Any update on the imposition of CVD on MDF boards with thickness less than 6mm? Management had commented in Q1 call that they were expecting positive news on the CVD imposition by August latest, but there was no mention of this in the Q2 or Q3 calls.

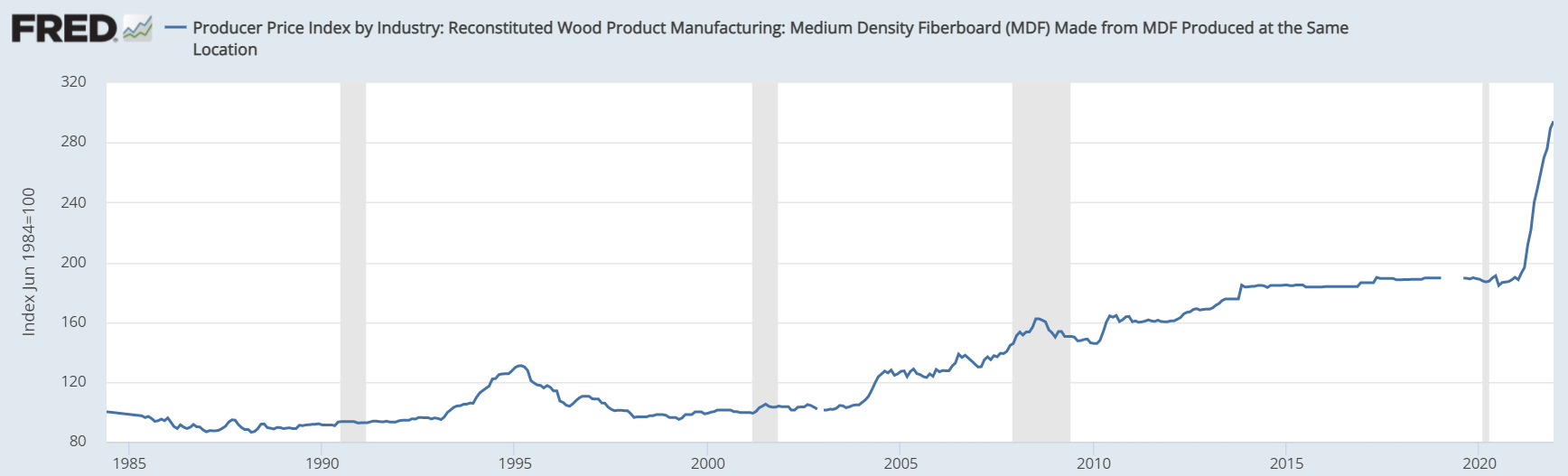

US PPI index shows how global MDF prices shot up since Dec 2020. Index is now at ATH value of 294 (Dec 2021). As long as these prices remain elevated, domestic players’ realizations will remain elevated.

3 Likes

5 Likes

Today Greenpanel reported good set of numbers for Q4-2022 and FY2022. Some comments/observations

1- Net Sales of MDF for Q4-Fy22 was 390 crores vs 302 crores in Q4-2021. Ebitda margin was 34.60% vs 28.60%.

2- Net Sales for Plywood for Q4-2022 70.5 crores vs 83 crores in Q4-2021. Ebitda margin reduced from 15.5% to 9.2%.

3-For the full year FY2022 Net Sales of MDF was 1330 crores vs 784 crores in FY21. Ebitda margin in Fy22 was 31% vs 23% previous year.

4- For the full year FY2022 Net Sales of Plywood was 256 crores vs 217 crores in FY21. Ebitda margin in Fy22 was 11% vs 12.4% previous year.

5- Net Debt reduced to 60 crores from 375 crores at the end of FY2021. Gross debt is reduced to 283 crores from 447 crores at the end of FY2021.

Future possibilities and commentary

1- Company expects to be net debt free by the end of current quarter which is Q1-FY2023.

2- Capacity of MDF stands enhanced to 660K CBM. I expect the utilization to gradually go to close to 100%.

3- MDF is gaining market share from Plywood. Current distribution is 80% Plywood and 20% MDF. Large opportunity for MDF to keep taking share from Plywood.

4- Company has established itself as the largest MDF player in India and focused on keeping it intact.

5- In my opinion company could do roughly 2100 crores of Sales in FY2023 unless some big negative event would happen. Company can keep the Ebitda margin at 27% which translates into Ebitda of 567 crores. With Net Debt going to zero the interest cost for working capital of about 220 crores would be roughly 26-27 crores. Depreciation would be roughly 80 crores. This translates into PBT for FY2023 to 460 crores. Applying Tax rate of 31% the PAT for FY2023 would be 317 crores.

6- With expected 317 crores of PAT (from “5”) for FY2023 the EPS would be 26. At CMP the of 570 the stock is quoting 22 times on forward earnings which seems reasonable for a net debt free company with industry tailwinds.

Thanks,

Krishna

PS: I am not a SEBI registered analyst. This is not a buy or sell call. I have strong ownership bias.

9 Likes

What is reason behind resignation of independent director?

Disc: I am invested in it.

What’s surety for supply chain integrity for raw material for Indian plywood / MDF / Panel board companies? So much expansion coming in India from these industries and mostly raw materials coming from outside India…what is risk on raw materials supply for these Indian companies. Can you please give more details on sourcing of raw materials for these industries

Good quarterly results were posted by Greenpanel

A company like Greenpanel with reasonable market share, good EBIDTA margin and good return on capital in a fast growing industry is trading at this valuation. What is amiss here?

2 Likes

UPDATES

- Revenue growth of 11.66% year-on-year in Q2. MDF segment saw revenue growth of 17.8%, while plywood revenue saw degrowth of 16.6%, although volumes were subdued.

- MDF gross margins improved by 205 basis points.

- PAT is up by 8.05% year-on-year to INR 72.46 crore

- Made advance payments of INR 30.5 crore during Q2 against expansion project.

- For FY2023, we are guiding for 12% volume growth for MDF in the domestic markets, although export volumes are expected to be flat.

- Long-term sustainable margins will be around 27% to 28%.

- Management is looking to increase in marketing expenditure from 1% to 2.25%.

- Exports will be a challenge due to multiple reasons - one of them being replacement of China by Vietnam and Indonesia as furniture exporters to the U.S. and Europe ence in the landed cost of the imports versus the domestic realization. – 8 to 10% cheaper to import

- Difference in the landed cost of the imports versus the domestic realization. – 8 to 10% cheaper to import

- Don’t see any further inflation in raw material prices. Margins should be maintained from the current level

- Topline target between INR 1,900 crore to INR 1,950 crore (mgmnt had guided 2000 earlier)

- At present, domestic capacity in general for whole India is around 2.3 million cubic whereas demand 1.9 million cubic. The trend will continue as more players are putting capacities - despite this management seems confident to maintain margins

- Will be investing approximately INR 600 crore over the next 18 to 20 months on the expansion projects. Will not be having any surplus cash flows up to FY24.

- Currently exploring other business opportunities, but they are at a very infancy stage.

- Management mentions that expiration of anti dumping duty is challenging along the coastal areas BUT not inwards due to freight costs.

-

Comment on future margins as compared to competitors: Rushil’s margins are closer to us and Rushil’s margins will be lower due to a mix of lower pricing and lower capacity utilization.

- Winding up of the Wholly Owned Subsidiary; M/s. Greenpanel Singapore Pte. Ltd.

7 Likes

Updates:

- Looks the last remnants of demerger are clearing up as the management has now shifted the office.

- I also wanted to clarify what date does the management prefer to disclose the quarterly result (second point).

Have always found their responses timely, simple and crisp. I really like this management.

3 Likes

Margins will shrink further as management told that they will boosting exports due to low demand in domestic market, further correction is expected

3 Likes

If prices are higher in the domestic market than export, why not sell in the domestic market even at lower price? If prices were higher in the export market, the Vietnamese and Indonesians would sell there rather than export to India, wouldn’t they? What am I missing here?

I think, to sell more in domestic, they’d have to drop their realisations. Most of these sales are not to end consumers (OEMs who make furniture) but to their channel and beyond a volume dealers/distributors won’t stock up without heavy discounts. And that sets off an escalating price war in the market because competitors don’t want to lose any market share.

From what I’ve read in concalls and what I know of commodity pricing in building materials, Greenpanel are the price leaders in the domestic market for MDF and the other players benchmark themselves against their pricing. If they drop prices the whole market follows suit and realisations and profits for the whole industry will suffer.

10 Likes

I am relatively new to VP. I have been mostly reading others views / opinions. Given all the pros/cons of the company, I am wondering if any of the existing investors see the current price levels as a good starting entry point. I have been following the company for the last 2-3 quarters but was hesitant to invest given the sharp decline recently.

Given the market leadership position, early stages in MDF usage in India (potential industry growth CAGR 15-20%), current valuation, expansion plans, Management execution track record, etc… seem to make a strong case to enter the stock if one has a long term view (3-5 years).

Any thoughts/comments on this are appreciated.

Thanks,

Bhanu

1 Like

Mine case is same as yours, been tracking for last month or so about this company.

I have one chief concern. The competition from other alternatives to MDF - plastics products, ceramics, tiles, plywood etc. There so so many options. How many people would prefer MDF over others would be main deciding factor.

1 Like

Talking about woodpanel space,

MDF is more viable then plywood also it is cheaper then lower end of plywood.

People are preferring ready to use furniture in urban areas

3 Likes

wait for few more quarters, Domestic demand should come back for good results

24022023122649_Medium_Density_Fibreboard_CareEdge_Report.pdf (133.1 KB)

Care ratings report on MDF industry.

Growth for sure, but margins to be impacted.

2 Likes

I have done analysis on this company and below are the details. Some parts which were previously discussed are left out.

Business

Largest MDF manufacturer in India with around 28% share. Future betting is that India will move away from Plywood to MDF just like rest of the world. The trend is visible in online sales and how young people give importance to looks.

Financials & Covid

Company has taken loan in dollars internationally for expansion in southindia. Strengthening of dollar, post covid has impacted margins. Revenues were growing consistently but 2023 was flat because.

- Due to slow down in global market, Thailand, Vietnam dumped MDF into india at cheaper rates.

- Other players in the market were also increasing the capacities.

P/E

On websites or screener, you would see the P/E is 16. In correct words the P/E shown there was 12 month trailing P/E that means 3 bad quarters with around 50 Cr profit and one good quarter with around 110 Cr profit.

It is clear that above mentioned 2023 conditions are going to continue until 2025. In simple words, if you calculate future P/E with 50Cr profit in future quarter, P/E will be around 25-sh. Because business conditions will not change and this is going to be the normal profit.

Management

So far from the reports, i found management to be responsible, caring about small shareholders, trying to use debt carefully. Overall i feel a 5 star management here.

Moat of the company

I could not think of any strength which can be called moat. For example, It might not take a long time for Century Ply to invest into MDF and use its own distribution network to sell much more effectively. Note that Green panel has to create Distribution network and work on branding. But Century ply etc might not be. Yes, entry is difficult for new industries due to investment etc etc, But if really trend is turning towards MDF from Plywood, it would just take 3-4 year for other companies to catch up.

Conclusion

I liked the management and their direction, but MDF market has to be created or transferred from plywood. I believe MDF is a future but who will emerge as a winner is difficult at the moment. For me any plywood company can easily venture into MDF and use their network and customer reach etc.

So waiting for better business conditions and see if GreenPanel can actually emerge as a winner.

8 Likes