Initiating this topic to keep a list of great book summaries that we come across. Refreshers on great books. Please cite source (in case not own work). Let’s share content and give credit where credit is due.

3 Likes

Zero to One by Peter Thiel

A tweetstorm by Douglas (@Douglas9162) - Incredible work.

Source: https://twitter.com/Douglas9162/status/967814217545015297

- Every moment in business only happens once. The next Zuckerberg won’t make Facebook, nor the next Gates make Microsoft. If you are copying these guys, you aren’t learning from them.

- Every time we create something NEW, we go from 0 to 1.

- Technology is miraculous because it allows us to do more with less

- Whenever Thiel interviews someone for a job, he likes to ask: “what important truth do very few people agree with you on?”

- If you take one typewriter and build 100, you have made horizontal progress (1 to n). If you have a typewriter and build a word processor, you have made vertical progress (0 to 1).

- At the macro level the single word for horizontal progress is globalization – taking things that work somewhere and making them work everywhere.

- The single word for vertical progress (0 to 1) is TECHNOLOGY.

- Its hard to develop things in big organisations.

- Start ups operate on the principle that you need to work with other people to get stuff done, but you also need to stay small enough so you actually can

- Advertising was too ineffective to justify cost to grow Paypal initially so they just paid people $10 to get them to sign – led to exponential growth

- Four principles for business: a) it is better to risk boldness than triviality, b) a bad plan is better than no plan, c) competitive markets destroy profits, d) sales matter just as much as product

- The most contrarian thing of all is not to oppose the crowd but to think for yourself

- Under perfect competition, in the long run no company makes an economic profit. Despite economics saying its best, it is actually the worst market to be in

- Google is a good example of a company that went 0 to 1. It hasn’t competed in search since early 2000s

- Monopolists lie to protect themselves. They know bragging about their great monopoly invites being audited, scrutinised and attacked. Therefore they pretend to be part of a bigger pie than they actually are.

- Example of above point: google. In may 2014 they had 68% of the search market(monopoly) yet google markets themselves as being in the worldwide advertising market where they only own 3.4% of market.

- Remember what market you actually are in. If you justify your British restaurant in SF with logic “no-one else is doing it so we will dominate” you will likely fail. You are not competing with other british restaurants in SF, you are competing with all restaurants in SF.

- Being the best restaurant > being the best british restaurant in SF. Best X > Best X given A and B. X is the actual market you want.

- Non monopolists exaggerate their distinction by defining their market as the INTERSECTION of various smaller markets.

- Monopolists, by contrast, disguise their monopoly by framing their market as the UNION of several large markets.

- In business, money is either an important thing or it is everything. Monopolists can afford to think about things other than money; non-monopolists can’t.

- Only one thing can allow a business to transcend the daily brute struggle for survival: monopoly profits.

- Creative monopolists give customers more choice by adding entirely new categories of abundance.

- “If the tendency of monopoly businesses were to hold back progress, they would be dangerous and we would be right to oppose them. But the history of progress is a history of better monopoly businesses replacing incumbents”

- Monopoly is the condition of every successful business.

- All happy companies are different: each one earns a monopoly by solving a unique problem. All failed companies are the same: they failed to escape competition.

- Competition means no profits for anybody, no meaningful differentiation and a struggle for survival

- Our educational system both drives and reflects our obsession with competition

- Higher education is the place where people who had big plans in high school get stuck in fierce rivalries with equally smart peers over conventional careers like consulting and Investment banking

- "All Rhodes scholars had a great future in their past”

- War is costly business. Rivalry causes us to overemphasize old opportunities and slavishly copy what had worked in the past.

- The hazards of imitative competiton may be why people why aspergers like social ineptitude are at an advantage. They are much less likely to do what everyone else is doing

- “amid all the tactical questions – who could price chewy dog toys most aggressively – who could create super bowl ads? – the companies totally lost sight of the wider question of whether the online pet supply market was the right space to be in” Choose your battles wisely

- if you cant beat a rival, it may be better to merge

- “sometimes you do have to fight. where that’s true, you should fight and win. There is no middle ground: either don’t throw any punches, or strike hard and end it quickly.”

- Any firm with close substitutes will see its profits competed away. E.g. restaurants and nightclubs once people move to trendier/better alternatives

- For companies to be successful they must grow and ENDURE. Many entrepreneurs focus only on short term growth. Because growth is easy to measure, durability isn’t

- If you focus on near term growth above all else, you will miss the most important question: will this business still be around in a decade?

- As a good rule, proprietary technology must be at least 10 times better than its closest competitor in some important dimension to lead to a real monopolistic advantage

- The clearest way to make a 10x improvement is to invent something new

- You can also make a 10x improvement through superior integrated design. E.g. Ipad vs all preceding tablets

- Network effects are when a product becomes more useful when more people use it.

- Network effects can be powerful, but you’ll never reap them unless the product is useful to its very first users when the network is necessarily small.

- Example of starting small: facebook started with just Harvard people – not everyone on earth

- A good startup should have the potential for great scale built into its first design. E.g. twitter doesn’t need many more features to attract more users

- Many businesses gain only limited advantages as they grow to scale. Service busineses are especially difficult to make monopolies. Service busineses will never reach a point where a core group of people can provide something of value to millions –unlike software for example.

- Techniques for polishing the surface don’t work without a strong underlying substance

- When Steve Jobs returned to Apple, he didn’t just make apple a cool place to work; he slashed product lines to focus on the handful of opportunities for 10x improvements

- every startup is small at the start. Every monopoly dominates a large share of its market. Therefore, every startup should start with a very small market. Becoz its easier to dominate a small market vs a large one

- 100% of a $50m market >>> 1% of $5bn market

- As you craft a plan to expand to adjacent markets, don’t disrupt: avoid competition as much as possible

- Its much better to be the LAST mover – that is, to make the last great development in a specific market and enjoy years or even decades of monopoly profits

- In the 1950s people were much more optimistic to business, now people a lot more negative

- Private equity and management consultants don’t start new businesses; they squeeze extra efficiencies from old ones with incessant procedural optimisations.

- Finance epitomises indefinite thinking because it’s the only way to make money when you have no idea how to create wealth

- a) - When a big company makes an offer, it almost always offers too much or too little: founders only sell when they have no more concrete vision for company; in which case the acquirer probably overpaid

b) - founders with robust plans don’t sell, which means the offer wasn’t enough. E.g. Zuck refused $1bn offer for FB in 2006 within 10 mins, as he knew it would be worth more - The biggest secret in venture capital is that the best investment in a successful fund equals or outperforms the entire rest of the fund combined.

- This leads to two rules for VCs: 1- only invest in companies with potential to return entire value of fund. Rule 1 eliminates most companies. Rule 2 is that rule 1 is the only rule as it is so restrictive.

- bcoz of (58) – this is why investors typically put a lot more money into any company worth funding

- The 12 biggest tech companies were venture backed. Combined they worth more than all other tech companies

- If anything, too many people are starting their own company these days. It is better to be facebook employee #10 than to be CEO of your own company for the sake of being CEO. Differences between companies dwarf the differences in roles inside companies

- “If everything worth doing has already been done, you may as well feign an allergy to achievement and become a barista”

- the actual truth is that there are many more secrets left to find, but they will only yield to relentless searchers

- when thinking what company to build, ask two questions: what secrets is nature not telling you? What secrets are people not telling you?

- A great company is a conspiracy to change the world; when you share the secret, the recipient becomes a fellow conspirator.

- It’s very hard to go from 0 to 1 without a team

- To anticipate likely sources of misalignment ask 3 things: Ownership- who legally owns company? Possession- who runs company day-to-day? Control: who formally governs the company’s affairs?

- A board of three is ideal, never exceed board of 5 unless it is publicly held.

- Hiring consultants doesn’t work, part time employees don’t work, even remote work should be avoided. Bcoz misalignment creeps in when people aren’t together full time

- A company does better the less it pays the CEO – one of clearest patterns Thiel notices #SkinInTheGame

- A cash poor, equity rich executive will focus on increasing the value of the company as a whole

- If a CEO doesn’t take lowest salary then they should take highest one, as long as figure is modest as this effectively caps pay

- People who prefer equity over cash show long term commitment

- Don’t work with people you can’t envision a long term future with

- When ppl ask why they should work for you vs prestige choice; focus on 2 things. Your mission and your team

- Above all do not fight perk war in reasons for people to work for you. Unique work >>> unique perks

- Everyone in your company should be different in the same way: a tribe of like minded people fiercely devoted to the company’s mission

- Best thing Thiel ever did at Paypal is make each person responsible for just one thing – defining roles reduced conflict

- Is a lukewarm attitude to one’s work a sign of mental health?

- Advertising matters because it works

- What nerds miss is that it takes hard work to make sales look easy

- Like acting, sales works best when hidden. None of us want to be reminded when we’re being sold

- If you’ve invented something new but you haven’t invented an effective way to sell it, you have a bad business – no matter how good the product

- In general, the higher the price of your product, the more you have to spend to make a sale - and the more it makes sense to spend it.

- Complex sales (>$1m sales) work best when you don’t have salesman at all. For Palantir (Thiel’s company) the CEO spends 25 days per month on road selling product. At complex price point people want CEO not VP of sales

- In between personal sales (salespeople needed) and traditional advertising (no salespeople) there is a deadzone ($100 -$10k ish), where few sales methods are economical

- Advertising can work for start ups but only when your customer acquisition costs and customer lifetime value make every other distribution channel uneconomical

- when you can only spend dozens of dollars acquiring a new customer you need the biggest microphone you can find.

- Whoever is first to dominate the most important segment of a market with viral potential will be the last mover in the whole market

- Most businesses get zero distribution channels to work: poor sales rather than bad product is the most common cause of failure. If you can get just one distribution channel to work, you will have a great business.

- Never assume that people will admire your company without a public relations strategy.

- Any prospective employee worth hiring will conduct his own diligence; so what he finds on google will be critical to the success of your business.

- Luddites are so concerned with being replaced that we would rather we stop building new technology altogether

- a) Seven questions EVERY business must answer: 1; Can you create breakthrough technology instead of incremental improvements? 2; Is this the right time to start your particular business? 3; are you starting with a big share of a small market? 4; do you have the right team?

b) 5; do you have a way to not just create buy deliver your product? 6; will your market be defensible 10 and 20 years into the future? 7; have you identified a unique opportunity that others don’t see? - If you nail all 7 questions above, you will master fortune and succeed. Even with 5 or 6 it might work

- Only when your product is 10x better can you offer the customer transparent superiority

- “There’ s nothing wrong with a CEO who can sell, but if he actually looks like a salesman, he’s probably bad at sales and worse at tech”

- The best problems to work on are the ones nobody else even tries to solve

- Having a head start and moving faster than anyone else is a formula for success

- We need founders in business, we should be more tolerant of founders who seem strange or extreme; we need unusual individuals to lead companies beyond mere incrementalism. The end xx.

21 Likes

100 to 1 In the Stock Market by Thomas Phelps

Book summary by Nitin (@BigNitin) - Fantastic work

Source: https://biginvestorblog.com/2014/12/11/100-to-1-by-thomas-phelps-in-95-points/

15 Likes

Tremendous stuff…overwhelmed…by the effort put in summarizing…it helps in grasping for like me who is unable to read the whole book

summary of Good to Great attached written some time back Good to Great.docx (418.6 KB)

also link below has summaries of few books

3 Likes

Zuhayeer Musa (Twitter: @zuhayeer) has made a website to find tweetstorm summaries of some great books.

2 Likes

4 Likes

"Of Long Term Value and Wealth Creation from Equity Investing (Observations, Ideas & Reflections)" by Bharat Shah.

Book summary (tweetstorm) by Abhishek Murarka (@abhymurarka) - Superb work.

Source: https://twitter.com/abhymurarka/status/1061206129705811971

- Essential principles of investing have largely remained unchanged over history of organized investing. What has changed is the interpretation and application by investors, as deemed convenient or expedient at a particular point in time.

- Investing is simple, but not easy. Simple, because it’s not difficult to understand the essential principles of investing- a large opportunity, accretive earnings growth, high character & a certain degree of predictability. Not easy, because the required discipline is rare.

- Even some of the best investors falter at “Doing it right” rather than “Knowing it right”. More failures have occurred, even among the greatest thinkers and investors, on account of former rather than the latter.

- Good investing is a heady mix of art & science. The art is about understanding the quality & character of business & of the people behind it. Transcribing the art into a tangible working model is the science of it. The art part feeds into the science, not the other way round.

- Returns are tangible, but the risk is not. Hence, returns appear as real to the investors, but risk appears as amorphous. Returns become real only if backed by intelligent risk taking. Quality of returns is different from quantum of returns.

- It is impossible to operate only on the good part of market cycles. Those incredible ‘timing’ skills hit you back if you try them long enough. Investing is indeed long term even though it is not considered fashionable these days. Anyone saying otherwise is likely fooling you.

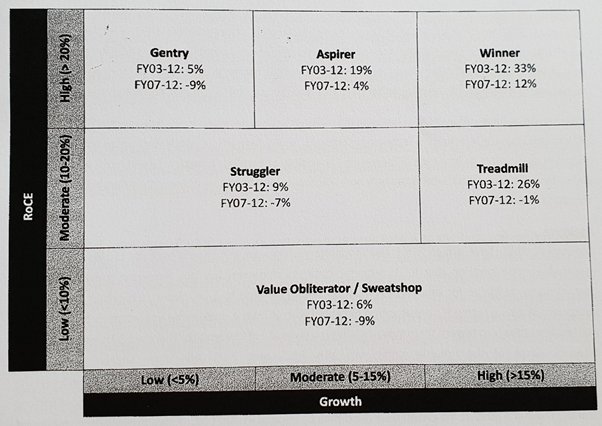

- Size of Opportunity is the foundation for growth investing. Ask will it hit a glass ceiling or soar freely for long. Uses framework of size of fish (company) & the size of pond (industry). Size of the pond determines the size of the fish AND your meal. Four possible outcomes (illustrated in picture here):

- A business may have high profitability, superior capital efficiency, reasonable growth, yet fail to create efficient compounding, if it is about to hit a glass ceiling. A large opportunity may fail to get high valuation if profitability is compressed. Eg: Organized retail.

- The debate around large caps or mid/small caps is largely an artificial one. Debate is really between quality vs lack of it, the nature of growth (Accretive/Dilutive) & about future size rather than present one. Large/mid/small is relative to opportunity they are catering to.

- After size, focus on feasibility of value creation. While size helps, what matters more is character. It is the ability of a business to create Economic Value (EV) by generating superior Return on capital over its cost of running the business over an extended period of time.

- Earnings Growth Quality: Uses the concept of Compounding Multiplier (CM), where CM = CAGR of investment returns/ CAGR of profits over a period. Denotes returns generated per unit of profits. The book presents CM analysis for over 100 companies over FY 2003-12 and FY 2007-12. Compounding Multiplier (CM) table here.

- When growth goes away, Stocks become Bonds and cannot really quote higher than the Net Worth. If the outlook deteriorates further, they will be treated worse than a Bond and might trade at a discount to their Net Worth/ Book Value. (Case in point: NBFC scenario now.)

- When the character of the market is a Growth market, focus has to be on growth investing and not Cigar Butts. Feels India is a growth market will ample high amplitude growth opportunities with desired longevity.

- Not all growth is good. Focus on businesses with accretive growth over dilutive growth. Markets view capital dilution with a healthy skepticism. Avoid if dilution is recurrent, devoid of economic logic, outsized or in unrelated areas or for perceived dubious reasons.

- Businesses entailing significant Capex & those with significant capital dilution are Siamese twins and have same operating conditions. High capex will have high capital dilution & vice versa. These are anti-thesis to good returns & will lead to mediocre compounding at best.

- Market distinguishes colour of money. It does not reward acquisitive growth in the same way as Organic growth. In other words, per unit market returns for a unit growth of profits is less for acquisitive growth compared to organic growth.

- On Capital Allocation: A mgmt unsure about the payoff but allocating capital is flirting with uncertainty. A mgmt unsure of the size of opportunity will allocate capital randomly which could destroy value. No mgmt has the capability of managing >1 or at most 3 businesses.

- Banking & Finance: A special compounding machine

a. Proxy of the economic growth - Inherent compounding

b. Are lead indicators rather than lagged

c. Money is RM, raising RM at lower cost creates value

d. Dilution & leverage are part of the game & not a crime. ROA is the game - Business Quality – Growth Matrix: Forms the crux of Growth and Value Investing. Price provides sails or wings to the ship while earnings growth provides the wind.

- Scenarios:

• High ROCE, High growth – Strength to weather storms and progress

• High ROCE, Low growth – Preservation, but no progress

• Low ROCE, High growth – Illusion of progress

• Low ROCE, Low growth – The ships will sink - Growth-Quality and Compounding Multiplication (point #11 above) are linked as seen in chart here.

- Quality, in simple terms, is the ability to generate superior, consistent, predictable & durable ROCE. Two vital tests of Quality:

a. Capital Intensity: Whether a business fundamentally requires high capital

b. Capital Efficiency: Whether the capital generates superior returns - A business with both high Fixed Capital & Circulating/Working Capital has unfavorable capital intensity profile. High Fixed capital intensity maybe compensated by low Working capital intensity and vice versa. A business may also be capital light but have mediocre capital efficiency.

- Predictability improves value since it has an implied effect of lowering the discount rate (in DCF). Future cash flows discounted at a lower or higher rate depending on it. Consistency drives pricing premium and triggers re-ratings.

- Businesses with lumpy capital requirements have a basic flaw from investing perspective & will have lumpy returns. Example: Airlines, Hotels. Metals (Steel), Oil exploration, etc

- The superiority of a business is inferred from superiority of the ROCE and the superiority of a management from the superiority of the ROE.

- Growth of the earnings has a way of covering valuation mistakes, and thus help in avoiding permanent loss of capital. Even if one has overpaid, it helps in obviating this error of commission.

- Margin of Safety: If you are going to invest like Ben Graham, then your sources of margin of safety are different than if you invest like Warren Buffett. You just have to be aware of those sources and also of their limitations.

- On timing: A high quality business, even if purchased at the highest price of initial year in a 5-year cycle & sold at the lowest in last year, generates substantially higher returns than opposite purchase timing for a low quality business.

- In bad businesses, the returns, if at all, can only be point to point; which means it is a very chancy transaction akin to flipping a coin many times over and getting it right every time.

- On Dividends: When business is mediocre, but payout is strong, market views it as unaffordable luxury. In such cases as far as Investment Returns go, mediocrity wins!

- Market has long memory like much like that of an elephants. Retail investors, at times get caught in a bubble, and rely on short term memory. This is a recipe for pain. PS: A bad management doesn’t change colour.

- When intent is not trusted, the value put on numbers will diminish, since market prepares for a possible future shock and thus systematically undervalues such a business and management, for a long period till, if at all, the credibility is restored.

- On valuations: Investing is about pricing the value, rather than valuing the price. Price to earnings is a rubbish way of computing value. But unfortunately it is most prevalent. P/E is in fact a derivative of value, but people infer value from P/E.

- The basic trick is NOT to look at valuations as first filter, but at quality. Pure cheapness is never a virtue. The trade-off is never in terms of valuation vs quality; its quality followed by valuation. Buy businesses with superior & sustainable ROCE rather than just low PE.

- On behaviour: It’s the innate desire of (even a good) investor to leave footprints on sands of time that makes him/her choose the less obvious over the obvious & to see virtues in inferiority over quality. Desire to shun boring businesses induces bias for the poisonous ones.

- Investing is not a get-rich quick scheme, though such outcomes also occur at times. When it happens, they are merely milestones in long term process of Wealth creation. Hoping for the same to sustain leads to a larger wealth erosion with the reverse flow hitting you harder.

- Ultimately, investing is nothing if not business like. It is a myth to believe that one can earn investment returns even if the underlying business has inferior economic value creation.

- Investors like to talk about absolute returns when markets are falling & relatively superior returns when markets are on ascendance. Absolute and relative returns are like two rabbits – you try to catch both, you get neither in your hands. Focus on first, you get the latter.

- Lao Tzu says “I have just three things to teach you: simplicity, patience, compassion. These three are your greatest treasures.” In good investing, read it as simplicity (of business), patience (of investor) and passion (for quality).

- “Based on my personal experience over last 3 decades, rarely do more than three or four variables really count. Everything else is noise.”

{kind=link}

{kind=link}

{kind=link}

Summary by @abhymurarka illustrated through 4Ps here.

{kind=link}

20 Likes

This book is not available in Flipkart or amazon. Can you please share the details from where it can be procured?

Summary of Global Asset Allocation book by Meb Faber:

- Diversifying your portfolio by including uncorrelated assets is truly the only free lunch.

- 60/40 has been a decent benchmark, but due to current valuations, it is unlikely to deliver strong returns going forward.

- At a minimum, an investor should consider moving to a global 60/40 portfolio to reflect the global market capitalization, especially right now due to lower valuations in foreign markets.

- Consider including real assets such as commodities, real estate, and TIPS in your portfolio.

- Once you have determined your asset allocation mix or policy portfolio, stick with it.

- The exact percentage allocations don’t matter that much.

- Make sure to implement the portfolio with a focus on fees and taxes.

- Rebalance once a year

- Go live your life and don’t worry about your portfolio!

More details with different portfolio returns comparison: https://cold-brew.blog/2019/01/09/book-summary-global-asset-allocation/

Folk Wisdom enlivens the book’s pages.

“Democracy on the Road” by Ruchir Sharma, of Morgan Stanley Global Strategy, is a ground-breaking book in many senses of the term. It focuses on the Dance of Democracy in India, and has over 2 decades of Ruchir Sharma’s observations of the polls in India ,behind it. It is,in that sense, not an over night phenomenon of a cut & paste compilation .

Ruchir Sharma belongs to a small town, Bijnor, in UP, from where he spread his wings globally. Hence, he is rooted in the heartland of India, and is able to look at the Indian poll-scene, through a global lens, without letting the heat and dust of a small town, fog the lens.

What is noteworthy about Democracy on the Road, are the many incisive insights which pepper the book. The author has his ear to the ground,and identifies many local and regional trends that influence state polls. Caste and local rivalries need to be taken into account,as he says,that India may have changed,but not fast enough or deep enough. Alliances seldom last, and usually are region-specific. The author discerns an anti-incumbency factor, that over-rides party politics,and is a long-lasting trend in Indian politics. He has a knack for recording pithy folk wisdom, that rings true.For instance, never get too close to a politician,because, like coming close to the sun, you may get singed.

All in all, the book makes interesting reading. Also available on Kindle.

I run a book review blog,and I published this review there.

1 Like

Wrote a thread with my key take-aways from What I learnt about Investing from Darwin by Nalanda Capital’s founder, Mr. Pulak Prasad.

3 Likes