Did anyone attend the AGM? Any notes? Also, do we know who the clients are now?

1 Like

At the end he talks about the agm

2 Likes

So I did try to attend the AGM to gain some insights into the future outlook. His introductory speech was very indeterminate and then just before he started to respond to shareholder queries, the broadcast stopped only to miraculously reappear for the last one minute of the meeting. It was super disappointing. So I wrote to the Company Secretary asking for what was divulged as future prospects but never got any response. I thought the whole affair as very unprofessional.

5 Likes

Some red flags I saw in the latest AR:

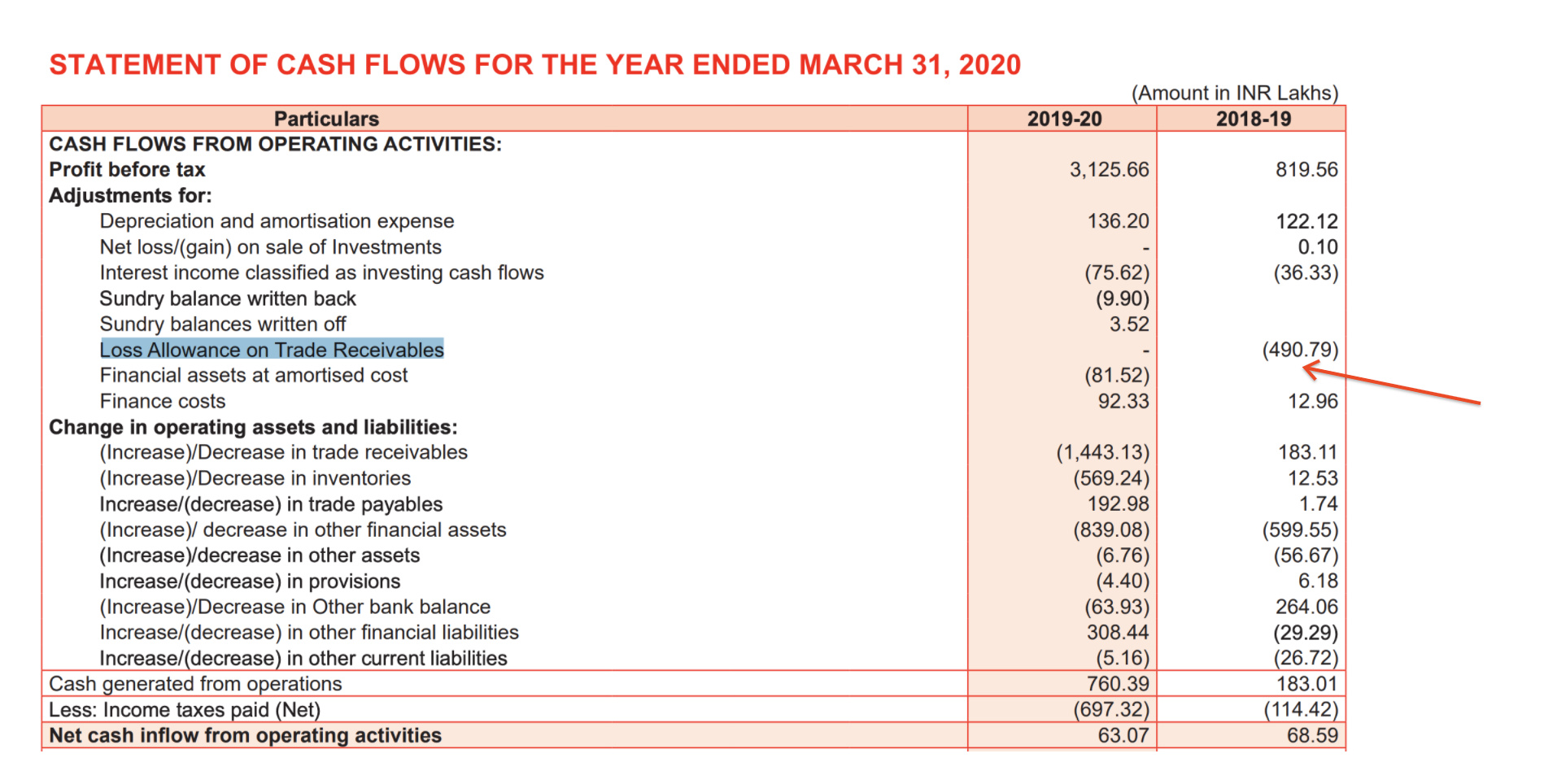

- The cash flow from operations has been very weak even before the change in business model. Hence, the low cash flow cannot be attributed to the change in business model.

In 208-19 the company wrote off 5cr of trade receivables which was major source of difference between PBT and CFO:

- The 2019-20 reduction in CFO is mostly due to receivables. Given the FY19 write off of receivables, we need to carefully monitor what happens to FY20 receivables in FY21.

6 Likes

Looks like they gave some concrete plans for future growth in the AGM hence they stock started flying post the AGM date. The stock-analysis by Pransejit Paul just mentions land-availability and adding new products, nothing specific, after 13:45 min in the youtube video. Though might also just be the PE catching up with the Q3 results anticipated (around 30% TTM PAT increase as per trend)

1 Like

The stock has broken out of a 28 year resistance recently …

1 Like

Good results https://www.bseindia.com/xml-data/corpfiling/AttachLive/f46a4853-80b6-44d3-9ce0-e3698fdfe8cf.pdf

2 Likes

Significant improvement in margin: QoQ, Sale: 74% NP=103%, YoY: sale, 65%, NP 608%.

High margins under the new business model seem to be stable, although there is possibility of competitive threat to the high margins in the future. At around 44cr PAT expected in a normal year without factory lockdown (like the previous quarter), the stock at around Rs 392cr market cap is trading at a low PE of 8.6, particularly given the company is one of very few big players in India in the fermentation processes. Any news related to the ongoing capacity expansion should further add to the valuation.

Disclosure: Invested

1 Like

Yes, biz seems to be stable, and risk of downside is low. Screener.in mentions PE as 10.4, further upside is dependent on the expansion plans. Though increasing realizations will sustain even better valuations, since it seems covid related effects are still there in the marginally lower topline, while OPM is at record level.

3 Likes

Plant shut down for repairs and upgradation from. Jan 2021

Gujarat will be temporarily shut down w.e.f. 5* January 2021 for an approximate period of 60 days for carrying out major repairs and up-gradation of the plant.

What is it being upgraded for?

capacity expansion & how much CAPEX goes into this, need to look for this infos!

From what I could gather from the internet …Gujarat Themis acutally has 2 plants …one in vapi and another in Hyderabad …I don’t know what’s the capacity of the Hyderabad plant though

2 Likes

I am guessing the revenue uptick could be explained by this apart from the business model shift. The surge came right after they commenced Rifamycin O production.

Source: Annual Report FY20

Rifamycin O is an intermediate for the drug Rifaximin used for the treatment of chronic GI diseases. It is a patent protected drug (innovator company: Alfa Wasserman) which Salix (subsidiary of Bausch) has the exclusive marketing rights for and is sold under the brand name “Xifaxan” having a fast growing market.

For Rifaximin API (and patent licensing), Salix has agreements with Alfa Wasserman, Lupin and Cipla, with an obligation to source at least 50% of bulk drug requirement from Lupin.

Source

The topline clocked by Salix for Rifaximin alone is more than the entire TB market size globally (as TB is more prevalent in under-developed economies with an infectious diseases burden) and the GI segment on a whole is growing at a faster rate led by chronic illnesses burden (IBS, etc) which is a developed economy issue.

Thoughts?

12 Likes

I think Lupin is not their client anymore. Who are the major clients now?

Also from which company Lupin is getting Rifampcin?

Last Budget gave a major emphasis on TB eradication. Coming budget will again focus on the same as they said TB eradication by 2025.

Rifampicin 150 mg, isoniazid 75 mg, pyrazinamide 400 mg and ethambutol 275 mg are needed for TB treatment.

Can anyone share the price trend of these especially Rifampicin and Isoniazid ?

4 Likes

Hey Nitin! What’s the source for the information about Lupin not being their client?

But the case in point is also that domestic Tuberculosis market (which Lupin and other domestic players cater to) has been on a decline despite the focus on eradicating TB.

Source

What do you think?

1 Like

I was on the opinion that Lupin is their client but in this thread it is mentioned that Lupin is not their client anymore. Please confirm the same if possible.

The article you shared if more than year old. We need to see current progress. GTB progress shows that demand is increasing, If I am not reading it wrong. I haven’t checked Lupin TB segment revenue. May be it will show latest progress on TB eradication front. If someone can help on these front -

1- Is Lupin still GTB’s client?

2- Latest price trend of Rifampcin, Isoniazid , ethambutol.

3- Lupin revenue trend from TB segment.

Thank you.

1 Like

Hi guys,

I’m fairly certain the recent revenue surge has come about due to Rifamycin O (Rifaximin).

Also, to get a clearer understanding about the product. Rifampicin and Rifaximin are themselves APIs. GTBL produces Rifamycin S and Rifamycin O which are used to make Rifampicin and Rifaximin, respectively. So, Rifamycin S and O seem to be API intermediates instead of APIs. I checked their old ARs also to get a product wise revenue detail (you may see FY15), it lists Rifamycin-S as the product generating revenues (not Rifampicin). Please correct me if I’m reading this wrong.

Now if they were producing the API itself and had to cater to the export market (regulated), they’d require quality compliance certifications (GMP, FDA, etc). But I don’t have much clarity on API intermediate regulations.

Why this feels important is that it opens up a very interesting field. India is heavily dependent upon KSM and API intermediates on China. More so for fermentation based. If GTBL can cater to the companies like Solara, Granules, etc. who are already selling Rifaximin API (Generic, not Rifamycin O), it could be potentially a very good opportunity.

So do you know the regulatory requirement for API intermediates for regulated markets? Can GTBL currently sell to companies targeting export markets?

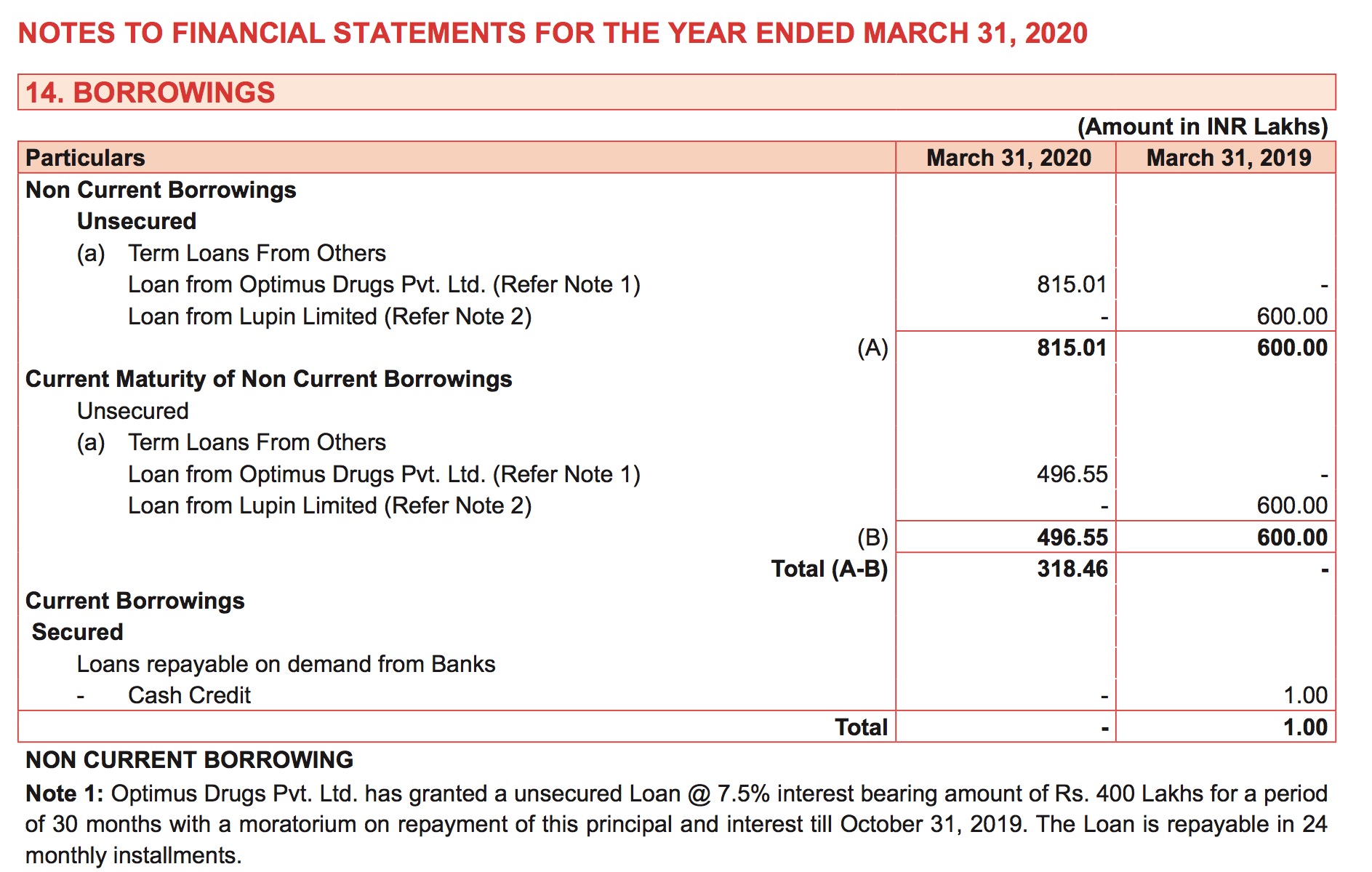

To reiterate the above, here is a leaf out of GTBL’s FY20 AR

You can see they have a loan from Optimus Drugs Pvt. Ltd. (the interest bearing amount and the difference between it and the total amount indicate it as sort of a soft loan with procurement interests in mind). The product list of Optimus on their website has both Rifaximin API as well as formulations. They have no presence in Rifampicin. So Optimus is a sure shot client. And the loan amount is also not a small amount considering GTBL just commercialised Rifamycin-O production. So they must have the volumes to supply to Optimus.

Another interesting point is that Optimus has a US-DMF for Rifaximin and is listed as a supplier.

Source

So if GTBL’s product can be used to manufacture Rifaximin API for regulated markets, it can be very promising considering the overall growth potential and potential of replacing Chinese raw material imports for domestic generic manufacturers.

15 Likes

A few observations:

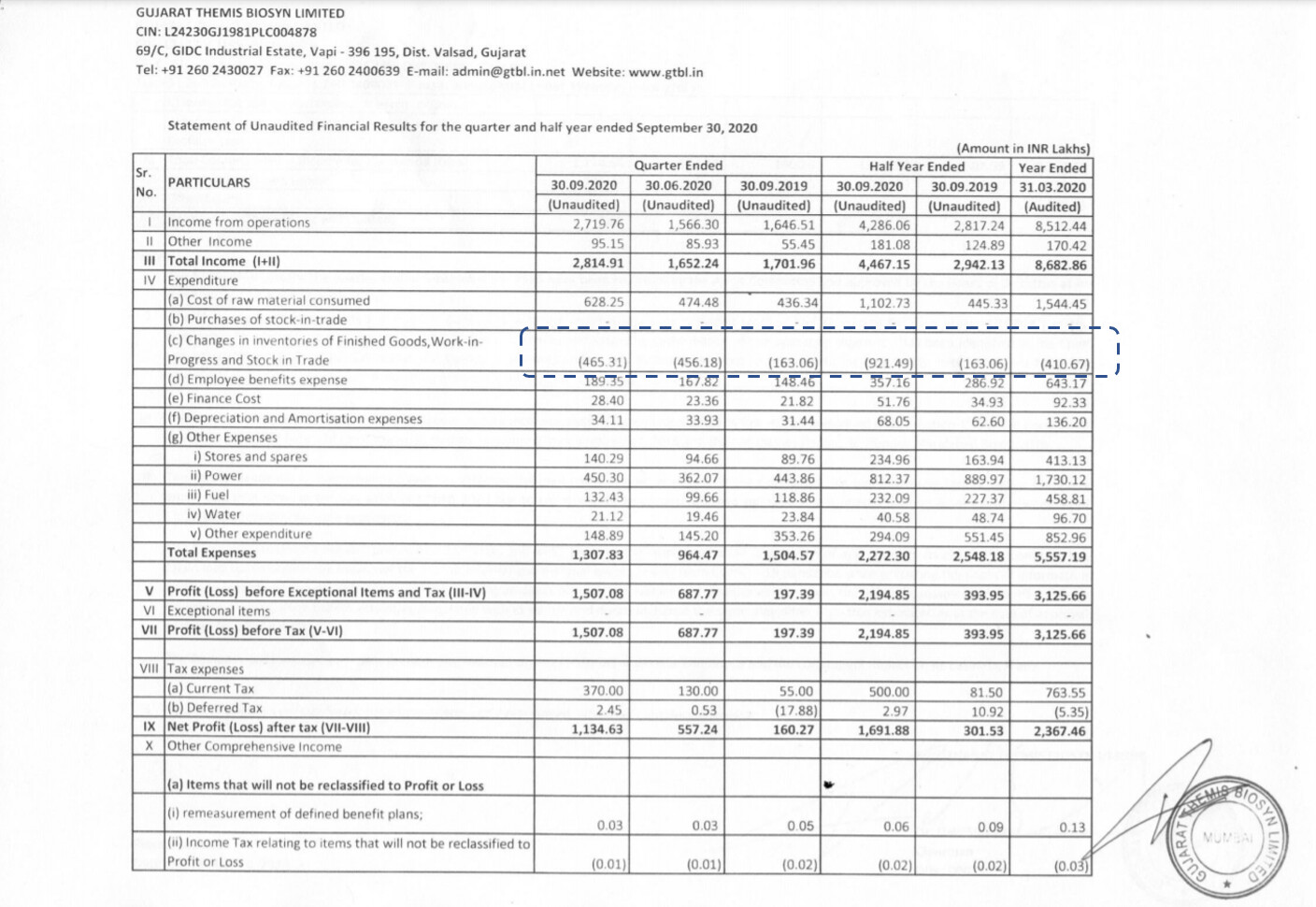

Company has been showing inventory gain every quarter from Sep 19 to Sep 20. Does anyone have more details on this? Jun’20 PAT numbers might have been very different if not for the inventory gain.

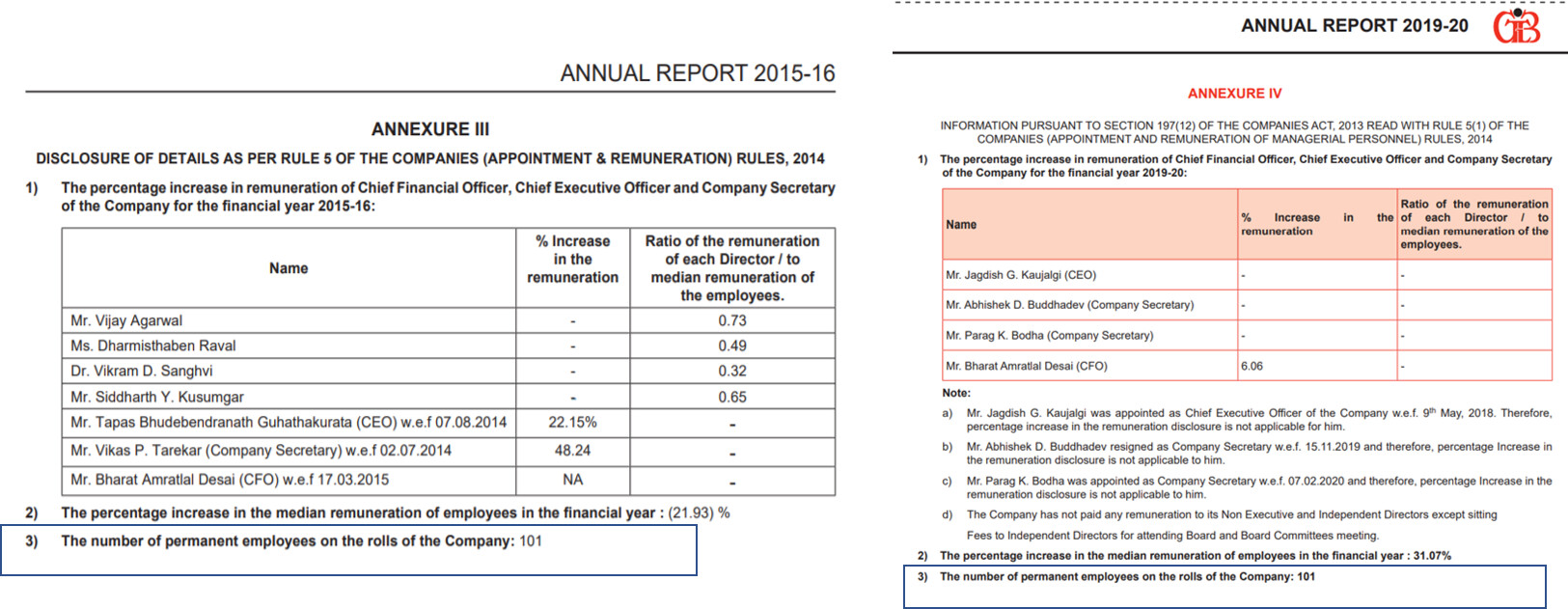

No. of permanent employees has remained the same for last 5 years = 101 . Found it a little unusual, considering that their business model has changed. Didn’t find any details on contractual employees.

1 Like