x the equity dividend.

I don’t care much for liquidity increasing measures like listing on NSE, Splits etc. They are just good news for traders and news channels but that does not increase any value for investors. I treat them as smoke screen.

I also like undiscovered companies where institutional (FII, DII) holdings are low as one bout of re-rating comes when these players come in. The moment stocks become discovered, one needs high conviction in business to pay premium for stocks.

Thanks,

Rupesh

1 Like