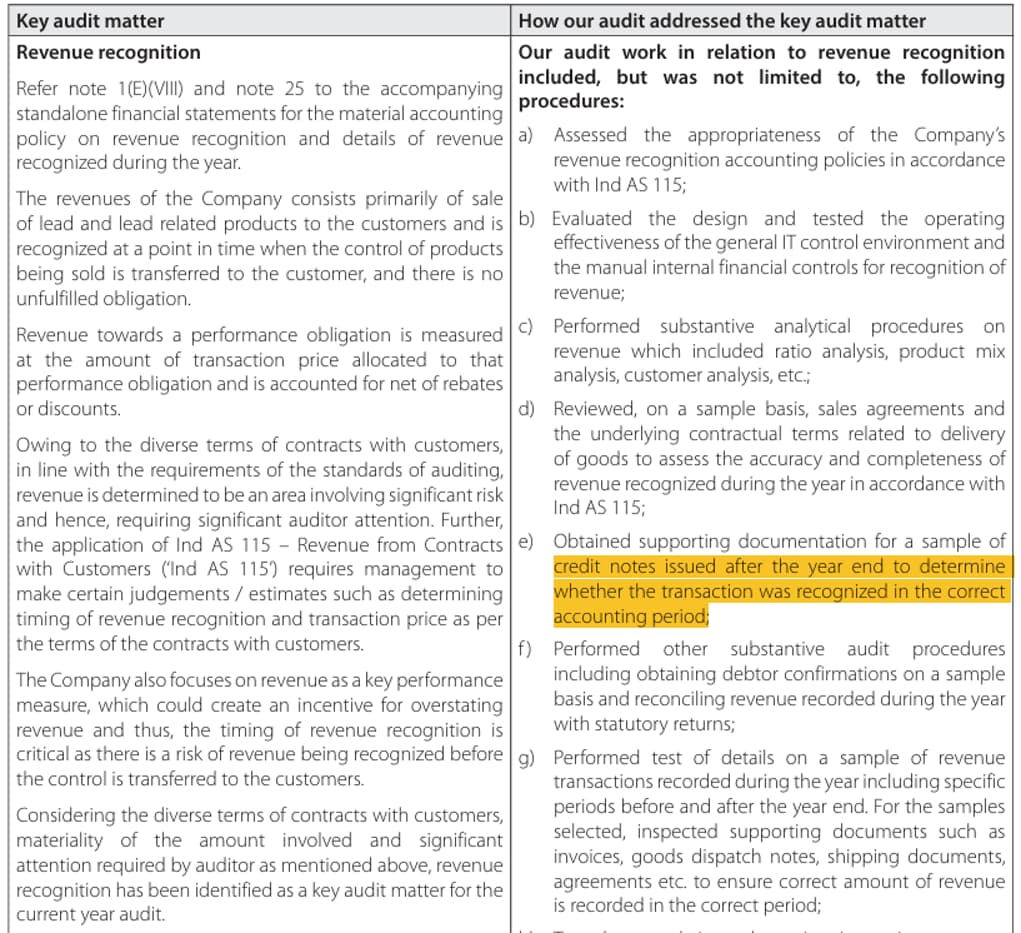

It appears Auditor has qualified their annual report for

revenue recognition - it is unclear about exact cause but I guess auditors are not blunt while giving qualifications

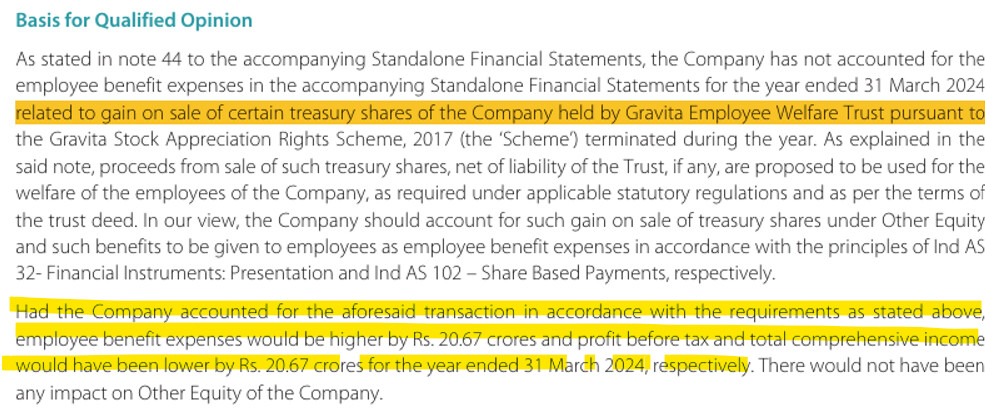

Company has not accounted for 20cr employee benefit expense via P&L

isnt this a red flag for company that has not generated lot of FCF?

Fundamentally, major profitability lies in Africa business - how to gain confidence that same would sustain over medium term reason for Africa business being this profitable could be lower compliance cost and informal sourcing.. any color on this? they have 55% market share in Ghana

Any thoughts on the results? Is anyone planning to attend the conference call?

They are counting big on rubber recycling, The estimates for Capacity in the Q4 presentation for FY28 are 7.27 lakh MT as against 5.05 on Q3 presentation. The capex plan has also increased to 1500 Cr from 600 Cr.

Will management be able to deliver on such high expectations, given that they have missed the initial goal of 2025 expected capex. Also does anyone see any impact of trade wars?

Summary form Q4 results PPT and transcript. Please feel free to suggest views/edits.

Is that an expensive choice at current PE of 45 Vs 3-year median PE of 27.4?

Future Guidance Gravita has outlined an ambitious VISION 2029 roadmap with specific targets. Key guidance points include:

Volume CAGR:** Targeting 25%+. Management expects volumes growth for FY26 to also be around 25%, potentially ranging from 20% to 30% depending on the pace of capex execution.

Profitability Growth:** Targeting 35%+. The company has historically surpassed this, with a 5-year PAT CAGR of 57%.

Upcoming Capex Total Capex Plan:** Rs. 1500+ Crore planned by FY 2028.

Revenue, Profits, and Financial Performance

Revenue: INR 3,869 crores, up 22% YoY.

Adjusted EBITDA: INR 404 crores, up 22% YoY. EBITDA margin stood strong at 10.43%.

PAT: INR 312 crores, up 31% YoY. PAT margin increased to 8%.

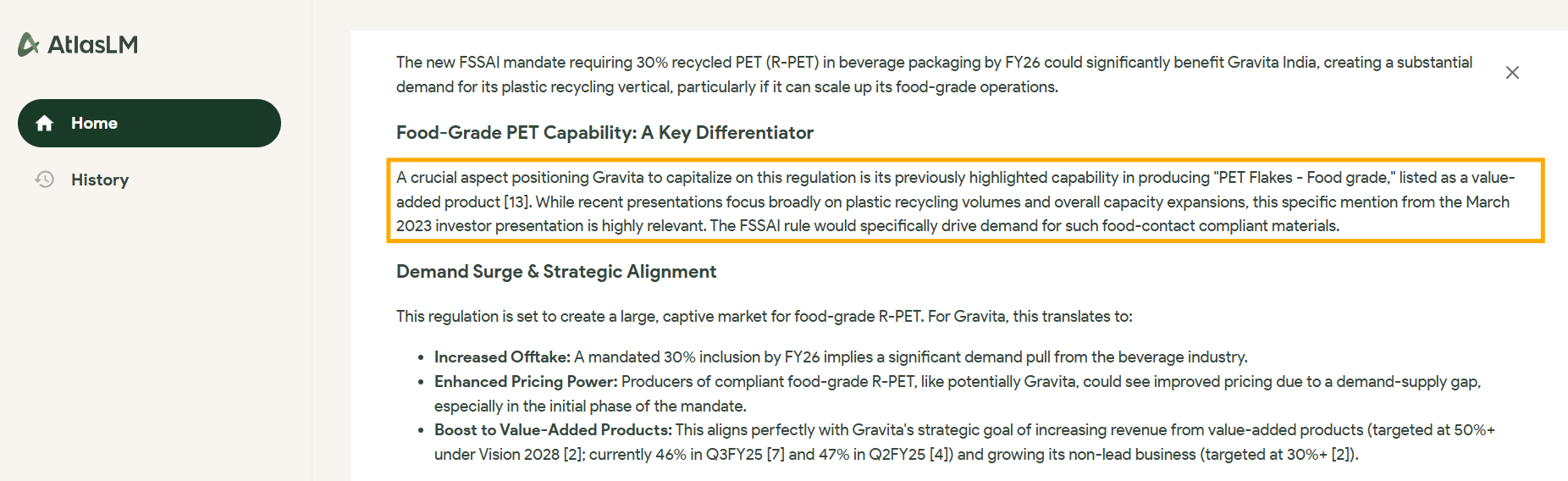

Food Safety and Standards Authority of India (FSSAI) notifies Recycled-PET Material Norms for Beverage Industry. New FSSAI rules as per Environ Min Rules mandating 30% recycled plastic in PET packaging by FY26

agree..but as I said, Gravita is a matured recycler which has nailed down most of its raw material and plants. POCL is an up and coming story where they are still sorting these things out.

I am expecting POCL to reach the heights of Gravitas eventually.

i think gravita is well diversified but pocl is working in highly niche segment. So, pocl also needs to diversify if they really want to achieve new heights. my 2 cents.

From what I see Gravitas PET & plastic recycling segment is 2-3% of its business as of now. They aim to increase this by FY 28. In the medium term I don’t think we will see much change

Net Profit: ₹93.3 Cr vs ₹67.3 Cr YoY – up 38.6%

Revenue: ₹1,040 Cr vs ₹908 Cr YoY – up 14.5%

EBITDA: ₹101 Cr vs ₹87.7 Cr YoY – up 15.1%

EBITDA Margin: 9.68% vs 9.66% YoY – flat

Takeaway:

Gravita India delivers another quarter of steady performance. Double-digit growth with margin stability reflects strong operational control and business momentum.

Management mentioned that growth will not be linear despite non cyclical nature. Minor fluctuations will be there. Sometimes volume growth will be 22%, sometimes it will 28%. Overall it will be around 25%.

Any idea why the stock is seeing continuous erosion? Fundamentally, company seems to be doing great and is headed for good growth with capex being put into operation. One issue which I keep seeing is promotor reducing stake frequently. But then many times promotors do that. Is this the only reason? Surely market knows something which we don’t know. Can anyone throw some light on this?

No particular reason, there can be many reasons behind promoter selling. May be they want to build some other personal assets, may be they want to just sell the stake and spend on their lifestyle. or may be they think stock’s valuation has become insane.

Just because promoters are selling, it does not mean company will not do well in future. There are so many companies in the past where promoter sold their stake consistently and stock price did well despite the promoter selling spree.

Gravita has reported a steady performance in H1FY26, showcasing consistent strength across both operational and financial parameters in all major business verticals. Staying true to its VISION 2029 roadmap, Gravita is strategically expanding capacities across its core businesses—lead, aluminium, plastic, rubber, and turnkey solutions—with a target of crossing 7 LTPA by FY28. Simultaneously, it is scaling up new growth avenues such as lithium-ion, paper, and steel recycling. The company remains committed to achieving over 25% volume CAGR, 35%+ profitability growth, and 25%+ ROIC, while steadily increasing the share of value-added products beyond 50% and non-lead segments above 30%, underpinned by strong ESG principles.

Coming to Q2FY26 performance, Gravita saw YoY growth of 4%, 12%, 10% & 33% in volumes, revenue, EBITDA, and PAT respectively, maintaining a healthy ROIC of 25%. Growth in value-added product contribution and domestic scrap sourcing underscores the company’s integrated model and efficiency gains. Backed by robust supply chain efficiency, capacity augmentation, strategic diversification, and consistent execution under favorable government policies, Gravita is well placed to drive long-term value creation.

The company remains committed to achieving over 25% volume CAGR

But in Q2 26, volume growth is 4%. How will they fill this huge gap in reality and ambition? Only silver lining I see is they have maintained the margins however I would have expected some increase there as they claim move value added products offering.