1. Introduction: What Is Green Hydrogen?

Green hydrogen is hydrogen produced by splitting water (H₂O) into hydrogen and oxygen via electrolysis, using electricity generated exclusively from renewable sources (e.g. solar, wind, or hydro). Unlike conventional “grey” hydrogen (made from fossil fuels without carbon capture) or “blue” hydrogen (grey hydrogen with carbon capture), green hydrogen has no associated CO₂ emissions. This clean energy carrier is viewed as a critical enabler for decarbonizing heavy industry, balancing renewable energy grids, and transforming transport.

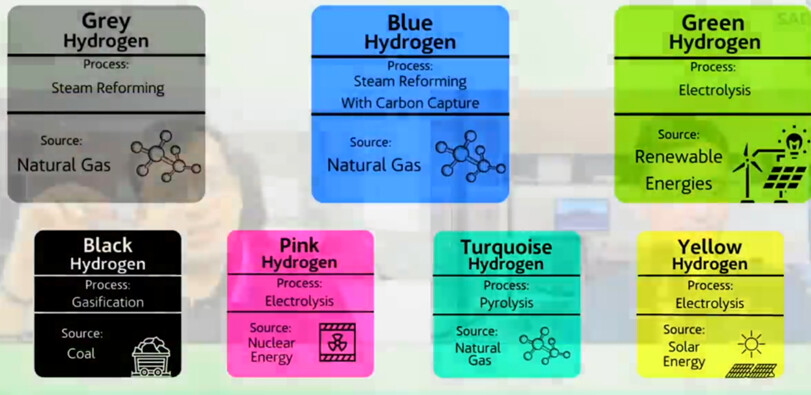

Besides green H2 there are other types of H2 also:

How Is It Produced?

- Renewable Electricity Generation:

Electricity is generated by wind farms, solar parks, or hydropower plants. - Electrolysis Process:

An electrolyser splits water into hydrogen and oxygen. Common technologies include alkaline, Proton Exchange Membrane (PEM), and emerging solid‑oxide electrolysers. - Post‑Processing:

The hydrogen is purified, compressed (or liquefied) for storage, and then distributed via pipelines, trucks, or ships. - Value Chain Overview:

- Input: Renewable energy and water (often pre‑treated).

- Electrolyzer manufacturing & Conversion: Electrolysis producing hydrogen and oxygen. Larsen & Toubro leads domestic production through JVs, targeting 5 GW annual capacity by 2027. Although there are various way to manufacture elctrolyzer, alkaline method is the most prominent one.

- Processing & Storage: Compression, liquefaction, or conversion into derivatives (e.g. ammonia). Hydrogen must be purified to 99.97% for industrial use. Bharat Petroleum (BPCL) collaborates with BARC to develop alkaline electrolyzers, targeting 1,000 MW capacity by 2027

- Distribution: Transport via pipelines or logistics networks.

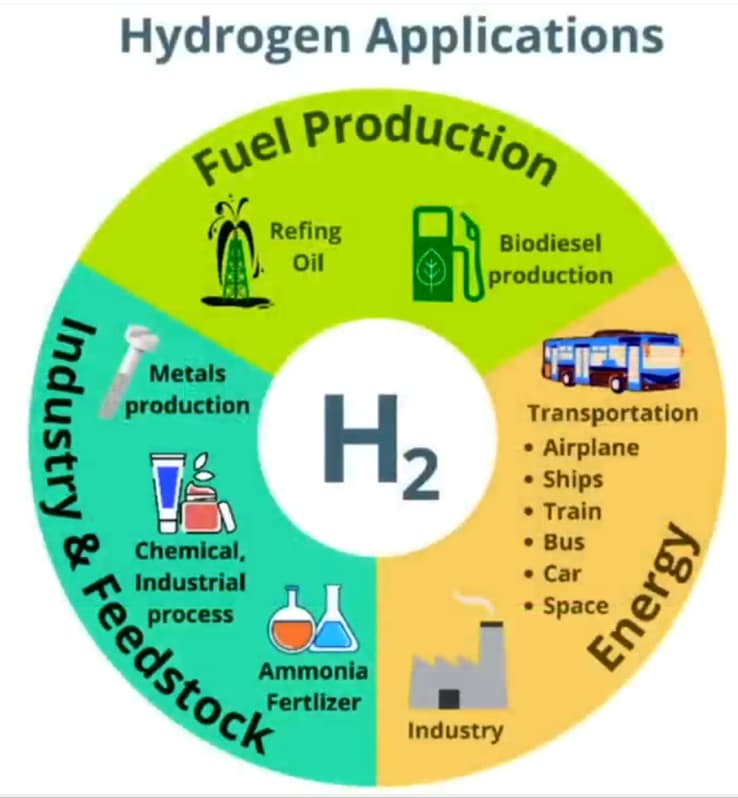

- End‑Use Applications: Power generation (for grid balancing), fuel for heavy‑duty vehicles, industrial processes (green steel, fertilizers, chemicals), and blending into natural gas networks

2. Why Green Hydrogen Matters: The Big Picture

Why do we need it while there are cheaper alternatives (like solar, wind) is available:

Solar, wind, and other renewables are essential sources of clean electricity, but green hydrogen serves a different and complementary role in the energy system. Here are a few key reasons why we need green hydrogen:

Energy Storage & Grid Balancing:

Unlike electricity, hydrogen can be stored over long periods and transported over long distances. This makes it a valuable way to store excess renewable energy during periods of low demand and release it when needed, helping to balance the grid.

Decarbonizing Hard-to-Electrify Sectors:

Certain industries—like steel, chemicals, and long‑haul transport—face technical and economic challenges when trying to switch directly to electric alternatives. Green hydrogen can serve as a low‑carbon feedstock or fuel in these sectors, where direct electrification is impractical.

Versatility in Applications:

Green hydrogen can be used in fuel cells for vehicles, as a raw material in producing green ammonia for fertilizers, or even blended into natural gas networks. This versatility helps reduce emissions across multiple parts of the economy.

Utilizing Surplus Renewables:

In many cases, renewable energy production (especially solar and wind) can exceed immediate demand. Converting surplus electricity into hydrogen can prevent waste and provide a storable, transportable form of energy.

Environmental and Economic Imperatives

- Decarbonization:

Green hydrogen can replace fossil fuels in industries that are difficult to electrify, such as steelmaking, chemicals, and heavy transport. For example, using hydrogen in the Direct Reduced Iron (DRI) process for steel production can lower CO₂ emissions by up to 95%. - Energy Storage & Grid Balancing:

Green hydrogen acts as a long‑term storage medium for excess renewable energy. In times when wind or solar output is low, stored hydrogen can be reconverted to electricity to stabilize the grid. - Industrial Feedstock:

Hydrogen is an essential ingredient for ammonia used in fertilizer production. Transitioning to green hydrogen reduces the overall carbon footprint of the chemical industry.

Proxy Industries Benefiting from Green Hydrogen/Application of Green H2:

Investing indirectly in green hydrogen can also be achieved by targeting industries that stand to gain from its adoption:

- Renewable Energy Developers:

Lower renewable electricity costs are key to reducing hydrogen production costs. Indian companies like Tata Power and Adani Green Energy are expanding their renewable portfolios. - Engineering and EPC Firms:

Companies such as Larsen & Toubro (L&T) have the expertise to build electrolysers, storage systems, and distribution infrastructure. - Heavy Industries (Steel, Chemicals, Fertilizers):

Firms like Tata Steel can benefit by adopting green hydrogen for cleaner production methods. - Fuel Cell and Transportation Technology Providers:

Companies developing fuel cell systems for heavy vehicles offer niche exposure to the hydrogen value chain.

3. Opportunity Analysis

Growth Projections and Market Trends

- Global Market Outlook:

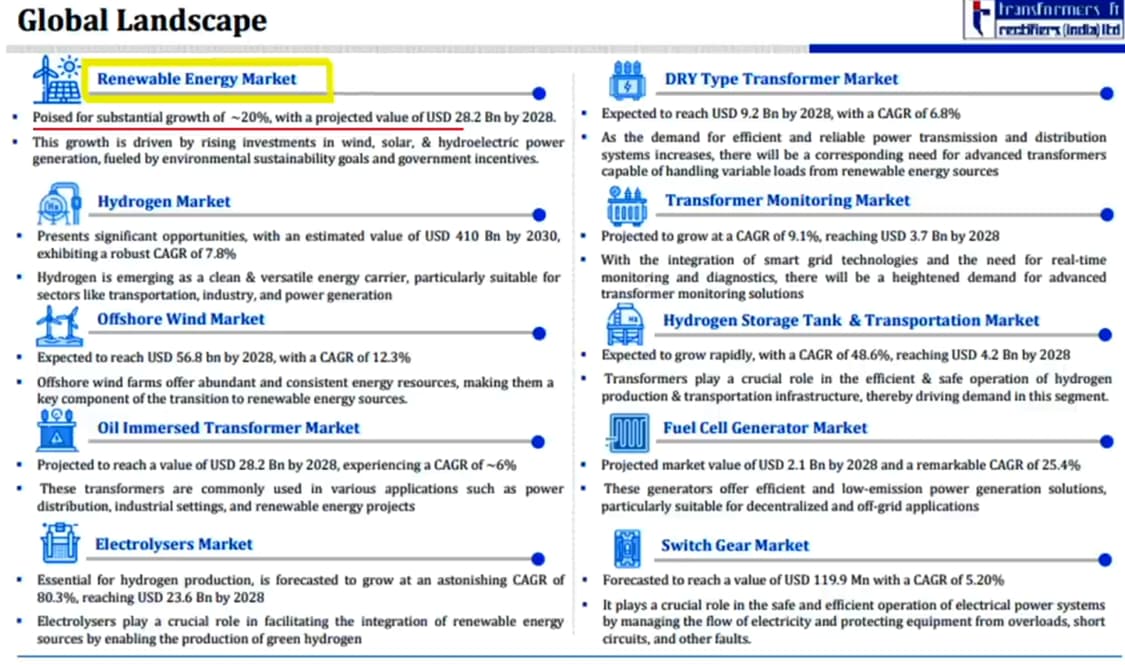

Research estimates the global green hydrogen market could grow from roughly USD 7–8 billion in 2024 to anywhere between USD 60–200 billion by the early 2030s. Some studies (e.g., MarketsandMarkets) predict a CAGR in the range of 60% or more. - Cost Reductions:

Electrolyser costs have fallen dramatically (about 60% from 2010 to 2022), and further declines are expected with economies of scale and technological advancements. Projects leveraging surplus renewable energy can produce green hydrogen at lower effective costs. - Policy Support:

Countries across the EU, the US, and Asia-Pacific are rolling out substantial subsidies and incentives (e.g. US tax credits of up to US$3/kg, and the EU’s Green Deal targets). In India, the National Hydrogen Mission aims to produce 5 million tonnes of green hydrogen by 2030, creating a supportive policy environment.

Specific Opportunities for the Indian Market

- Domestic Demand & Export Potential:

India’s strong renewable energy base (high solar insolation and wind resources) and aggressive targets for green hydrogen production position the country as both a consumer and potential exporter. Heavy industry and infrastructure projects (e.g., green steel production) will drive domestic demand. - Stock Prospects in India:

Indian-listed companies that are likely to benefit include:- Renewable Energy Developers: Tata Power, Adani Green Energy

- Engineering/EPC Firms: Larsen & Toubro (L&T)

- Industrial Conglomerates: Tata Steel, Reliance Industries (which is exploring hydrogen as part of its broader energy portfolio)

- Technology Providers: Companies involved in fuel cell technology and energy storage solutions

4. Risk Analysis

Key Risks and Challenges

- High Production and Infrastructure Costs:

Even with cost reductions, green hydrogen remains more expensive than grey hydrogen. Large capital investments in electrolysers, renewable power plants, and storage/distribution networks are required. As of 2025, green hydrogen accounts for <1% of global hydrogen production due to costs (~$4–6/kg) remaining 3× higher than grey hydrogen ($1.50–2/kg). However, technological innovations and economies of scale are projected to achieve cost parity by 2030 - Demand Uncertainty:

A significant barrier is the lack of long‑term offtake agreements, particularly in sectors like transport and power generation, where the market is still in early stages. - Shortage of Skilled Manpower:

India is grappling with a significant shortage of skilled manpower in the green hydrogen sector, which poses a critical risk to its ambitious production goals. The country aims to produce 5 million tonnes of green hydrogen annually by 2030, necessitating around 600,000 trained professionals across various stages of the value chain. Currently, the workforce is insufficient to meet this demand, with a particular need for expertise in electrolyzer manufacturing and hydrogen production. The government has initiated programs to address this gap, allocating approximately $2.4 billion to incentivize training and development. However, the success of these initiatives is crucial; failure to develop a skilled workforce could lead to operational delays, increased costs, and diminished investor confidence, ultimately impacting stock prices for companies involved in this sector. Investors should closely monitor workforce development efforts and their alignment with green hydrogen production targets to gauge potential risks and opportunities in the market.

- Technological Risk:

Multiple electrolysis technologies (alkaline, PEM, SOEC) compete in the market. Uncertainty exists regarding which technology will dominate and achieve cost-effectiveness. - Policy and Regulatory Risks:

Changes in government policy, subsidy adjustments, or regulatory uncertainties (both in India and globally) can impact project economics and investor confidence. - Competitive and Supply Chain Risks:

The debate over sourcing key components—such as whether to rely on cost-effective Chinese electrolysers versus building localized supply chains—adds complexity to margin and quality considerations. - Market Maturity:

The hydrogen sector is still maturing, and near‑term returns may be volatile. Investors must be patient for long‑term scale and cost reductions to materialize.

5. Long‑Term Investment Perspective in the Indian Market

Why Invest in Green Hydrogen via Indian Stocks?

- Strategic Renewable Advantage:

India’s abundant renewable energy resources reduce the cost of green hydrogen production over time. - Government Support:

The National Hydrogen Mission, along with state and central incentives, is designed to boost production capacity and drive technology adoption. - Industrial Decarbonization:

As heavy industries in India face increasing pressure to decarbonize, investments in cleaner technologies such as green hydrogen will become more attractive. - Ecosystem Development:

Indian companies are increasingly integrated across the renewable energy value chain, from power generation to heavy industrial processing, making them key players in the transition.

Recommended Investment Approach

- Diversification Across Sectors:

Investors should consider a diversified portfolio that includes renewable energy developers, EPC firms, industrial conglomerates, and technology providers. - Long-Term Horizon:

Given the early-stage nature and capital intensity of green hydrogen projects, a long‑term (10–15 years) investment horizon is recommended. - Focus on Integrated Business Models:

Companies with vertically integrated models—covering renewable generation, hydrogen production, and industrial off-take—are better positioned to capture value. - Monitoring Policy and Technological Advances:

Staying updated on government initiatives, subsidy adjustments, and technological breakthroughs is essential to rebalancing exposure as the market matures. - Risk Management:

Due to high upfront costs and market volatility, consider using a mix of direct equity exposure and thematic ETFs or funds that focus on the energy transition.

6. Conclusion: A 360‑Degree Long-Term View

While the sector is currently challenged by high production costs, technological uncertainties, and demand risks, strong policy support and the imperative for industrial decarbonization provide a robust long‑term growth narrative. Indian companies—ranging from renewable energy developers like Tata Power and Adani Green Energy, to engineering giants such as Larsen & Toubro and industrial leaders like Tata Steel—offer compelling indirect exposure to green hydrogen’s growth.