From the Press Release (bseindia.com)

The Ranipet Plant will have capacity to produce 120,000 units by end of this fiscal year and gradually ramp up to 1 million units in near future

From the Press Release (bseindia.com)

The Ranipet Plant will have capacity to produce 120,000 units by end of this fiscal year and gradually ramp up to 1 million units in near future

Another player jumping in

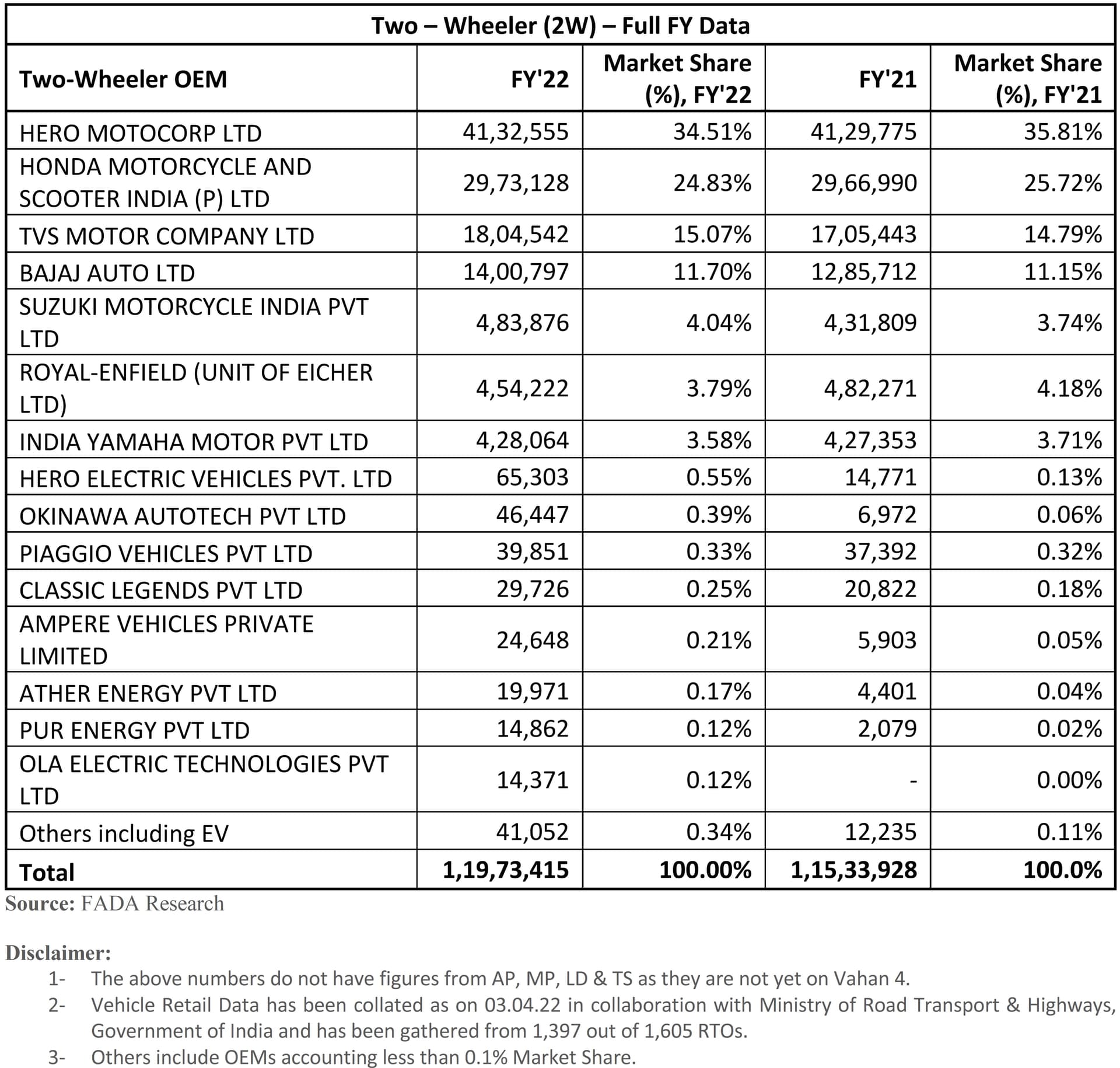

been tracking the Vaahan data and Ampere seems to be clocking 6k+ sales in both March and April, only behind Ola and Okinawa and almost matching Hero Electric.

can you please share the link? this should be very helpful.

You can check manufacturer wise registration data on Vahan portal:

VAHAN SEWA| DASHBOARD (parivahan.gov.in)

Jan 4220

Feb 4304

March 6341

Apr 6539

For the year 2022: 21422 (4 months and 1 day)

For the year 2021: 12470 full year

Not sure how they came up with the 18k figures. My hunch is Vaahan doesn’t capture all of it or Greaves is reporting sale to dealers (channel stuffing). Either which ways, Q4 volumes are likely to be higher than Q3 (assuming that dealers would maintain similar or not a very different inventory level).

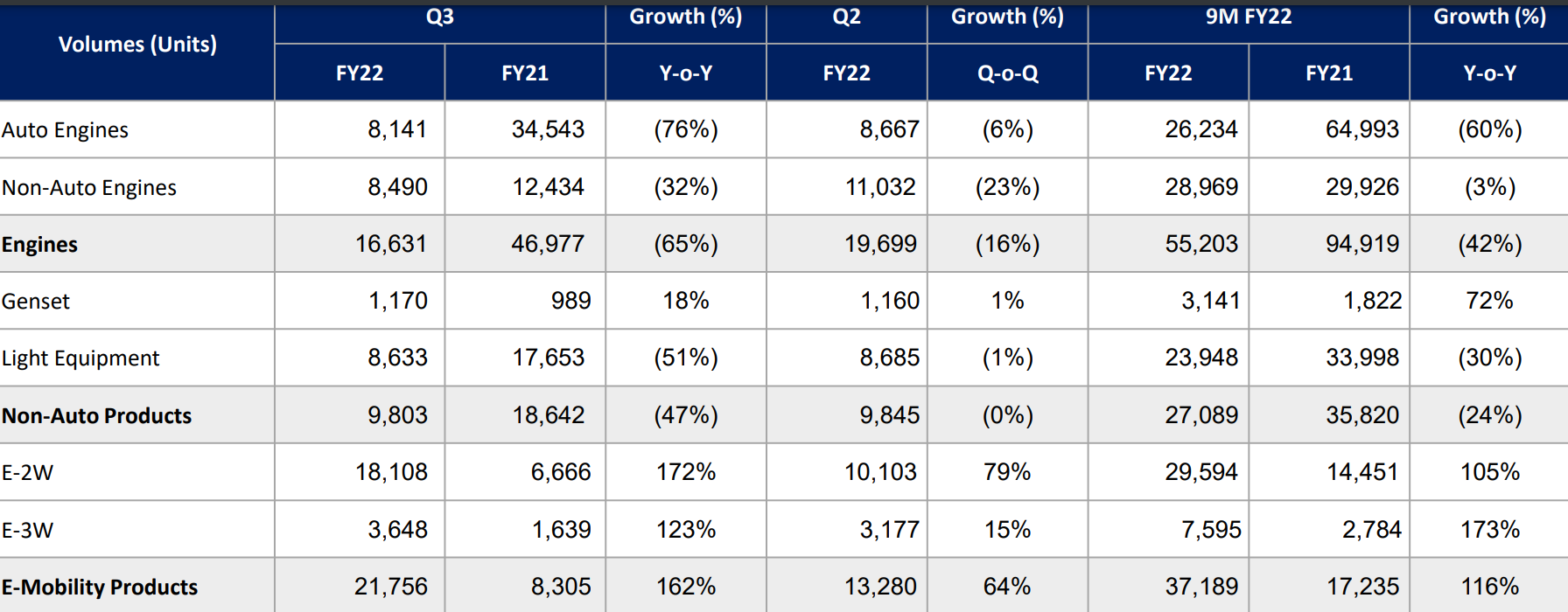

In Q3, GEMPL recorded 180crs of revenue and had -ve EBITDA (possibly -3crs since standalone is +17crs and consolidate Greaves is 14crs EBITDA).

My hunch is in Q4, GEMPL should record around 20%+ QoQ revenue growth so around 210crs. EBITDA to be in single-digit % so maybe around 6/7crs EBITDA.

Q1FY23 however seems to be turning out fire for Ampere if April 2022 is anything to go by. My hunch is the co may exceed 100k volumes in FY23. It is already on track for 72k and we know there is going to be MoM growth in EV volumes.

D - Invested at around 200. Researching and trying to understand Greaves’s supply chain, competencies, etc.

It maybe because Vahan maintains registration data, but low speed e2W does not require registration(ampere manufactures quite a lot of them) and it does not reflect in vahan data.

Dealer numbers won’t give the full picture when it comes to EVs since both Ola and Ather are D2C.

In any case, best to wait for results, expecting the co to report double-digit EBITDA.

Did better than my expectations. GEMPL revenues grew by around 30% QoQ in Q4 to reach an all time high of around 237crs. Annual run rate now is close to 1000crs.

Only thing to watch out for is how the launch of Hero’s 2W EV will affect the incumbents. If low impact, the incumbents could continue gaining the market share on a market that is increasing its size rapidly.

Entirely possible that EV biz reports revenues of over 1500crs for FY23 with PAT of >100crs (assuming modest margins).

EDIT - Also Ampere is now comfortably beating Ather in monthly volumes. Though both the 2Ws cater to different customer segments, the gap between them is only growing. Ampere is now a distant third behind Okinawa (1st) and Ola (2nd).

Interesting to see if Ampere can bump its volumes from here. Has everything going for it currently - better distribution, a good product, not much controversy.

How do investors in the stock perceive its valuation right now?

Do you compare this with Ather that’s nearly 1 billion $ in valuation as per latest round, and Ampere with similar revenue rate even at 80% discount shd alone hv valuation of 5k? Add to this 400 crs. of cash and equiv.

You are getting these at 40% discount and other businesses free.

Is this the correct approach or wat is it that I am missing here?

Disclosure :- No investment. I’m currently in Anti-EV camp. Was looking for few deep value bets in this carnage and came upon this purely from valuation point of view.

Possible reasons for undervaluation:-

It is in the above context that fund raising plans become important. If greaves can raise fund from a marquee investor, the market will show some confidence to it.

Ofcourse the whole thing / perception will change if Ampere is severely able to beat competition and get close to Ola / Okinawa in terms of numbers.

Currently, Ampere is a distant third.

Seems like Ampere is selling more units than Ola in June. Also on track to post the highest ever monthly and quarterly volume I think. In March Greaves did around 6500. It’s already at 5800 in June with 3 days to go.

Annual run rate must be now comfortably over 1000crs with such volumes. My guess is roughly around 1300 to 1400crs.

As of June this morning:

AMPERE VEHICLES PRIVATE LIMITED 5,564

ATHER ENERGY PVT LTD 3,155

OKINAWA AUTOTECH PVT LTD 6,245

OLA ELECTRIC TECHNOLOGIES 5,361

For 2022

AMPERE VEHICLES PRIVATE LIMITED 32,808

ATHER ENERGY PVT LTD 15,292

OKINAWA AUTOTECH PVT LTD 46,382

OLA ELECTRIC TECHNOLOGIES 41,470

July/ Aug/ Sept

AMPERE VEHICLES PRIVATE LIMITED 6,320/ 6,399 /6,188

ATHER ENERGY PVT LTD 1,289/ 5,297/ 6176

OKINAWA AUTOTECH PVT LTD 8,099/ 8,558/ 8,280

OLA ELECTRIC TECHNOLOGIES 3,863/ 3,440/ 9,649

For CY’2022 as of 10th Oct

AMPERE VEHICLES PRIVATE LIMITED 53,822

ATHER ENERGY PVT LTD 29,870

OKINAWA AUTOTECH PVT LTD 73,486

OLA ELECTRIC TECHNOLOGIES 60,186

“We believe that successful transition towards electric mobility in India goes much beyond just the sale of EVs, but also extends to a myriad of customer centric solutions and services, including an easy & affordable access to quality after-sales service during the lifecycle of the vehicle.

Interesting update at Auto Expo - https://www.bseindia.com/xml-data/corpfiling/AttachLive/5fb15dba-0cee-43c4-b9e8-fa7d9370ea9c.pdf

and video release for branding Har Gully Electric Anthem - Take Charge with Ampere - YouTube