got hold of this blog on gujarat themis. very detailed and insightful analysis on the company.

7 Likes

Analysis is good but how come exit PE of 17 is considered the norm ? Almost no pharma company trades at that PE even during this downturn of pharma/ api companies and it did not during the last upturn phase in 2020 - 2021.

2 Likes

Company is working on almost full capacity therefore revenue degrowth has happened YoY.

It got benefitted with excess inventory in Q1FY24 which is not present at the moment.

Growth is likely to be slow until migration happens from A) current Rifa-intermediate product to Rifapentine which will free up some capacity (it will lead to same revenues at 50% capacity as prices for the products are high while product’s requirment is low) coupled with B) New capex to be commissioned in FY25 end most likely.

But until then, don’t expect any growth this FY (especially since last year got the benefit of higher margins & stack up of inventory which was ultimately sold despite business running at full capacity)

8 Likes

Thanks for the update. Management should hold a conference to give clarity in the capex and newer products. Quant MF entered the stock , so was expecting the 200cr capex revenue kickstarting

1 Like

Hi, I was an investor in this counter two years ago. I made 30% in six months and exited.

The problem with GTBL is that it’s just a two-trick pony. There are only two products at present. When the 200cr capex will come and how much sales it will generate are the questions for the future.

There are not many optionalities. And if you compare the valuations, it is neck and neck with Giants like Divis, which is not only the largest producer in many APIs but has a large number of molecules (optionalities)

So basically, only 2 molecules and RICH valuations, prevent me from entering this counter.

Just tracking.

dr.vikas

8 Likes

- Positive Start to Fiscal Year:

- Performance met expectations in Q1.

- Sales and Production:

- Sales lower due to selling built-up inventory in previous quarters.

- Production capacity remained optimal.

- Strong demand for products.

- Capex Updates:

- New R&D facility: Half operational, new molecule development underway.

- More R&D sections to be commissioned in the next few months.

- API block: Plant and lab work ready, equipment qualification ongoing.

- Pilot plant batches to begin in a couple of months.

- Additional fermentation capacity: Civil construction halfway completed.

- Capex execution progressing as planned.

6 Likes

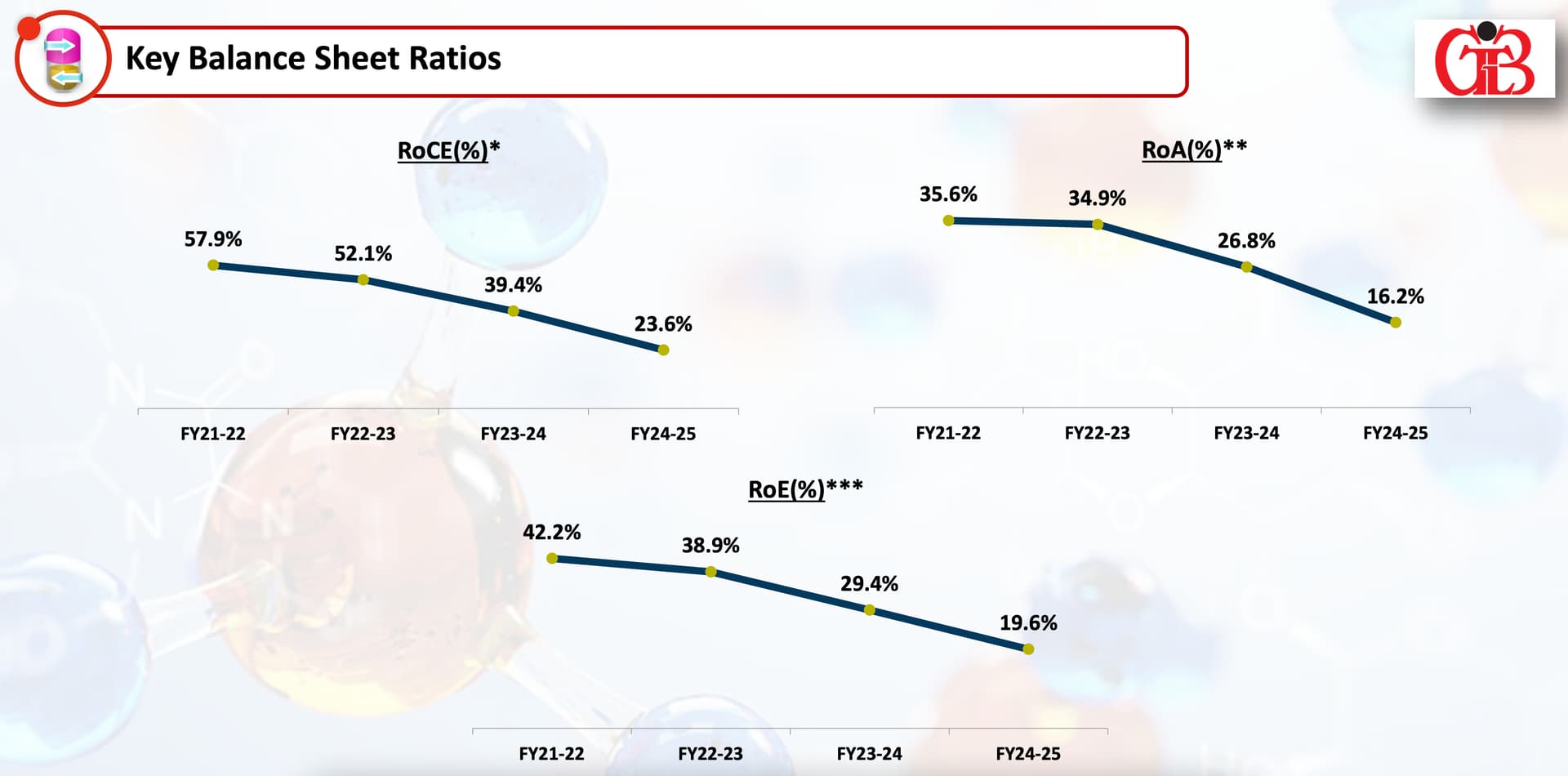

Rich Valuations, especially PS > 22.

200 cr capex with and asset turnover of 1.2 ~ 250 cr Sale (considering average values).

Current sale of 170 cr + 250 cr = 420cr.

Its trading at 8x PS 1 year forward and assuming full utilization, again considering “good case valuations”.

As the company makes high margin, 8x PS-10x PS is what market tends to give (non-conservative).

A more clarity or concall would have been good. Capabilities are not at question, valuations are!

7 Likes

Anyone has idea on the current quarter results ? The new molecules aren’t delivering yet? The valuations are ripe but expectations are also high.

Wish the management gives clear idea on where are they on delivering APIs

1 Like

I exited the stock now. Valuations are at its peak. 20x PS without any direction or concall whatsoever by the management isn’t giving any confidence to hold it longer. Made good gains nonetheless and diverted the money into some better priced opportunity.

2 Likes

hey, I don’t know the actual reason but I talked to investor relation team last week.

Low topline due to frequent power failures due to severe monsoon led to process disturbances resulting in lower output.

- Production now is back on track.

- Demand however for both our products remains very strong.

Capex Update -

- Part of new R&D facility is operational wherein new molecule development work is progressing satisfactorily. The remaining R&D sections are expected to be commissioned in the next few months.

- With respect to our API block , batches in the pilot plant are expected to start soon, followed by validation process.

- Civil construction of our additional fermentation capacity is progressing well, and we are in the process of procuring machinery simultaneously.

Talked to Investor relation team on call -

12 new molecules are coming, 4-5 molecule will start commissioning at end of FY25

Topline major growth will be visible in FY27

6 Likes

is this for GTBL or themis medicare? Any indication on the size of the molecules?

its for guj themis.

No information about the size of molecules.

1 Like

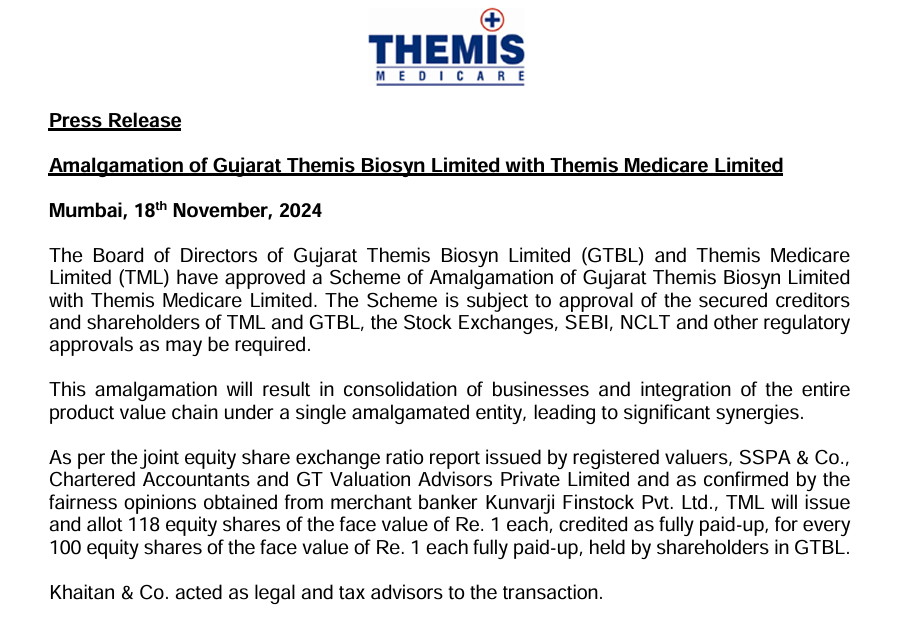

Just read this news. Need to understand the long term impact of this amalgamation scheme. On first look it appears to be positive as the company moves forward into formulations business with added capabilities in synthetic API’s in addition to its forte in fermentation based API’s

2 Likes

Now, we have to study Themis Medicare seriously.

Sharing below the credit ratings of the same.

I hope you find it useful.

dr.vikas

2 Likes

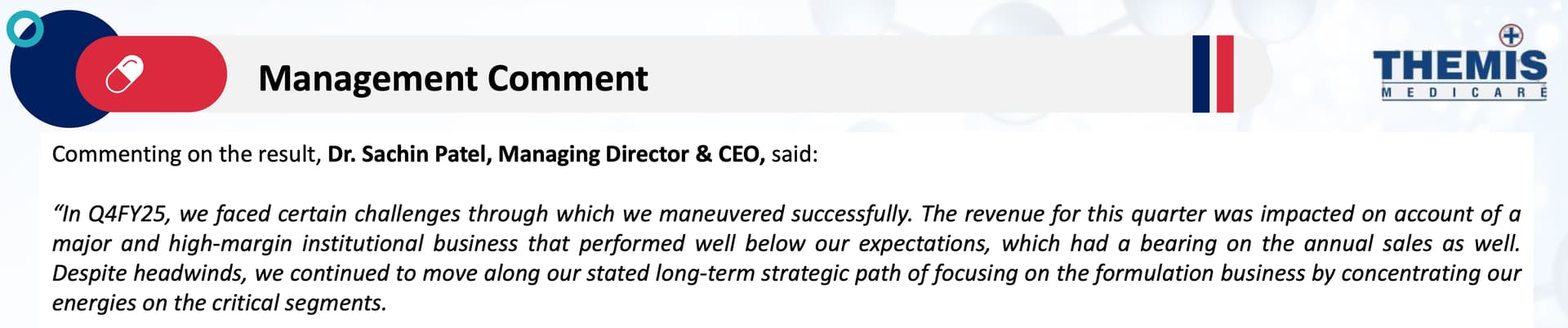

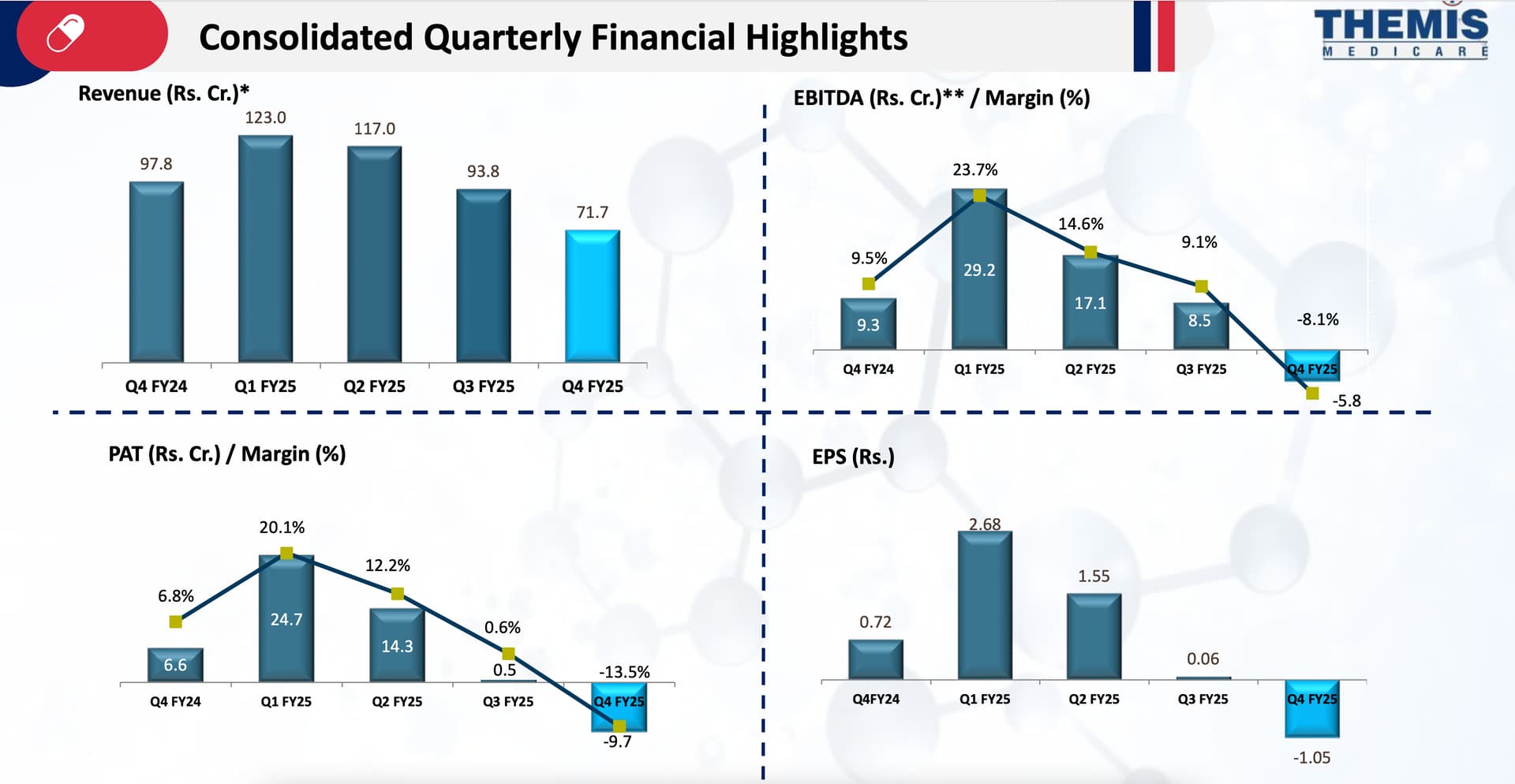

Results have come and the numbers aren’t looking good. Any one had a closer look and know why the results are muted?

This is the reason given by the management of course of Themis Medicare.

But the continuous decline in sales, EBIDTA, EPS and profit ( actually a loss in this quarter) is worrisome.

Just tracking.

Personal opinion - Better avoid this counter as of now as there are more better plays available out there.

dr.vikas

2 Likes

With declining revenue, I have to wonder whether there is enough demand for the new molecules that will be produced through the capital expenditure.

1 Like