Margins deteriorating because of cost pressure. Debt has increased. There is lot of Capex build and still there is not light on cashflow generation. Looks like market share is being gained at the expense of margin.

Granules Q4-Fy23 con call notes

General

-

Problem with distribution - missed shipment and penalty. Moved to a new PLM provider, and it will be complete by the End of May 23

-

Expect to grow at 20% over the next few years.

-

Price erosion has stabilised, and do not expect higher.

-

Margin expansion will happen due to a better product mix. Overall it will be better even on a yearly basis. API to FD conversion for paracetamol.

-

Getting offers from various investors to participate in CZRO (Green initiative) through debt or equity.

-

Aiming for Net debt/EBITA will be around 1

-

Expected to complete Enzyme-driven API in next few quarters.

-

US packing facility will reduce working capital, and it will be fully operational by Sept 2023

-

MUPS blocks- 1 asset turn, and expect it to be 2 this year. Gross block for MUPS- 240 cr.

-

Failure to supply cost is 8 cr. Sales lost of 4 to 5 million- April may have some challenges. Hopefully, this should done from June onwards.

-

Paracetamol- Market share increase in US/Other parts of the world. Pricing reduction in line with PAP reduction.

-

Hope to establish a green initiative in the next 1 to 2 years.

-

Next two years

- R&D (more than 3% of sales in Fy24/25)

- Green chemistry.

- establish green credentials.

-

30% of the global market share. It can go to 50% of the global market share. Green chemistry will help us do it.

-

The green chemistry-related pilot has been established at 100 kilos.

-

Current chemistry used for DCDA is very pollutive.

- Demonstration 100 kilo/Day./. Next is 1 ton/day. Once we prove the main

- Next one 10 ton/day

- When Granules reach 30 tons/day - we will be able to serve 70-80% of global capacity. -

Margin shall improve from Q2 onwards. Q2 margin shall be the benchmark. revenue shall also increase

-

From Q2 onwards, some control substances in the US (MUPS product) and Europe launches.

-

Parcetamol API has lot of competition. But for PFI and formulation, we have huge demands.

-

We are licensing our product in US/Europe/African and Asian markets. Huge demand for Paracetamol

Capex

- FY24-

- 250 cr CRZ (DCDA and PAP green KSM). Expect the pilot to sept end. Commercial product of other KSM in FY25/26.

- 250 cr Lifesicien

- 200 cr regular

- total capex of 700 cr this year.

Europe

- Sell Paracetamol in Europe- Germany/UK/Hungary- Plan to expand it to full Europe this year.

My view:

Overall, I think Granules is going through the biggest transformation so far. They are betting heavily in terms of huge Capex and new technology, which is not yet tried or tested.

If they succeed in Green Chemistry, then they will establish their credential in the green ecosystem. Of course, after three years, if they came out as they are saying now, it will be a different Granules, but until then, the market will fret and doubt and would like to see their green execution before seeing valuation improvement.

Note: Long time Invested

10 Likes

PFI share has gone down to APIs. Guessing it has more to do with product mix change. Would love to see the momentum in the opposite direction though.

1 Like

I’ve no doubt that once they prove their capabilities in green chemistry in the next couple of years, there will be another, as yet unforeseen, capex cycle.

FCF ko bhool jao. At best it will be a trickle.

Red Queen Effect & all that.

D: Long time investor.

4 Likes

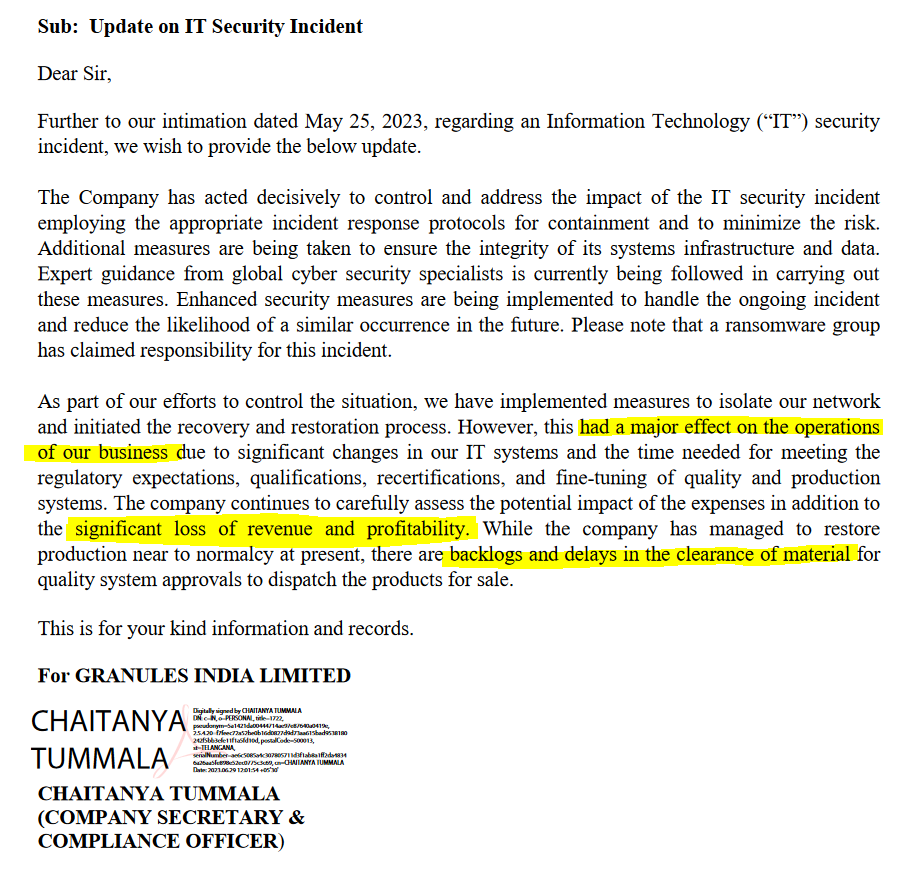

This seem to have happened in May. Why are they announcing so delayed?

2 Likes

Q1 might be a washout.

@ksaravanan The company admitted it in May itself. 615df5e3-bf68-4cae-8116-df5cdc0116a7.pdf (bseindia.com)

5 Likes

Q1FY24 results are out and as expected degrowth in revenue but substantial erosion in margins (due to loss of revenue while expenses incurred). While this could be one off but investor presentation doesn’t talk about what is revenue and profit guidance for rest of period unless I am missing something.

1 Like

From investor concall…loss of revenue estimate of Rs.150 Cr and failure to supply penalties of Rs.21 Cr …these are kind of one off …

R&D Exp of Rs.43 Cr in Q1FY24…expected to go upwards of Rs.50 Cr in subsequent quarters of FY24

Gradual improvement expected in Margin from Q2 onwards but management declined to confirm any guidance around revenue & margin for rest of FY24…

They also discontinued giving molecule wise sales break-up because of competition

3 Likes

As per latest concall, Management is expecting a high R&D expense in Q4. Paracetomol & Metformin Sales Price declining. They are keeping the margin but topline is reducing for top products. New facility Commercialization maybe in FY26. They are introducing new Products (FD) in US & applying for approvals in Europe.

Management is not giving guidance. They are talking about a lot of Capex and I can not get a clear picture on how & when it will improve revenue.

I have a small position now but do not have a clarity to increase investment. Any Opinions on how you are tracking thier performance?

2 Likes

Looks like they want to move to FD to improve the margins.They have hired a new CMO as well. A couple of qtrs back, then new CEO Dr. Ramarao said, the focus then onwards is going to be on Cash flow generation. They have completed lot of capacity expansion and it should support in revenue expansion. However, I am not sure why most of the capex is driven through Debt and not done with internal accruals.

2 Likes

Although they are talking about cash flow generation, they are unlikely to in the immediate future for the following reasons:

-

CRZ (Green) invests more than 1000 cr in that green field facility. Although the first DCDA plant is getting operationalised in Q4-24, it is likely to generate revenue from Q4-Fy25 onwards. As they will be replacing DCDA sourced from China with internally generated DCDA, I am not sure if they will even save a lot in terms of cost because imported DCDA is cheaper.

-

The PAP plant is kind of a long shot. They will start in that plant next year, but it will be operated in FY26, which is further away.

-

For the last 2/3 years, they have been talking a lot about MUPS block. Although the block is operational, they are not able to generate much revenue from it yet for one reason or another. They do not even talk about it in their con call.

Historically, Granules has always relied on debt to fund its expansion. API is a capex-heavy business where they need to invest heavily to create capacity and needs a lot of money for working capital for FD.

Hence, their dependence on debt will not reduce; in fact, it may increase as they invest even more in green chemistry projects in CRZ.

7 Likes

SVP Operations - API manufacturing head has resigned from the company.

There seems to be a string of changes at the senior management level. Does anyone have any idea why this is happening?

I see a block deal on MIT trendlyne.

1 Like

Granules India has received approval for its generic version of Trazodone tablets. This is a positive development as it expands Granules’ US market presence in the anti-depressant segment. Expect increased revenue and profitability from this product in the coming quarters.

3 Likes

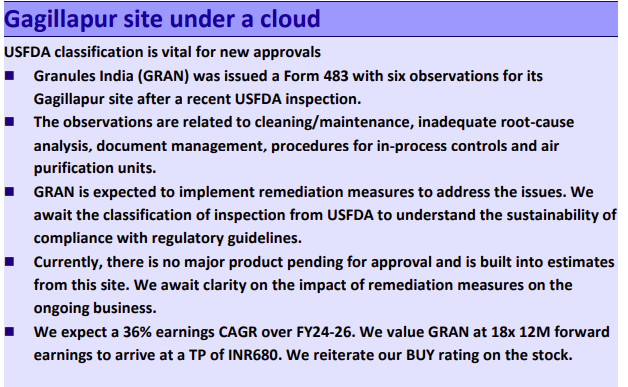

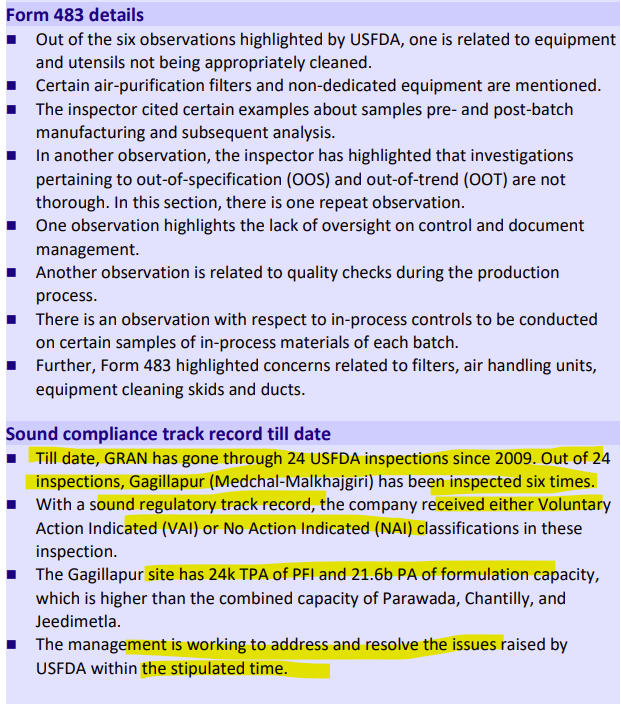

The recent crash in Granules share price is a nightmare for small investors and this is precisely the risk of overdependence on US market. In normal situation this should have been an opportunity to buy, but given the seriousness of FDA observations, it would be naive to buy without knowing the details of repercussions. At the sametime Motilal has given a buy call.

So learned friends with domain knowledge may throw light on it and expected turnaround in companies business. As there is no doubt about the quality of the management here, there is no risk of company evaporating.

4 Likes

Regulatory hurdles, market competition, and fluctuating raw material costs are on way ahead .

2 Likes

Is Motilal trying to give exit for big investors by spreading the loss to many (retail) investors?

1 Like

Looks like Fidelity India focus fund has increased its positional size in Granules.