Makes sense, thanks for the clarification.

Do you also have any information on the receivables situation and inventory build up? Since the clientile is concentrated with Lupin being the main one, is this likely to put further strain on the receivables in the future? There is no management commentary or guidance available on any of this right

1 Like

Receivables are a concern, I have highlighted about it in my earlier comments.

Since earlier it was working with Lupin, receivables were less ( still the company had mentioned 4cr credit loss in 2018, which is concerning).

Now company has moved to B2C business and receivables have shot up.

2 Likes

Lupin is not their client anymore …

2 Likes

Since when have they stopped serving Lupin and without Lupin is the current revenue achievable?

2 Likes

According to new SHP https://www.bseindia.com/corporates/shpSecurities.aspx?scripcd=506879&qtrid=106.00

Plutus wealth management has picked up stake about more than 1%

1 Like

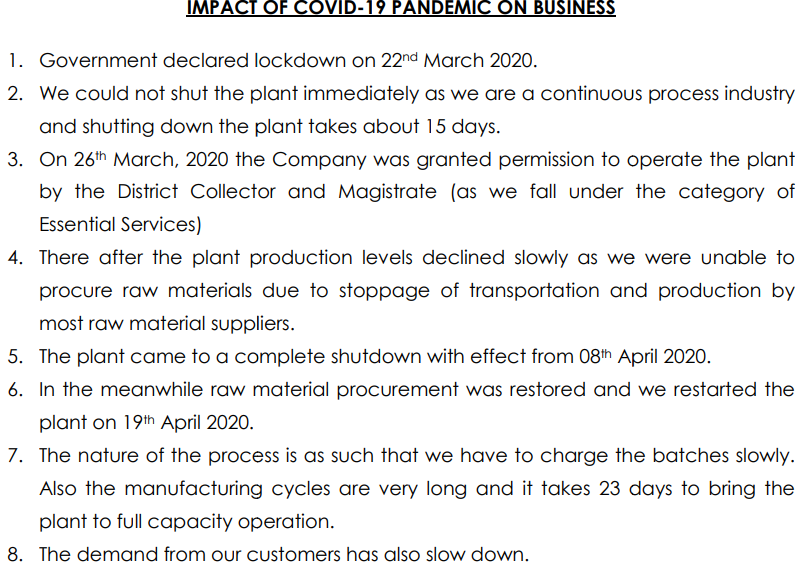

The Company has given update on Impact of COVID 19 on business. Main points are:-

-

The plant was operational between 22nd March 2020 till 8th April 2020. Though production level declined slowly on account of shortage of raw material

-

Complete shut down from 8th April 2020 till 19th April 2020

-

The Demand from customers has slow down.

Does the 3rd point above indicates a negative future outlook? Would be grateful if seniors could through some light on this.

Yes, seems like ~1 month of production was lost, and demand is low also. (but seems temporary slowdown only)

https://www.bseindia.com/xml-data/corpfiling/AttachLive/21ef8a4d-9f45-485f-be7e-d043810a6083.pdf

2 Likes

I was able to get in touch with one person from the company. .his number was listed in indiamart …he told me he’s in technical department of Gujarat themis …he told me that there’s no demand problem and that company lost about one month sales but things are back to previous levels and business is good …here’s his number if you are interested +919909928611

1 Like

Pretty decent results and on expected lines …hopefully things have normalised by now

1 Like

One of the big concerns was whether the company will be able to sustain its higher margins. I will assume the answer is yes although we cannot say with full certainty given the current results. Assuming the capacity expansion will likely be complete within a few quarters, this seems to be a good opportunity to enter for the long term. On the flip side, it is possible that capacity utilitization may drop or be delayed due to Covid.

Disclosure: Tracking.

1 Like

Rifampicin is one of the anti-biotics listed by Indian govt. in PLI scheme, fermentation based APIs are the biggest Chinese imports, accordingly PLI offers biggest incentive to fermentation. If anything Covid should provide even bigger positive for this company.

Negative is the smallish scale and management. Almost no pharma company was affected much by lockdowns, while they had the production cut in half!

Disc: invested

2 Likes

A fair comparison will be with peers in fermentation. Disruption in production may be due to the nature of the manufacturing process. As the company said, 23 days were needed to bring the plant to full capacity operation.

They may have long-term contracts for raw materials to reduce costs, which were not available due to the force majeure of Covid. Having said that, hopefully, the management will improve the procurement of raw materials after learning from this episode.

Overall, the company has three big pharma-based promoters. So, the management is expected to be professional.

2 Likes

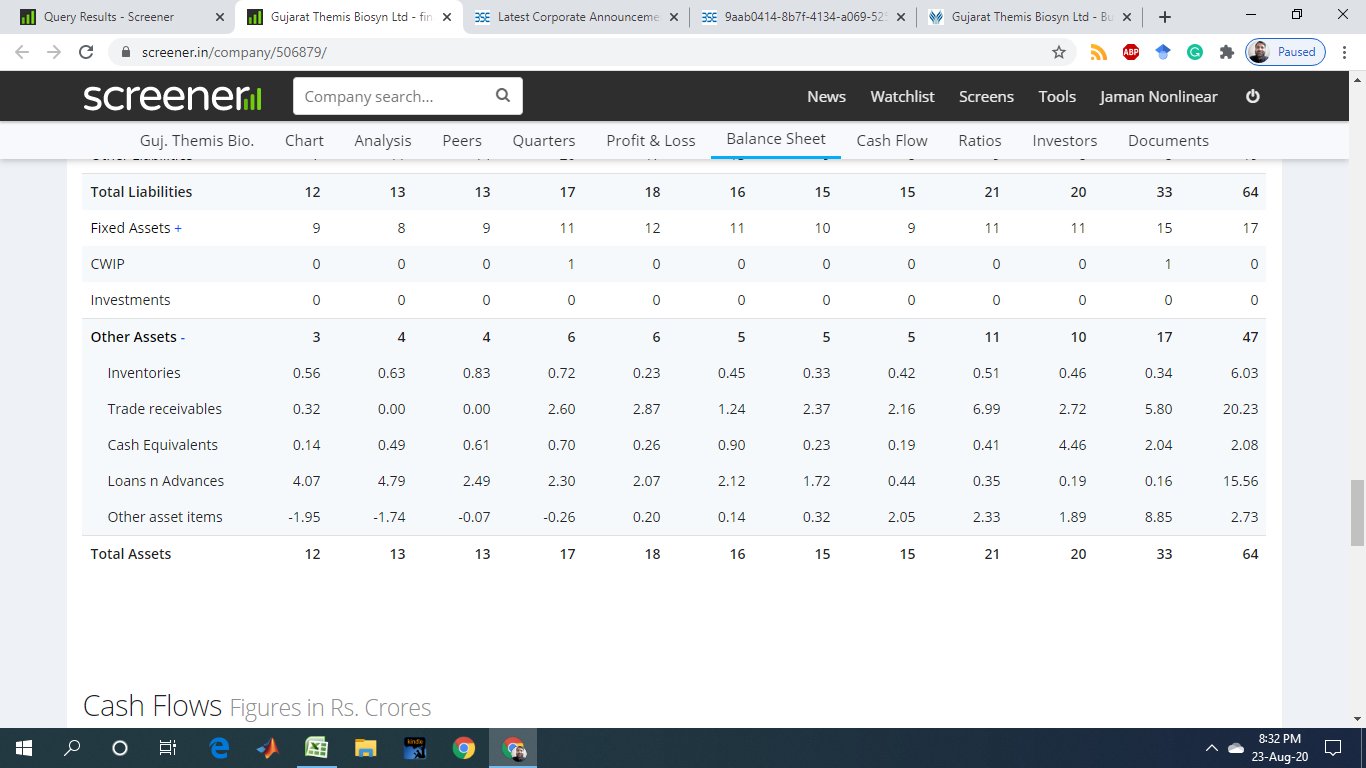

When I was analyzing G Themis Biosyn [

], I found,they have given loan/advance of Rs. 15.56,a huge amount compared to the previous year. Why they are giving such amount of advance and to whome?

@vikas_sinha,

@kalidasa. Further though the net profit increases, cash is at same place?

1 Like

The item you mentioned is registered as “Other non-current financial assets” in the balance sheet. Will have to ask the company for details.

Roughly speaking, it is the likely part of the normal business flow, so on one hand they are having ‘Trade Receivables’ of 20.23 Cr as amount to be recovered from sales made and on the other side they have paid in ‘Advance’ 15.56 Cr to their vendors for raw material.

Together they account for 40% of the overall turnover of 90Cr, seems bit on the higher side but maybe reasonable for their kind of biz.

Tried to capture some relevant excerpts from AR 2019-20:-

- Commercial production of Rifamycin O started in September 2019 on the basis of technical input provided by Themis (Rifamycin O is an intermediate for manufacturing the drug Rifaximin (Antibiotic used for treatment of traveler’s diarrhea, irritable bowel syndrome, and hepatic encephalopathy)

- GTBL is in the process of identifying products which have good domestic and export potential. The Company also has plans to establish a new R&D lab to take care of technological developments for new products that are being identified for global markets.

- Change of business from contract manufacturing to manufacture and sell

- Company recorded an increase in sales of 107.37 % from Rs. 41.05 cr in FY19 to Rs. 85.12 cr in FY20. The full year performance can be hugely contributed to the change in our business model and manufacturing of new products. The EBIDTA also shows a drastic improvement of 334.21% to Rs 31.84 cr, due to increase in revenue. The Company registered 269% increase in net profit from Rs. 6.41 cr in FY19 to Rs. 23.67 cr in FY20.

- Board approval for increase in limit for Related party transaction and borrowing power

- During the year Company has introduced ESOP schemes for employees

- Proposed dividend of INR 1.65

- Risk & Concern - The government policies are creating new risks for domestic market by including new molecules to the price control umbrella and also the issuing ban on various Fixed Dose Combinations

- Observed that the salary cost of KMP is on lower side

Link to Annual Report https://www.bseindia.com/xml-data/corpfiling/AttachLive/2550bbe6-0b94-4ff3-858d-7852eb63eff6.pdf

4 Likes

The government policies are creating new risks for domestic market by including new molecules to the price control umbrella and also the issuing ban on various Fixed Dose Combinations.

I believe this is a major risk going forward. The economic state of the govt is very poor after sub-5% GDP growth even before the Covid outbreak. Recently, the center failed to fulfill its GST compensation payment towards the states. The next few months are going to highly challenging with Covid and will incur a lot of expenses. India may be going through the worst economic crisis in the last 4-5 decades.

Given all this, it can be expected that the government will impose price controls on more medicines in order to reduce its financial impact. The outcome will be counterproductive, but has to be expected given the track record.

2 Likes

Could someone explain conversion charges from the Anual Report?

Your Company’s major operations were from Sale of finished products. During the period, sale of finished products recorded at Rs. 6769.19 Lakhs (previous year Rs. 107.75 Lakhs) registering increase in sale. The Company also earned Rs. 1782.50 Lakhs (Previous year Rs 3,982.61Lakhs) from conversion charges during the year ended 31st March, 2020.

1 Like

This should be the leftover from the previous model of operations, contract manufacturing, where the raw material was supplied and all finished products taken by the out-sourcer, GTBL only was paid the conversion charges by this sourcer (Lupin).

Now they have started showing RM purchase and Finished product sales figures, so several metrics show a big jump (trade receivables and payables etc.)

IMHO, Indian drug price control is among the weakest in the world, it was common knowledge to buy domestic focused pharma companies, since their margins were much superior to the exporters.

The price control policy mostly consists of averaging market price of certain formulation/molecule and then establishing a ~30% price band upon this market discovered price, which no brand can violate.

There is no way any govt has the spine to control the drug mafia. Your doctor will simply brow beat you into buying top-dollar branded stuff though much cheaper generics may be equally good, case in point is one of the market darlings.

The concern on price control is nothing new. Besides AR 2020, AR 2019 and AR 2017 also has the following sentence:

The government policies are creating new risks for domestic market by including new molecules to the price control umbrella and also the issuing ban on various Fixed Dose Combinations.

AR 2018 says:

The Industry continued to face challenges due to imposition of price controls and bringing many

products under the ambit of National List of Essential Medicines.

Drug price control has been counterproductive:

Government interventions to regulate prices of essential drugs have led to hike in their cost when compared to unregulated similar drugs instead of making them affordable, according to the Economic Survey for 2019-20.

The analysis of the Essential Commodities Act (ECA) clearly shows that stock limits and price controls under the Act lead to sub-optimal outcomes which are actually opposite to what the Act is mandated to achieve, it added.

It seems that drug price control is really a serious, ongoing concern in the pharma sector:

The current drug price control policy has had many unintended consequences. For example, many pharmaceutical companies have opted to go out of production because their profit margins decreased. This has led to substandard and spurious drug manufacturers dominating the pharma market. In the absence of strict quality regulations, there has been a trade-off between price and quality; a report by the United States Trade Representative claims that 20 per cent of drugs in India are fake. Decrease in profit margins of quality manufacturers has led to a reduction in spending in research and development. It has deterred future investments in the pharmaceutical sector.

Many manufacturers migrated to non-essential drugs (80 per cent of the drugs in non-essential list) or stopped promoting essential drugs.

But, it seems the government is doubling down on price control. Below are a few articles in this regard:

3 Likes