Did this happen? I don’t see any new names

Yes, but no new names

Why the company is in ASM list?Is it just because of price run up or any other reason? Where to find these information? please guide

Questions Worth Asking in the Upcoming Q2 FY25 Concall

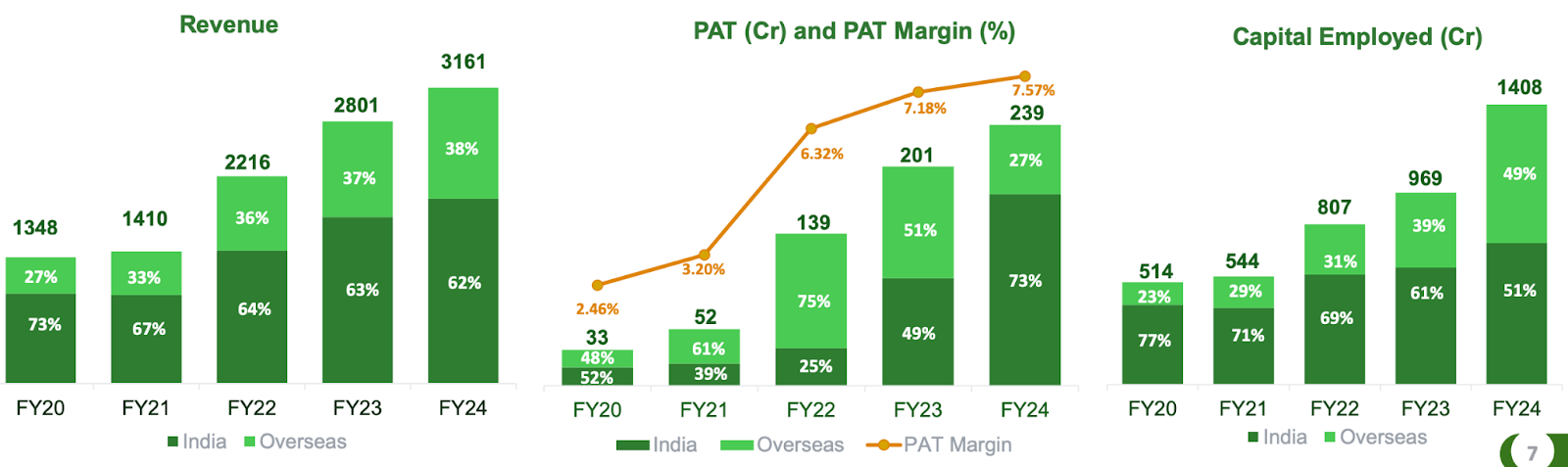

From the above graph, we can notice that while the revenue contribution from the overseas business increased from 36% in FY22 to 38% in FY24, the profit share dropped significantly from 75% to 27%, and the capital employed in overseas operations rose from 31% to 49% over the same period.

- What are the factors driving this disconnect between growing revenue and declining profit contribution?

- What specific challenges have been affecting the efficiency of the overseas business?

- What measures are being implemented to enhance profitability and returns on the increased capital employed?

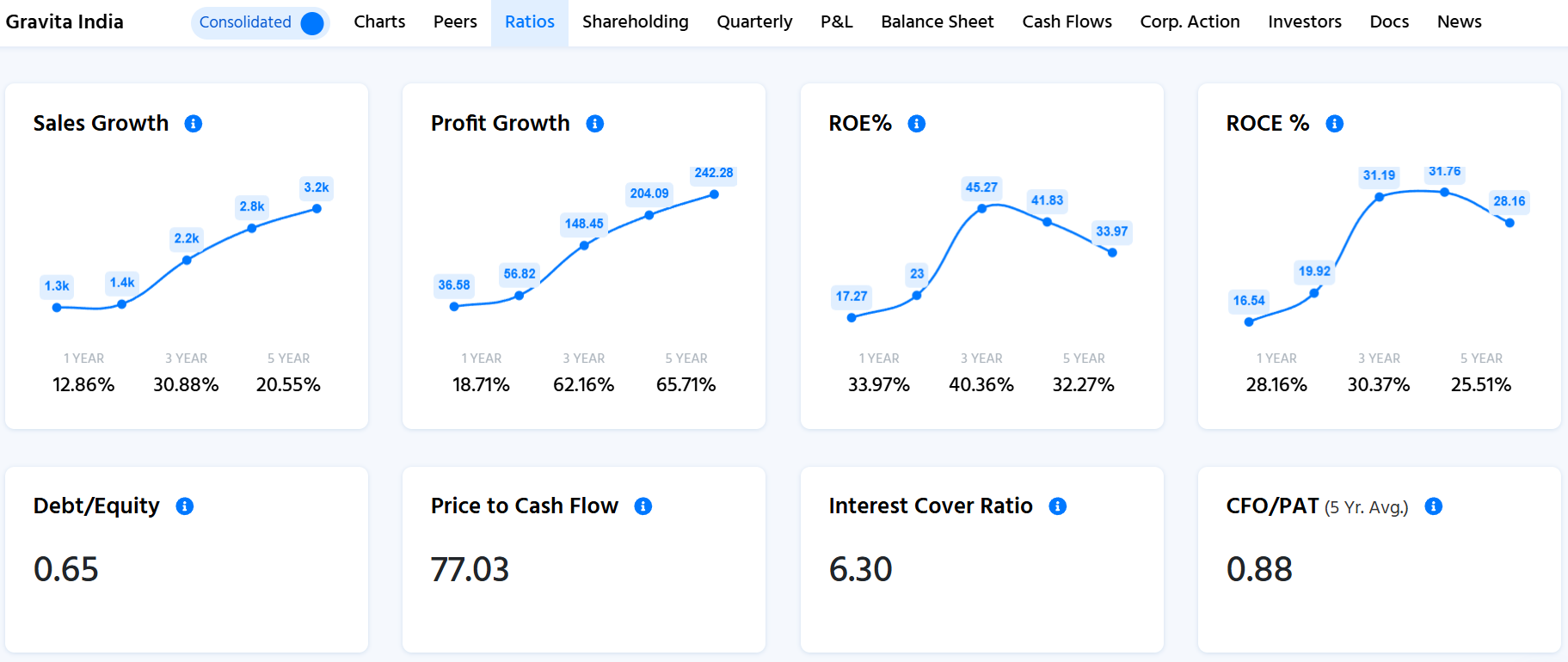

From the above image , we can see that the CFO By PAT ratio is less than 1. It means the company is unable to convert its profit to cash.

Update on the New Overseas Acquisition

Gravita’s subsidiary has signed an MOU to acquire an 80% stake in a waste tyre recycling facility in Romania, which can process around 17,000 MTPA (Metric Tons Per Annum), for ₹32 crore. The remaining 20% will be owned by local partners in Romania.

This move marks Gravita’s entry into the European recycling market, significantly increasing its potential market reach, with Europe’s waste recycling industry valued at USD 155 billion in 2022.

This expansion into new regions and products is expected to be a key driver of the company’s future growth.

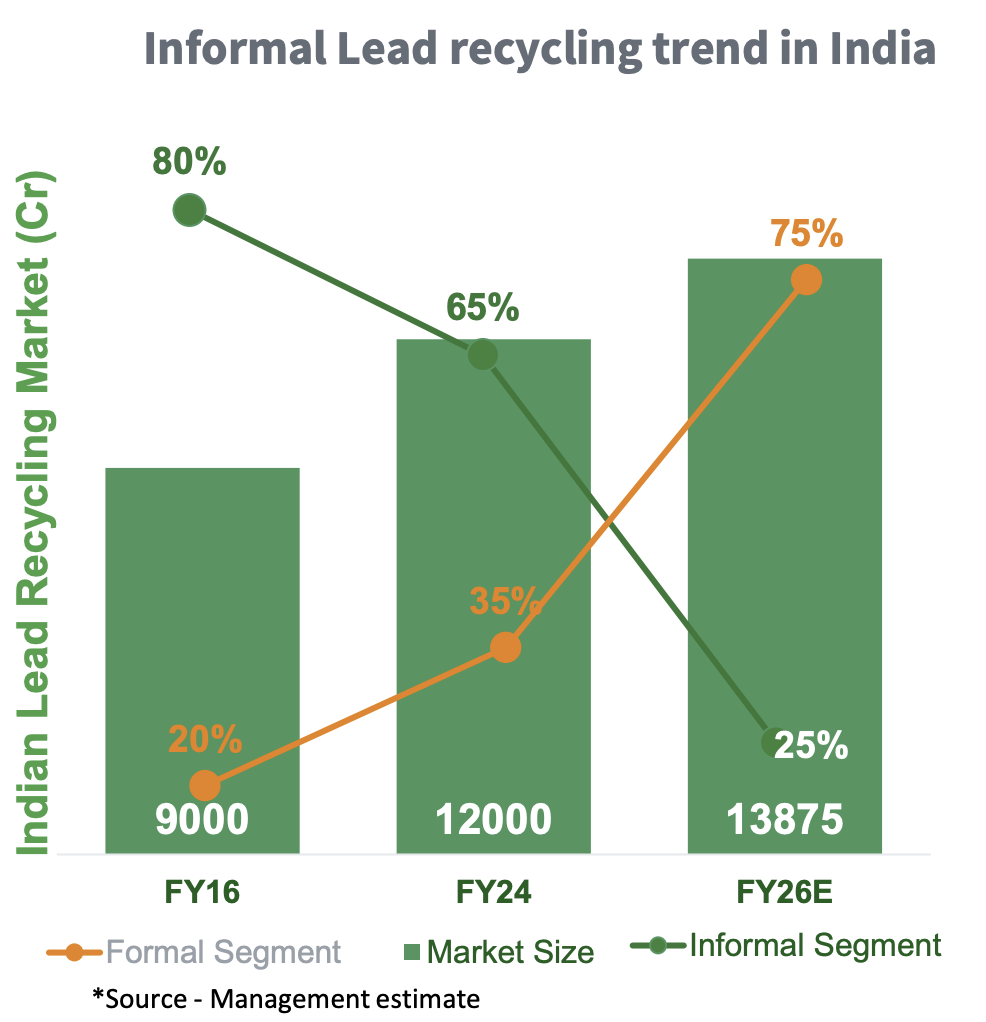

Multidecadal Tailwind in the Recycling Business

India’s battery recycling rate is just ~20%, far below the 60-80% as seen in Western countries.

Currently, 65-85% of recycling is handled by the informal sector.

However, recent regulatory changes are rapidly shifting this trend toward formal, organised players, creating a long-term earnings opportunity.

1️. Battery Waste Management Rules (BWMR): The 2022 BWMR has set the stage for formalising the industry by encouraging investments in collection networks and allowing legitimate recyclers to trade Extended Producer Responsibility (EPR) credits. This is pushing more business towards organised players.

2️. Extended Producer Responsibility (EPR): Manufacturers are now required to take responsibility for the entire lifecycle of their products, including post-consumer waste. They must collect at least 70% of their sold batteries once they reach end-of-life. This means more scrap batteries flowing into the formal channels, boosting business for organised recyclers. The mandate is expected to increase the volume for organised recyclers by 3x to 5x going forward.

The EPR rule mandates that recyclers can only recycle up to their capacity limit. The entity cannot outsource the recycling work. This mandate provides the clear reason for capacity expansion and utilisation within the industry.

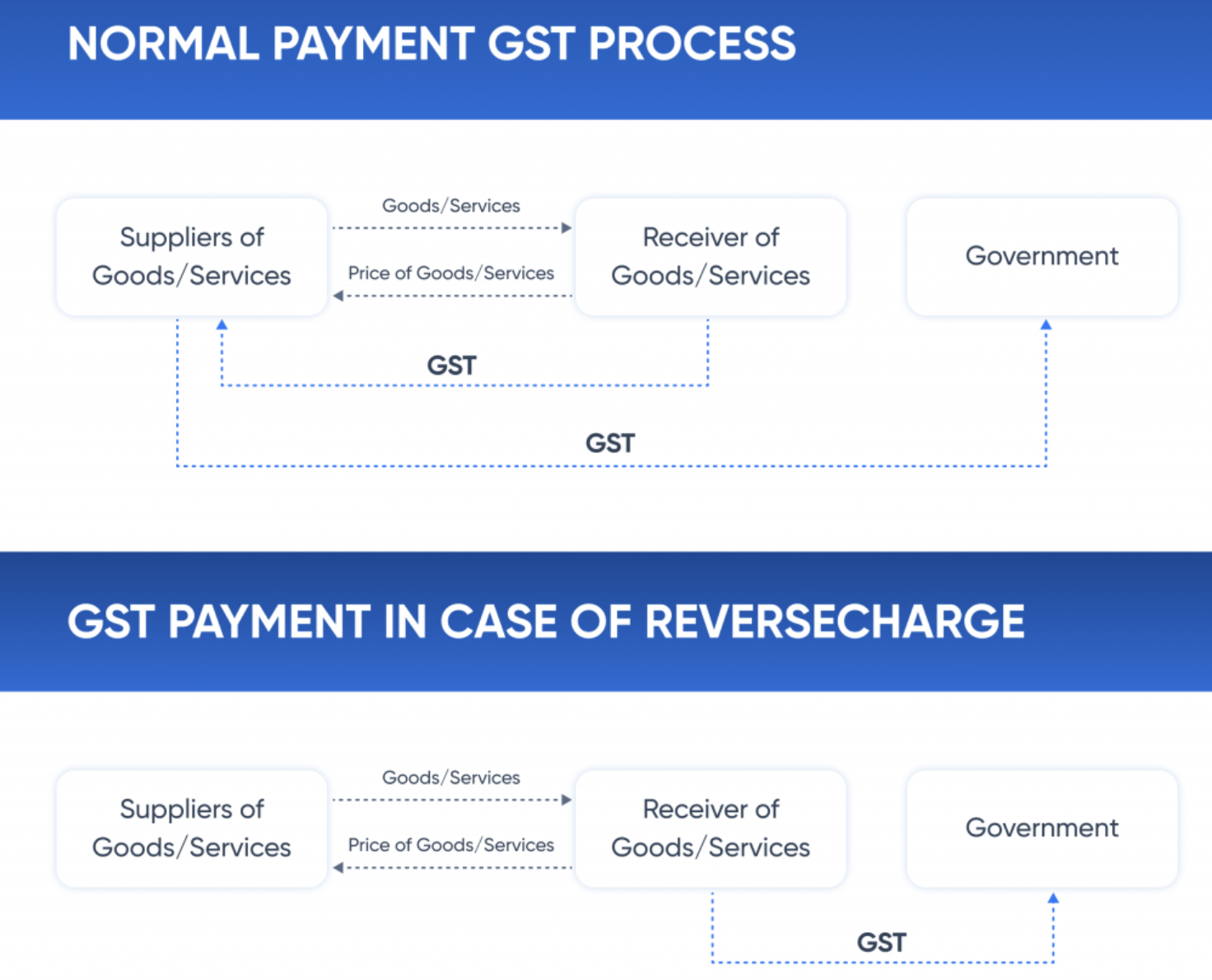

3️. Reverse Charge Mechanism (RCM): Registered recyclers are now required to pay tax on scrap, even if they buy it from unregistered suppliers. This creates a formal tracking system and is expected to reduce the dominance of unorganised players, who currently handle 65% of the market.

The introduction of the RCM is a game-changer in levelling the playing field in the lead recycling market. Shifting the responsibility for GST deduction and deposit to the scrap buyer will effectively reduce the cost advantage that unorganised players gained through GST evasion (18% GST on scrap materials). As a result, it will benefit the organised sector. In our opinion, this could be an even bigger tailwind than the BWMR rule.

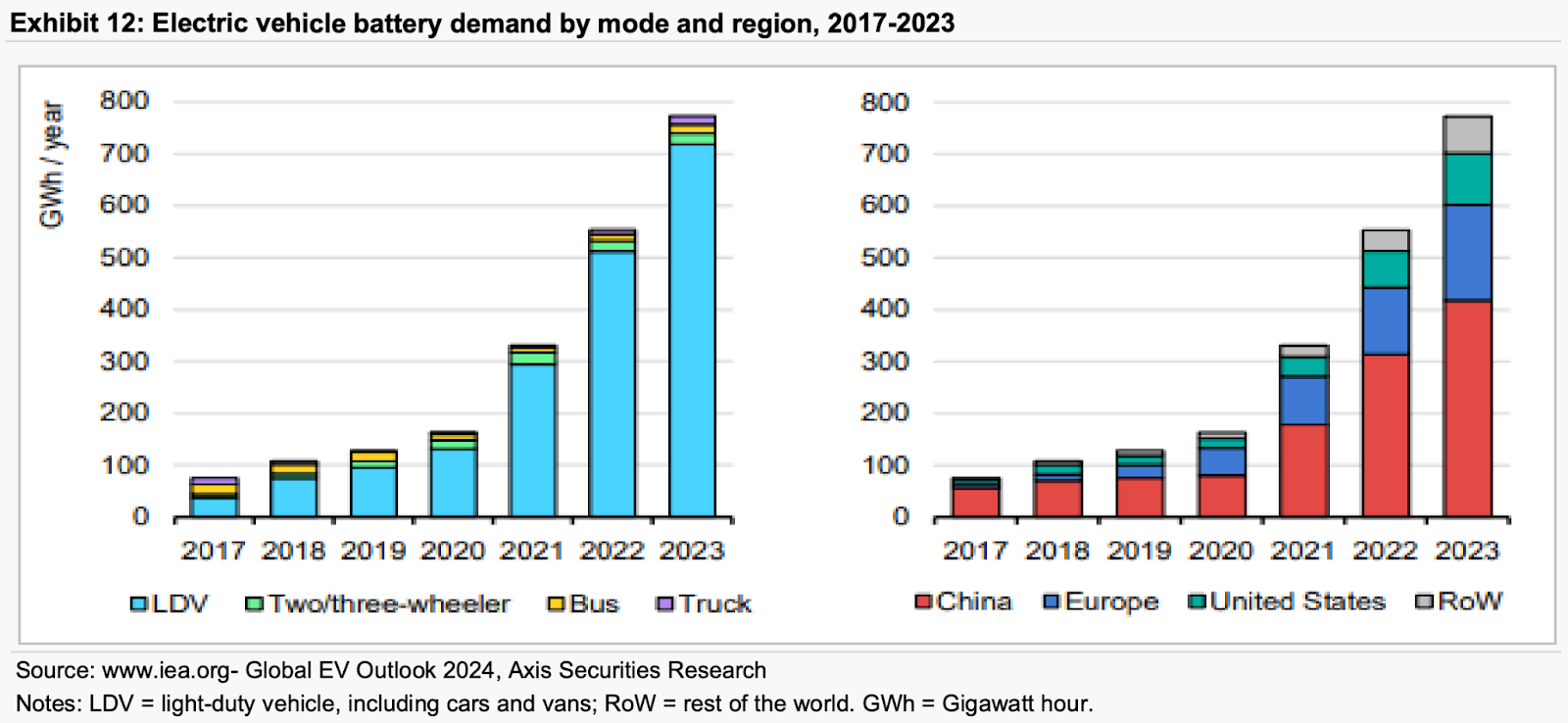

4️. EV Battery Recycling: The global EV battery recycling market is still in its early stages. However, as the first generation of EVs nears the end of its lifecycle (in about 5-8 years), India’s demand for recycling infrastructure is expected to skyrocket. While India’s lithium-ion recycling facilities are still developing, the first major wave of recycled EV batteries is projected globally by 2028-2030, and India will need to step up quickly.

5️. Vehicle Scrappage Policy: India’s Vehicle Scrappage Policy is designed to retire old, polluting vehicles, significantly boosting the battery recycling industry. As more end-of-life vehicles are scrapped, especially older models with lead-acid batteries, the recycling volume is expected to rise.

16 Likes

An explainer on why the Indian aluminium industry is lobbying for higher import duties ahead of Budget 2025. Why India needs more import duties on Aluminium

An article in finshots. Tailwind through regulations.

Similarly, a spike in primary aluminium prices might drive up demand for recycled aluminium, straining supply chains and inflating costs in that segment too.

Few points about the Company -

-

Company though pitching itself as a Recycling company, but primarily it is a lead recycling company. 90% of its Revenue and profits come from Lead. Aluminum, Plastic and Rubber is miniscule. Lithium battery recycling, which company is talking about has still not started. So its business ratios like Margins, Asset Turnover, ROCE are very much dependent on Lead only. Other LOBs does not have much influence. If the lead demand will go down, then the company will suffer big time. And we do not know, the Profitability that the company can generate in other LOBs, as currently it is dominated by lead.

-

Company in the beginning of FY24, said that they would invest 600 cr in the next 3 years. In FY24 they invested total 98 cr and in FY25 H1 they invested total of 27 cr. So they are nowhere in track with their proposed capex, which had to drive the growth for next 3-5 years.

-

Also Company said that they would do the capex from internal accruals only, but wont go for any debt or QIP. This also is quite impossible, as company does not generate that much cash. Co already has about 540 cr debt in their books.

-

Company in the beginning of FY24 said that they will grow Rev in the next 3 years at CAGR of 25% and PAT at a CAGR of 35%. But the way last 1.5 years have panned out, they are nowhere close to their guided number.

-

Giving a PE of 60, to a primarily a commodity producer, of a single metal, does not make sense. If overall demand of lead goes down, this Company will suffer in a big way.

8 Likes

I’ll only give very simple to understand statements -

Lead can be recycled infinite number of times.

EVs will not reduce battery demand for lead acid batteries.

BESS will increase lead demand.

Demand supply mismatch will take lead prices higher.

EPR norms will force recycling by incentivising as well as imposing penalties.

Recycling requires 35-40% less energy compared to extracting lead from ore, significantly lowering production costs and environmental impact.

Overall, Lead recycling will do good.

Lithium, the management is very right in their approach not to start early, as there isn’t enough lithium battery waste available to recycle, considering their scale of operations.

There’s a reason that the management has been able to manage the business with such high ROCE consistently.

6 Likes

Yes, one needs to be clear that they are betting on Lead recycling company, and not a generic recycling company.

Company till now has gross fixed assets of 400 cr but wants to do a capex of 600 cr in the next 3 years.

Company has good ROCE but poor Cash Flow from operations.

Again my question does a company whose 90% business comes from Lead recycling deserve a PE of 60. There is not much tech differentiation in Lead recycling, though recycling is more economical than generation from Lead ore.

But there is a cost involved in collection of scrap and holding scrap inventory.

A better question to ask is if a company guiding to grow bottom line at 35% deserves a PE of 60?

I see Gravita as being in a similar position to where KEI was a year ago. Both companies are experiencing consistent growth of 20-30% and have attracted significant institutional interest due to their reliable earnings. This influx of liquidity has pushed valuations higher. In terms of price movement, I anticipate a similar pattern for Gravita. Like KEI, it’s likely to consolidate within its current price range in the near future until earnings catch up the valuation.

Disclaimer: Exited Gravita recently after holding for 2+ years.

2 Likes

I agree with your points. I’ll also share my understanding. Please correct me if I’m wrong

- Yes, It’s in commodity business but especially Lead , Aluminium recycling but this price movement revolves around several factors such as Whole EV Hype and investors euphoria around it, Goverment’s circular economy push, Fast expansion to cater future demand, Company’s Hedging Mechanism (MCX contract), VAP business, Good ROE, ROCE, ROA, Dividend Rewards etc made this company attractive investment choice for every participants especially in this Bull rally where there’s lot of liquidity.

- While reviewing this company, I observed they have taken debt to fund their expansion which is fine, fast growing companies require capital to grow but this internal accural things also didn’t sit right with me which makes me comes to your 3rd point. Company does not generate that much cash flow and 6/12 years have -ve FCF. How this internal accural thing going to work i’m not sure.

Disc: Have Small position

- Company never generated good CFO or FCF. For last 5 years the ratio between CFO / EBITDA is only 43%. Lot of money is going in the Inventory and Trade Receivables and so cash conversion is very poor. Their FCF is negative for last 10 years. So it is the debt which is funding their growth. For such a company to say in FY24, that they would make further investment of 600 cr in the next 3 years and would the fund the investment from internal accruals only was quite surprising. Now that is changed as the Co. has gone for a QIP of 1000 cr.

- Company has high ROCE / ROCE, becoz they have very high asset turns of 6.5, which was mainly applicable for Lead biz. Now since they are going for massive capex, which is almost 1.5 X of the present gross block, and venturing into other LOBs, will they be able to maintain this asset turn. Has the management clarified this. If not, then going forward the ROCE/ROE shall also come down.

- You are right that the share price is going up, becoz of the EV story, Govt Recycling push etc etc. But company has no proven expertise Lithium recycling, and economics of the same is also not well established. Co. has collection network with the OEMs, which may help them in the biz, but still we do not know how profitable the other LOBs will be when they become significant for the Co. Unless the other LOBs start contributing significantly, we cannot gauge the biz.

- Even the Company’s revenue / PAT/ Capex guidelines are also going all over the place in the last 2 years.

- Given this background giving such a high valuation to the co, looks dicey to me.

4 Likes

Summary of Gravita India Ltd. Investor Presentation Q3 FY25

- Corporate Overview: Gravita India, established in 1992, has diversified its operations to include lead, aluminum, plastic, and rubber recycling, with an ambitious growth vision.

- Financial Performance (Q3 FY25): Achieved significant year-over-year growth: 33% in volumes, 31% in revenue, 29% in PAT, 14% in EBITDA.

- Vision 2028: Aims to become a top global recycling company, targeting 25%+ volume CAGR and 35%+ profitability growth by enhancing capacity and innovation.

- Strategic Investments: Raised ₹1,000 crore through QIP to support expansion and operations.

- Sustainability Commitment: Initiatives include a focus on renewable energy, ESG goals, and innovative recycling technologies ensuring operational excellence and environmental preservation.

Summary generated by FinDL.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/78df8811-9049-4f58-b26e-25538d8e4405.pdf

2 Likes

You are right about valuations. Valuations was the main reason I bought POCL over Gravita last year. They are in the same business, do a good revenue and also have the same growth plans as Gravita.

They only lack in their margins which Gravita has mastered by capturing Africa and a plant in Kathua.

POCL is already 6x from it’s last year valuations. But I like Gravitas current valuation too and have added to my small PF.

Invested in both POCL and Gravita with 6 and 3% of PF respectively.

3 Likes

ROCE and ROE of POCL are way off than GRAVITA. No wonder GRAVITA enjoys a higher PE multiple apart from higher OPM. Not to undermine POCL performance though. Industry tailwinds are pushing both stocks

1 Like

Hi have just started following the company. My understanding is that majority of the revenues comes from Lead Recycling, but battery manufacturers like Amara Raja have started their own recycling operations, has management commented on the impact of something like this earlier and would it impact their growth plans?

- This is relatively old news, and management has already addressed it in previous conference calls.

- Amara Raja’s plant is located in South India, while their sales are pan-India. Gravita can still handle recycling for them in regions outside the South.

- Amara Raja is not the largest client; the Tata group accounts for 20-25% of the total battery collection.

4 Likes

- Gravita India, announced plans to invest Rs 2,500 crore in the business over the next 3-4 year

- Company has fully cleared its debt in India and aims to continue its debt reduction efforts moving forward.

4 Likes

in the interview, he says RCM and EPR.

can anyone please help understand these 2 abbrevations ?

EPR - Extended producer responsibility

RCM - Reverse charge mechanism

5 month old interview ![]()

2 Likes