great lessons from jatin khemani sir, valuable insights, Grateful to you sir, keep providing such valuable insights sir, and thanks to the person who uploaded, keep uploading such valuable content. it really helps.

I was feeling aggrieved about my lack of concentration these days. I read the Stern article practically in one sitting, spilling water while having breakfast.

I too dream of investing in a down and out company with great prospects. Then I look at Mehtas of this world and their deep-diving, and I bow to them.

Great word of wisdoms:

The next multibagger rarely comes with flashing neon signs or front-page headlines. It’s usually hiding in plain sight—quiet, overlooked, even ridiculed. The crowd doesn’t see it, the analysts don’t model it, and most investors dismiss it outright. That’s precisely why it has room to surprise.

Great winners are almost always born misunderstood. In the early days, the narrative is confusion, doubt, and disbelief. The market sees “risk,” while the few who dig deeper see “optionality.” And as the business executes step by step—building moats, scaling operations, defying skeptics—the price begins its quiet march.

Then one fine day, the switch flips. The world “discovers” it. Media calls it visionary, institutions pile in, and the same voices that once mocked it now call it a “wonderful business.” But by then, the outsized gains have already been harvested by those who believed before the spotlight arrived.

The essence of superior investing lies in this gap—between perception and reality, between doubt and conviction. The crowd waits for validation; the true investor moves before it.

So remember: the next big winner won’t look obvious. It will look questionable, messy, maybe even boring. And that’s the very disguise that hides greatness until it’s too late.

Disclaimer: Copy and paste from Twitter handle of Arun Mukherjee.

17 Likes

This is indeed more or less perfect articulation of investing journey.

All multi baggers are almost always in the hindsight. No one predicted those at the start of their journey. All analysts generally start painting rosy picture once it has already been 5 or 10 bagger. That’s how analysts operate (unfortunately!!). Why will they tell you that specific stock is going to be a multi-bagger in advance before they themself have made some profit by investing much before you.

I may be wrong but this is my personal experience.

You have to build your own framework, process and conviction. TCS used to trade at P/E < 18 during its early days while Infosys used to have Avg P/E of about 25. How many analysts would have thought that TCS was undervalued at that time. Very Few. Eventually TCS started commanding Avg P/E of 25 to 30.

2 Likes

I found this article by Eagle Point Capital which talks about the different kinds of business and how they navigate an inflationary world.

Building Resilience to Inflation

This write-up references and builds on Warren Buffett’s 1977 article on How inflation swindles the equity investor

It touches upon:

- Why equity investors in inflationary times are forced to invest fresh capital just to keep up with purchasing power and ROIC

- Then it goes on to list different kinds of businesses and how resilient they are, or how much pricing power they have to beat inflation. Examples touched include Commodities, Long Lived assets (real estate, infra, railways, utilities), Take rate or pipeline like business (Actual pipelines, tollbridge, Visa, Amex, Mastercard, AMCs), Insurance etc.

While the piece starts off on inflation resilience, it includes a great write-up on qualities of great businesses with pricing power. This can be useful in helping build a mental model on the qualities an investor can look for while buying any business.

13 Likes

I have found out an excellent article regarding the distinction between intrinsic value and a market price of a stock.

The Calculus of Value ( The Memo by Howard Marks).

The memo presents a framework for understanding the distinction between intrinsic value and market price, emphasizing that value is derived from the fundamentals of an asset, while price is shaped by investor psychology and market forces. Marks highlights how elevated prices and optimistic psychology can disconnect prices from underlying value, and discusses the risks associated with such environments. He reviews market developments in 2025 (including tariff shocks and relief rallies), and the increasingly prominent role of tech giants in market valuations, usually at higher price/earnings (p/e) ratios. The memo concludes with advice for investors to become more defensive in periods of high valuation and exuberant investor sentiment.

6 Likes

Universal business lessons that applies to building businesses in any Industry.

4 Likes

https://archive.ph/CKCVH

Mistaken Ghost Order Caused Worst India Trading Blunder in Years

The broker informed the sellers about the error soon after the market open, telling them that Avendus had managed to repurchase the shares and that there would be no losses for the family, according to the people.

Won’t there be a huge tax due incoming because of this? The cost of these promoter shares must be in single digits and sold at more than 1k.

6 Likes

Found this substack helpful to understand the economics of capex in hospital sector.

2 Likes

Must read for novice as well as a reminder for investors been in the markets

Brightcom Saga: How numbers can lie.

2 Likes

Summarised the entire story:

What Happened

SEBI dropped hammer on Brightcom Group Ltd (BGL), exposing years of deceptive accounting and misleading disclosures. Once hailed as a digital marketing powerhouse, BGL is now suspended from trading and facing serious penalties.

Key Violations

- Impairment Losses Hidden: ₹868 crore in losses were tucked away in “Other Comprehensive Income” instead of the Profit & Loss statement—masking the company’s true financial health.

- Fake Promoter Shareholding: Promoters quietly sold off shares, dropping from 40% to 3.5%, while falsely reporting 18.47%—misleading investors for nearly a decade.

- R&D Cost Manipulation: ₹504 crore in R&D expenses were wrongly capitalized as assets, inflating profits and balance sheets.

- Intangible Asset Shenanigans: Costs were delayed and misclassified to make the company appear more valuable than it was.

Fallout: Over 6 lakh retail investors are stuck, with no way to trade.

12 Likes

5 Likes

How to look for red flags. This guy has done a good job of explaining the possible shenanigans. Some of the highlights from the video

- buying land from its promoters

- started paying a significant royalty to its promoter

- loans and guarantees given to promoter group companies

7 Likes

As per MINT, Retail investor’s share in cash market is at 10 Year Low i.e. at 34.2% in August 2025 Vs. 45% in 2020-21.

This is a good indication for true long term value investors. Once the over enthusiasm about share markets goes down then generally you can invest at more reasonable valuations.

(I am not posting the link since it is paid and not a free article).

15 Likes

I liked Ray Dalio’s series on Why Nations Succeed and Fail and How Countries Go Broke both of which are free to read on linkedin.

In his latest post, he draws parallels between the world as it is today and as it was in the 1930s.

One tends to ignore the isolated events, unless they are listed out together like Ray does in his article, and then you realize how things are progressing. While i don’t agree with him lumping India with the bloc of rival nations, but still the article is a decent read to understand the developing geo-political situation.

4 Likes

Ray Dalio and some other notable authors from economics to geo politics have in recent times drawn attention to current situation we are in. Based on my learning from the books by Ray, Turchin, others I had made a presentation on and uploaded it VP. Sharing if it interest you.

3 Likes

Pretty detailed presentation Sougata, you really put a lot of work into it! Its a nice comprehensive summary of the 4 books you mentioned.

2 Likes

Michael-Burry-Case-Studies (1).pdf (601.3 KB)

Michael Burry was born at a very young age. He studied medicine in college and in his free time read Benjamin Graham and David Dodd. During his initial days he used to run his own blog where he recommended stocks. His writeups were so good that a little investor that no one had heard of (some Greenblatt or something) was really impressed. Mr. Greenblatt waited for Burry to leave medicine and start his own fund where Joel bought a million dollar stake in the fund.

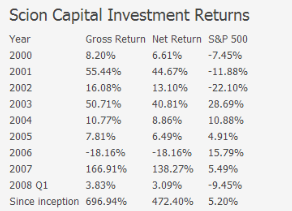

Here is the performance summary of Scion Capital, the fund run by Dr. Burry. These returns cure cancer. The only negative year he had was 2006 and that was because of premiums paid on Credit Default Swaps. He beat the market in 2006 as well ex-CDS. Funny thing is people remember him for that one trade he made where he betted against the entire housing market in what is possibly the greatest recession the world has ever seen since 1929. But there is much more to Burry’s genius than what appears.

I have attached Burry’s MSN money articles from his college days. It will be the best 46 pages you will read this month. Probably the next 6 months or probably ever.

He covers everything - how to evaluate management, how to identify business cycles, how to evaluate a business, how to distinguish a bad news that is not so bad after all, how to distinguish a good news that is not so good after all, how to make money from small caps, mid caps, large caps, micro caps (you name it).

He correctly predicted the IT bubble burst, obviously predicted the 2008 crash 3 years before it happened. Closed down his fund and started Scion Asset Management to manage his own funds, outperformed not only the S&P 500 but also the average hedge fund in the USA!

He was one of the first person to identify that Gamestop (NYSE: GME) was undervalued and bought a 4% stake in 2019 or early 2020s. We all know what happened after.

He shorted Tesla early citing valuation and business fundamentals reasons. He indeed lost a lot of money, covered his short. Humorously, 1.5 years later, Tesla reported huge de growth in its business and stock tanked 50%.

In early 2000s, CISCO announced a $ 1 billion write-off. Sell side analysts at the time said, its a one time write off and the business prospects are great hereon. Burry in his blog stated with reasons why he thinks that this not a temporary problem. He criticized the management and had a very insightful analysis on stock options.

Cisco took 25 years to get back to the price when Burry published that blog.

Also, Burry identified Apple as a Buffett stock (consumer facing with high brand recall), 16 years before Buffett identified it as a Buffett stock! He sold it for a quick 60% gain though. He backed the then Steve Jobs run Pixar (when Jobs was fired from Apple) and made a lot of money where people weren’t even daring to look. (The consensus at the time was that Toy Story was the only profit driver of Pixar)

Calling Burry a genius would be like calling outer space big.

20 Likes

Reading books on investments is overrated. After the first few ones, namely Lynch, Graham and Fischer, there is not really any value addition that other books do. They say the same thing in different words. They are theoretical in nature and provide no practical insight.

For example, Mr. Marks in both of his books screamed that cycles play an important role. That an investor should always have an idea of the market or industry cycle to put the “odds” in his favor and that cycles are inevitable. While I agree, I would have been better of reading how to actually identify at which point of the cycle we are standing . How to figure out the estimated inflexion point in the real life. He doesn’t talk about it anywhere.

Then I figured that to actually understand a business, industry, or cycles thereon the best material one can read is research reports published by Short Sellers. Fundamental based short sellers target companies in euphoria, analyze their business model, competitive intensity and short sell companies that are vulnerable to future business and industry developments. They also look past management and consensus forecast and do their own pragmatic future financial projections. They will tell you how they think and how you should think.

Some short sellers also look for forensics and accounting shenanigans. Frontloading revenues, outright accounting fraud, questionable management judgements, etc.

Rather than reading the same theoretical points again and again I’d rather read Hindenburg Research, Viceroy Research or reports by other forensic research firms.

One such firm is “Off Wall Street” (OWS).

About OWS

OWS is a fundamental short based research firm, that provides recommendations to only a select institutional fund managers. Their subscription is very expensive but very effective.

Some of their notable short recommendations include Lala Tech companies in 2000s, Enron, Allied Capital, Silicon valley Bank and wait for it, Lehman Brothers.

In fact during the hearing of Enron, the judge of the hearing said “How do you explain why you missed the signs that Off Wall Street Consulting Group saw?”

I am hereby attaching a research report published by OWS on PLUG POWER and their SHORT FRAMEWORK, both taken from their website, is free and accessible to everyone.

Disclaimer: I don’t have their subscription. I have just downloaded their free sample report from their website which I feel would be useful to me and the members of the forum. If I sell both of my kidneys AND take a huge loan, I would probably be able to afford their annual subscription fee ![]() .

.

Short Framework.pptx (4.9 MB)

PLUG Short Initiation 6.25.2023.pdf (4.0 MB)

15 Likes

Question is if it’s so expensive how can retail investors access it and any similar research in Indian context

1 Like