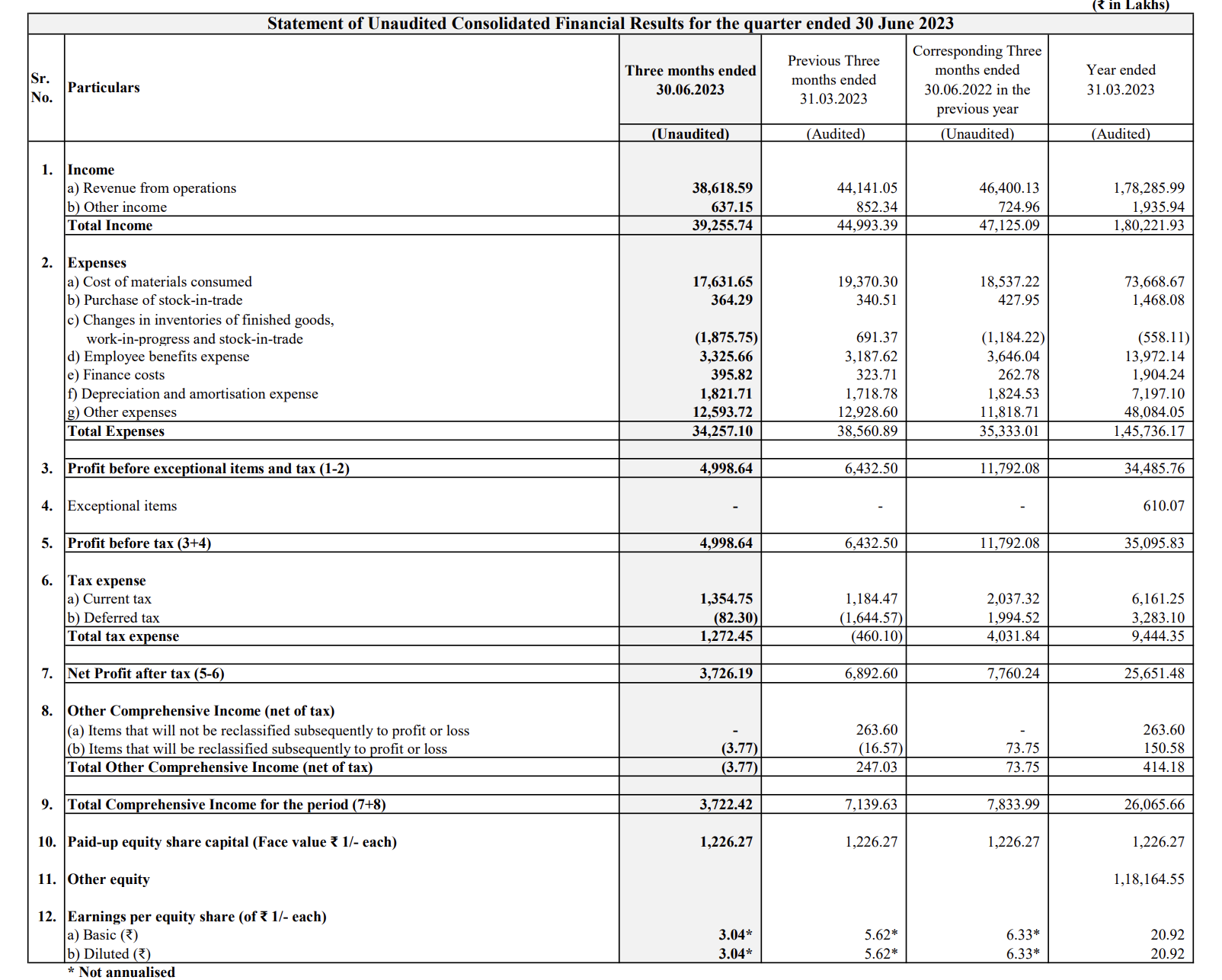

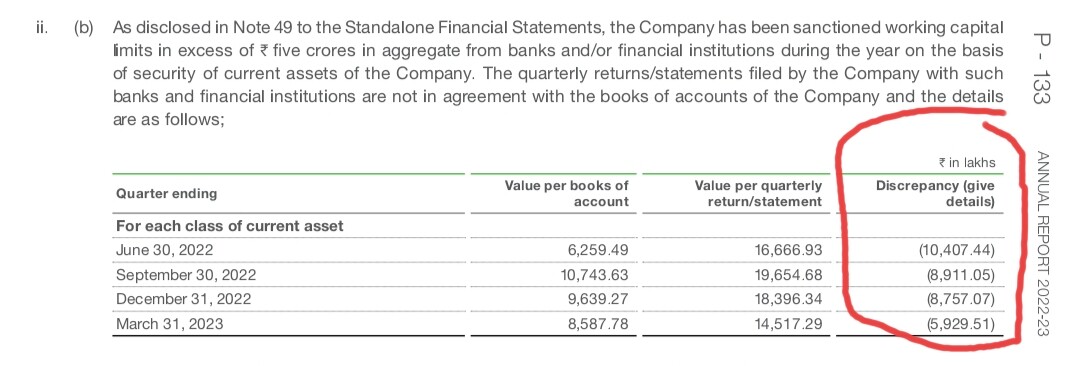

In the AR 2022-23, the statutory auditor remarked that the quarterly returns filed by the company with banks were not in agreement with the books of accounts.

Discrepancies are huge as shown below:-

Is it something serious?

4 Likes

This item does appear in sometimes but here the amounts are on the higher side. Note 49 on page 243 gives the reasoning but it still does not explain fully the root cause. I think it is better to write to company and ask why the quarterly returns submitted to the bank are not in accordance with Ind AS 115 and what the company plans to do about it. You can also register as a speaker at the AGM and ask the question. Note that this item was there last year also but not there in FY21. So what changed in FY22? It might be due to some process change or software related reason. You can ask what the company plans to do to align the two in future.

3 Likes

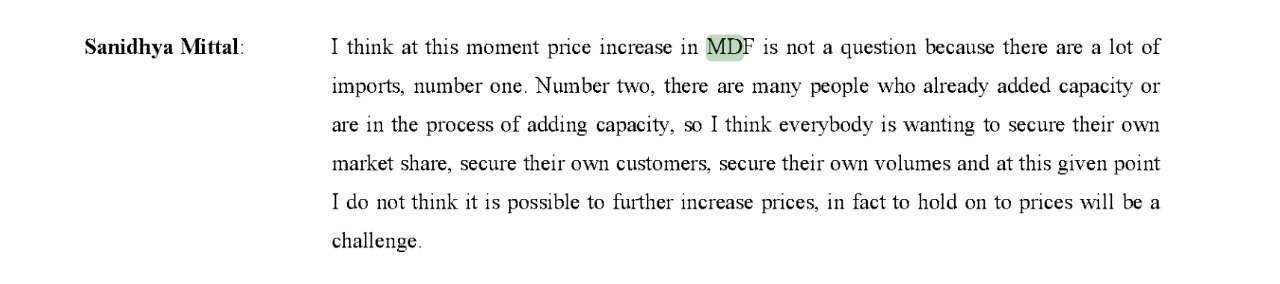

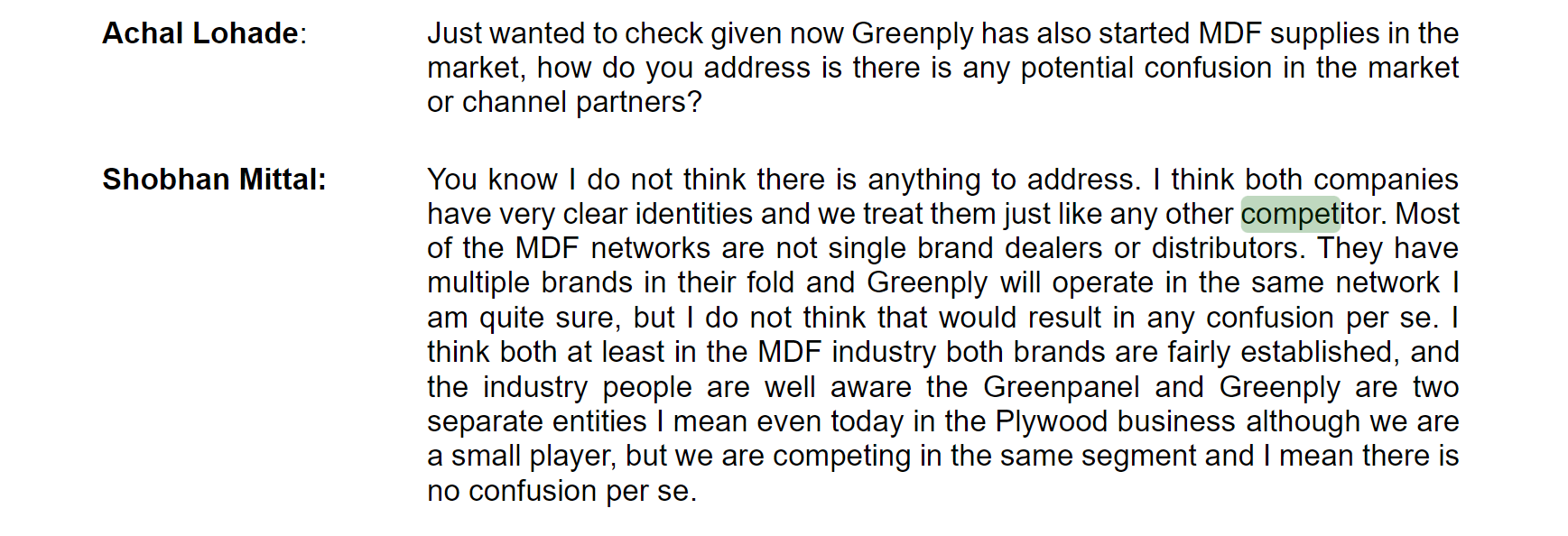

This is actually a big anti thesis/risk for this I was under the impression, read recent concall of greenply they have installed a plant for MDF and are also selling 2-5% cheaper. Thought after demerger greenpanel would be exclusively focused in MDF but seems like family is competing with each other in same line of business so margins will not increase.

1 Like

I just listened to the Q3 2024 call. Management is strongly expecting that BIS implementation will deter imports atleast in a short term. But then, Capacity seems to be ever increasing which would result in price pressure. Green ply getting into MDF is not good (although it was not discussed).

My original thesis buying this Share was that housing growth will help. Elevated wood prices will help. And I liked the fact that they are very concentrated in MDF and have a Capacity built in for 2-3 years growth. I still believe in this thesis BUT wondering whether they can ever establish a good enough Brand Equity to sustain price and grow above industry average.

Appreciate any thoughts.

1 Like

I exited this stock after finding that the no competence contract is no longer valid and also that greenply is doing capex and is also selling at 2-3% discount to gain market share, I feel there is no MOAT and I am bullish on the housing and MDF sector but then I think it could be a commodity with no real pricing power.

5 Likes

Just found this, thought of sharing it over here. Need to wait another fortnight for this BIS norm to get enforced. The management was talking big in the last 2 concalls regarding this. Let’s see!!

Ref:https://www.bis.gov.in/upcoming-qcos-notified-and-due-for-implementation/

Disc: Invested

4 Likes

This got implemented correct ?

1 Like

Lot of news saying its been delayed to Feb 2025

2 Likes

Well, results are bad and their half hearted guidance of 15% volume growth in FY25 is not very convincing either. IF real estate is doing well, wouldn’t these companies do well? Is it a matter of losing market share because of over capacity or just weak demand? Any thoughts?

1 Like

I agree with that results for FY24 were really poor. All guidances given by the management at the start of FY24 blown away. Feels like the products are commodity kind of, and there is over capacity through imports, as such margins n volumes are very much lower than the estimates given.

This stock has been rising off late despite poor results.

Thoughts on Greenpanel Industries ?

Personally i feel home decor is a sector to watch out for in the coming years.

I’m also confused for why it is rising despite poor results. One thing mentioned in the concall is that the prices are at their bottom, and they don’t expect any big fall further since all major capacities are live now.

3 Likes

People are expecting that prices had bottomed out, or on ground prices increase may have started already.

In my opinion we should wait for few more quarters as all new capacities also coming on stream, this could increase supplies more and drag the price down.

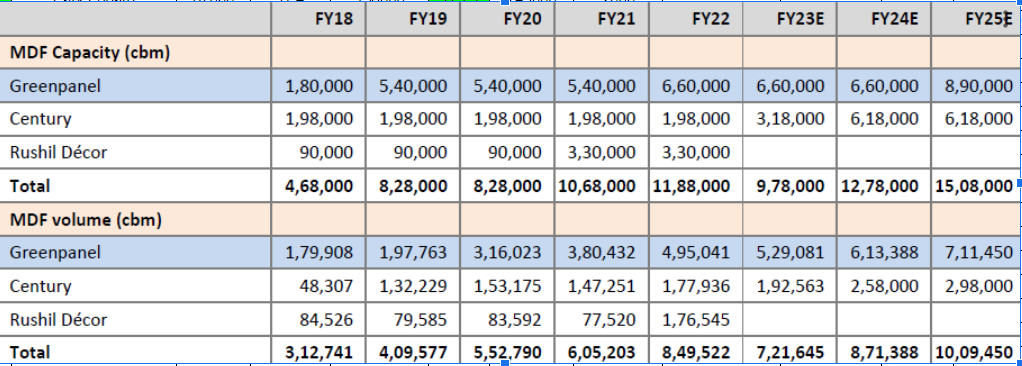

Below is the old capacity expectations from a report. I am not tracking GP closely now a days, will look for any entry once prices start recovering

9 Likes

I have started adding small quantities of Greenpanel based on their latest concall.

The management in its latest concall highlighted the following points which gives me confidence to add this in PF.

- MDF prices have bottomed out.

- Unorganised players in trouble and do not have pricing power anymore due to rising timber prices.

- BIS norms for MDF to be implemented in Feb 2025 will further weed out unorganised players

- Imports are gradually reducing.

- Company has reduced its long term debt which has significantly bought down its interest costs.

2 Likes

Yes. They have been saying this for quite some time now. Let’s see what how September quarter results turn out to be. Have added very small quantity based on their latest concall as well as technical charts.

3 Likes

September 2024 quarter results declared. Sales down 15.5% y-o-y. Sharp contraction in operating margin. Sequentially, the contraction in operating margin in just 40 basis points. Let’s see how price reacts.

2 Likes