They reduced the position from 5.23% to 2.73%

4 Likes

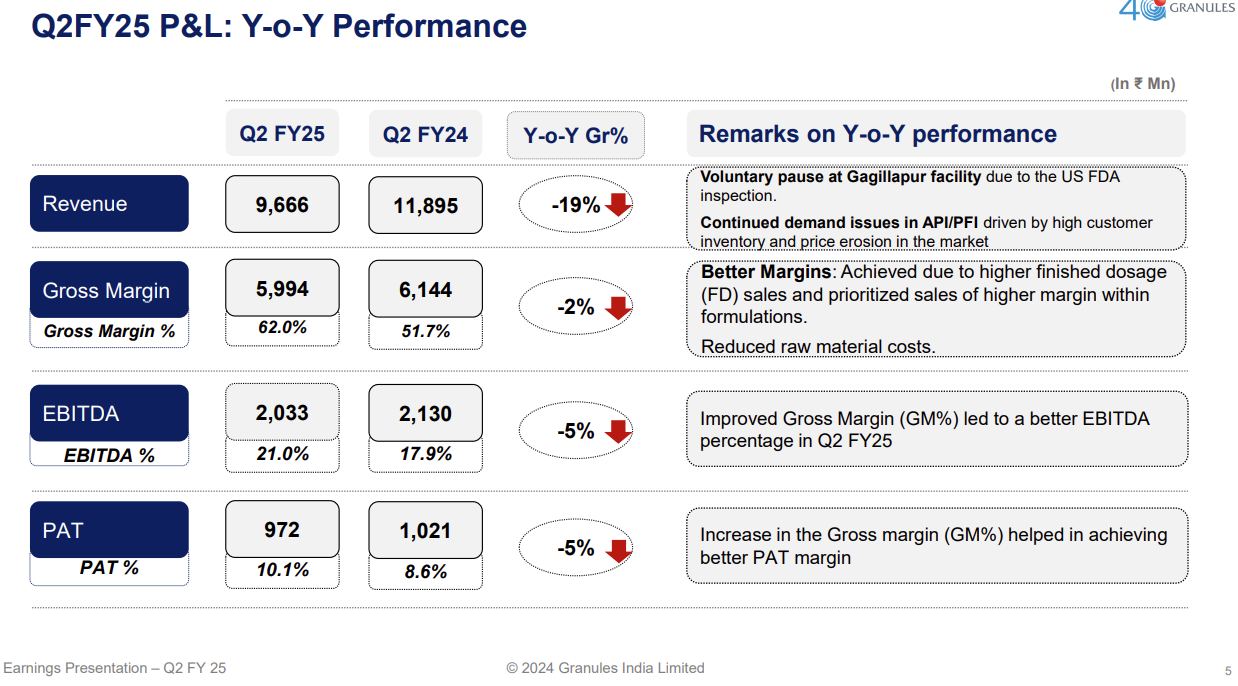

Granules Q2 FY25:

https://nsearchives.nseindia.com/corporate/GRANULES_06112024132254_NSEBSEINVESTORPRESENTATION.pdf

Disclosure: Invested

2 Likes

Management informed:

"This is regarding our communication dated September 07, 2024, about the US FDA

inspection of the Company’s facility at Gagillapur, Hyderabad, Telangana and the issuance of

Form 483 with 6 observations.

US FDA has classified the inspection as “Official Action Indicated” (OAI)."

Any inputs, from fellow VP members, on what could be the impact of this OAI on revenue / profitability.

Disc: Not Yet invested, but Tracking from quite some time.

Official Action Indicated (OAI) is a classification given by the US Food and Drug Administration (FDA) to a facility that is not in compliance with current good manufacturing practices (CGMP). The FDA notifies the company of the classification within 90 days of the inspection.

An OAI classification can mean:

- A facility has been cited for egregious violations related to food safety

- A facility has an uncorrected Voluntary Action Indicated (VAI) condition from a previous inspection

- A facility has a condition that poses an imminent health hazard

- The FDA may withhold approval of pending applications or supplements from the facility

An OAI classification does not immediately impact existing production or revenue, but it can lead to:

- Blocked new product approvals

- Further regulatory actions, such as warning letters or import bans

- Increased remediation costs

6 Likes

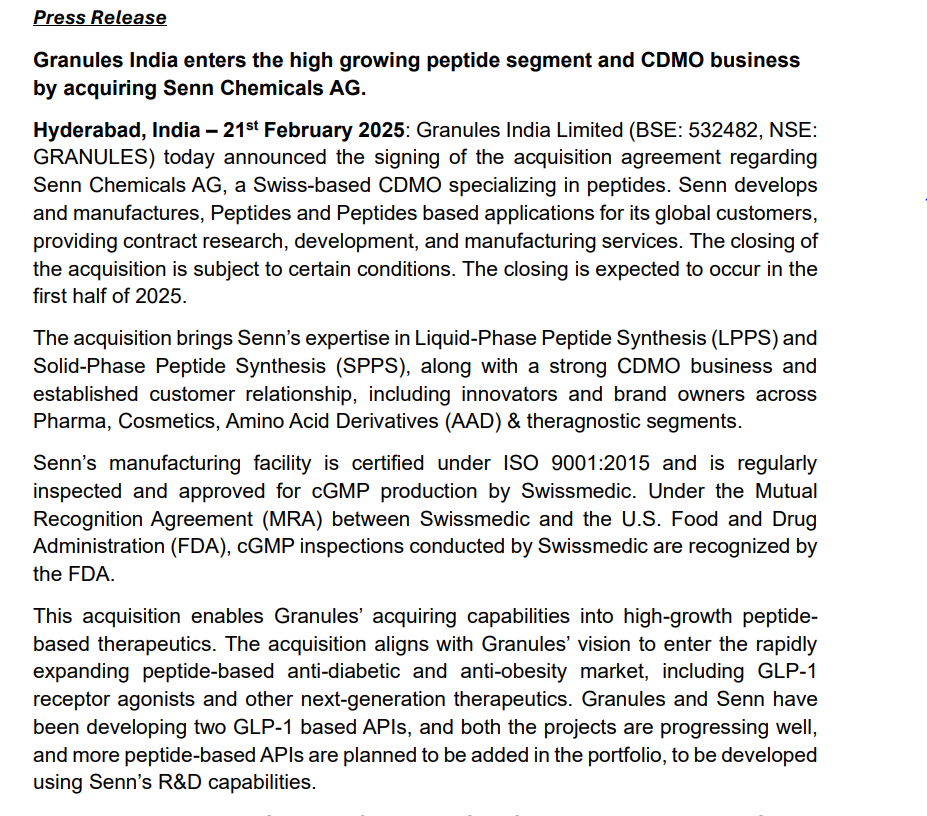

Finally Granules in moving into peptide CDMO by buying 100% of Senn Chemical AG for 192.22 cr

4 Likes

Q4 FY25: * Flat results from the company.

-

Revenue: ₹1,197.4 crores (+2% YoY).

-

Gross Margin: 63.4% (vs 60.1% YoY).

-

EBITDA: ₹252.4 crores (21.1% margin).

-

Net Debt: ₹706 crores (improved from ₹842 crores at start of year).

-

Cash-to-Cash Cycle: 202 days (vs 213 in Q3).

FY25 Full Year: -

Revenue: ₹4,481.6 crores (flat YoY).

-

Gross Margin: 61.5% (↑635 bps).

-

EBITDA: ₹945.2 crores (+10% YoY).

-

R&D: ₹238 crores.

-

ROC: 16.6%.

-

There is a major impact because of the FDA inspection at Gagillapur facility

Gagillapur FDA Inspection: -

August 2024: Inspected; six Form 483s issued.

-

February 2025: Warning letter received.

-

Manufacturing continues but with slowed operations due to remediation.

-

Over 1,200 batches and 2,600 swabs tested—no contamination found.

-

Remediation guided by three global consultants; expected to continue for 1–2 more quarters.

-

Remediation Cost: ₹60 crores in FY25; will continue at a lower level in H1 FY26.

-

For a Company of 12K crore Market capital, it is investing ₹1000 crores in Capex of which 300+ is already spent and remaining to follow.

-

The company wants to pivot from API, PFI manufacturing to FD, to move up in the value chain.

-

Looks like it is in transition towards with Peptides and oncology products.

1 Like

Remediation & Operational Impact

- Remediation measures have impacted Q4 results and are likely to continue affecting performance for the next two quarters.

- Expenses: Incurred ₹60 crore at Gagilapur for third-party consultants, travel, and remediation in FY25.

R&D and Capex

- R&D Spend: Increased from ₹199 crore to ₹238 crore, a 20% rise year-on-year.

- Capex on Peptides: Investments ongoing in both Switzerland and India, targeting large-volume peptide products.

- Overall Capex Target: ₹600 crore, including investments in Seen Chemical.

Subsidiaries and Strategic Moves

- Seen Chemical: Currently at or near breakeven. This situation may persist for another 2–3 quarters, after which a new strategy will be implemented.

- Innovator Targeting: Focusing on some innovator products. High-volume GL1-related products are likely to be manufactured in India.

Sales & Product Pipeline

- Europe Sales: Recently driven by Paracetamol API. However, future growth will focus on formulation launches, which were delayed but are expected to proceed going forward.

- Oncology Platform: One product filed; approximately 10 more in the pipeline. This segment is expected to start contributing meaningfully from FY28 onwards.

2 Likes

Statement by Krishna Prasad Chigurupati, Chairman & MD, Granules India – CNBC-TV18

On Flat Performance:

- The flattish performance is primarily due to capacity constraints.

- We’re currently undergoing remediation at our Bonthapally (Bagalapur) facility, which has resulted in a 10–15% drop in production. The main issue is supply-related, not demand.

- Our new Gagillapur (GLS) plant, with a 10 billion unit capacity, has been successfully inspected by the US FDA. We expect approval in the next one to two months. Once approved, this will help us overcome current supply issues.

On Facility and Regulatory Updates:

- The Bonthapally (Bagalapur) facility under remediation is expected to be reinspected by the FDA and should be cleared by Q3 FY25.

- From Q4 onwards, we expect to see a significant improvement in performance.

On Demand and Order Book:

- We have a strong order book.

- With an additional 20–25% capacity, we believe we can easily sell everything we produce.

- The FDA inspection went well, and we are confident about upcoming approvals.

On Margins:

- Gross margins have been improving, and as revenue increases, we expect a healthy margin expansion.

- We are confident of seeing quarter-on-quarter improvement, particularly a strong Q4 performance for the full fiscal year.

On Paracetamol and US Manufacturing:

- The paracetamol API contributes about 10% to our revenues.

- Globally, there’s sufficient capacity for paracetamol.

- For normal generic products, even with a 25% import duty, it still doesn’t justify manufacturing in the US.

- We do have a manufacturing facility in the US, but that focuses on higher-margin, niche products, especially in the CNS and ADHD therapeutic areas.

- Generic manufacturing in the US still doesn’t make economic sense for most products.

On Duties and Impact:

- Any duties imposed will eventually impact US consumers.

5 Likes

-

Granules had a meeting with the U.S. FDA regarding the Gagillapur facility. This was only a meeting, and the FDA may conduct unannounced visits in the future. Management sounded optimistic during the call, expressing intentions to resolve all issues by Q4. However, considering the average time taken for import alerts, it is more likely to be resolved in Q1 or Q2. Management appears to be raising investor expectations by sounding overly positive.

-

The GLS facility in Genome Valley, Hyderabad, with a capacity of 10 billion, is now operational and has successfully passed a U.S. FDA inspection. This provides a second source of supply for finished dosages (FD) and pre-filled syringes (PFS) to the U.S. market from India. Some prescription products currently sold through Gagillapur will now be supplied from the new facility.

-

Around 4 to 5 products will be transferred from Gagillapur to the Genome Valley facility.

-

Once the import alert on Gagillapur is lifted, the company expects to sell more new products and approve some pending products.

-

Remediation expenses are approximately $2 million per quarter for Q1 and Q2, and these costs are expected to decrease in Q3 and Q4.

Growth Drivers:

- CND-ADHD products from the GPI facility in the U.S.

- Scaling up large volume products in the U.S. and Europe.

- Moving up the value chain in Europe.

- Monetization of the oncology facility in Unit 5 (management has been targeting this for several years, setting up Unit 5 long ago but with limited success to date).

- Peptides through Senn Chemical (medium to long-term potential).

- Even a breakeven performance would be positive. The Indian market will take years to generate meaningful revenue, so expectations should remain low on this front.

Regarding Senn Chemical and Ascelies Peptides:

- Ascelies operates as a separate legal entity and works at arm’s length from Granules India.

- The Swiss facility serves as the global R&D and CDMO hub. Ascelies will act as the scalable manufacturing and R&D backbone from India and has set up a peptide R&D center in collaboration with IIT Hyderabad.

- They reported a loss of 20 crore in Q2 but aim for profitability by Q4 FY27.

Note- Invested

3 Likes

As per this article, Granules in planning to raise money (first time in the last 8 years as they raised money through QIP in 2017 at 120 per share).

- I’m not sure why they are doing a private placement. It seems like they may be looking for a major investment, reducing debt, or anticipating some contingent liability. However, in the last conference call, they mentioned they were comfortable with their debt levels, so this announcement is a bit surprising.

- They are likely to raise funds around the current market price (CMP), with a 3–5% discount. Once the funds are raised at that level, it usually becomes a price floor. For example, if the CMP is 580 and the private placement is done at 560, then 560 typically acts as a support level for the stock over the next few months, unless something drastic occurs.

Note- Invested

1 Like

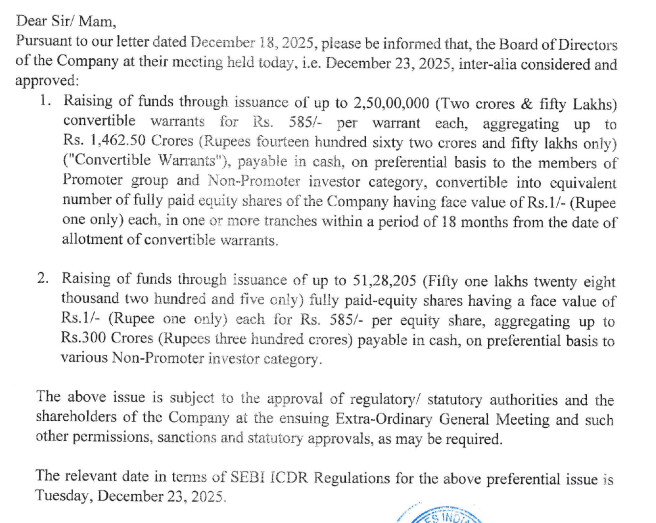

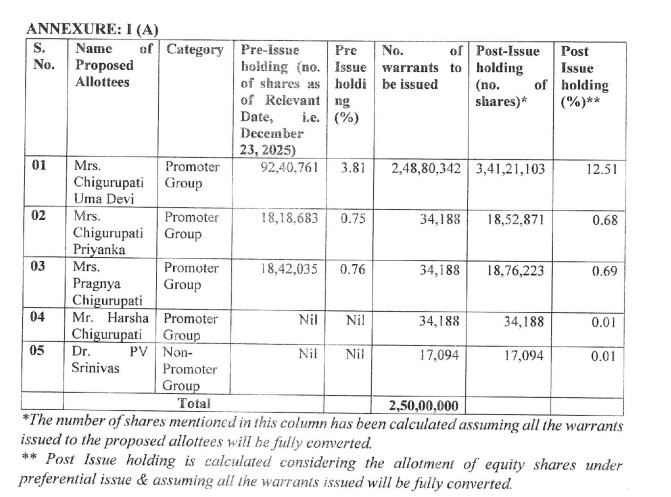

They are going to raise approx. Rs. 1462 Cr. (mostly from Promoter family) via issuing warrants, and an additonal sum of Rs. 300 Cr. via private placement (mostly from 360 one backed funds) all at Rs. 585 / share.

Wondering .. Ye promoter log kahan se leker aate hai itna paisa to invest as fresh capital. Granules ka to Dividend Yield bhi miniscule hai :)

https://www.bseindia.com/xml-data/corpfiling/AttachLive/dcbcc32c-e356-495b-a0e1-e0b10b816c33.pdf

Disc: Invested.

2 Likes

Good point.Sudden large fund infusion by promoters at 585, after having sold 3% at 400 less than 2 years earlier to release pledged shares.

Neither is the purpose of the 1750 crore fund raise revealed. Will know only by EGM on 22nd January 2026.

Market feedback is that Granules promoters have sold substantial personal real estate holdings at Hyderabad and Vizag in the recent past.

My guess is that it is for building a Peptides unit in the name of their subsidiary, Ascelis using recently bought Swiss subsidiary Senn Chemical’s technology for Biologicals perhaps catering to some CDMO deals.

6 Likes

GI has not explained the Fund raise of 1750 crores, except in vague terms. Apparently many institutional investors didn’t appreciate the preferential offer to the promoters and voted against it.

There was a post in X ( Twitter) their ED Priyanka Chigurupati about looking to buy an injectibkes unit for $50 million, most likely abroad. The post has since disappeared.

Q3 performance and Concall do indicate better days ahead with hefty contribution from US subsidiary and breakeven of loss making Swiss subsidiary, ramp up at GLS, Onco block…

I am not sure why the management is being so secretive. It doesn’t help the investor perception nor the share price.

Agree, they have not explained (not at all) for such a big fund raise. But they are raising money @585, which is 52 high price and also getting on-board a PE Fund (360 Wam).

PE funds expects 20-25% CAGR for the next 3-5 years so looks good for investors returns perspective.

Having said that explaining the funds is a basis necessity and investors participating in the con-call also did not press management hard enough to answer question about it.

Let us see how the market sees it but the price has a strong anchor @585.

1 Like

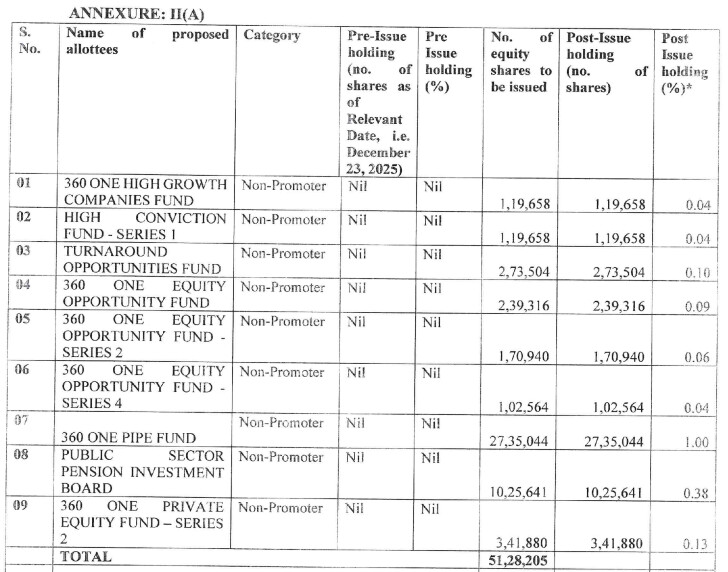

The resolutions approved by the shareholders on January 22, 2026 authorizes the Company for:

- Issuance of up to 2,50,00,000 (two crores fifty lakhs) warrants convertible into equity shares of the Company on preferential basis.

- Issuance of up to 51,28,205 (fifty one lakhs twenty eight thousand two hundred and five only) equity shares of the Company on preferential basis.

One side : Diluting the shares ,Not EPS accretive.

other side : Preferential issuance is Value buy.

Suggestions plz.

After a long time, Granules does seem to be at an interesting crossroad. Some of the Growth Triggers that come to mind:

1. A Product Mix Shift is happening

- Complex Generics is picking up pace and now has become 49% of the total portfolio contribution and only growing.

- These Complex Generics are into interesting therapies, where barrier to entry is very high and there are massive tailwinds. Few of the therapies Granules’ complex generics are present in are: ADHD, CNS, Controlled Substances. Granules also claims there is a demand > supply issue in ADHD, and they have lately commercialized Granules Lisdexamfetamine[1]

- The pipeline is also looking robust with tentative approval for Adzenys[2] (Generic Amphetamine)

- Management claims that they are expecting an incremental $40-$50 million in annual revenue from these high-entry barrier launches in the US business by FY27

- API Prices

- The worst of the API price erosion is over

- This can prevent anymore downside in the legacy business, with your RM prices stabilizing while your growth driver will remain the CG business

- The Peptide Business

- The Peptide CDMO business which is the Siolys/ Senn Chemicals → posted an EBITDA loss of ~Rs 24.8 Cr in Q3.

- Management has guided that Q3 FY26 had high maintenance costs, but Q4 FY26 is expected to reach EBITDA neutrality

- In Q4, there is a possibility this can segment can breakeven, and then from Q1/Q2FY27, the bottomline starts picking up

- Balance Sheet

- Net Debt at ~1015Cr

- Granules recently did a fund raise[3] where the promoter group and non-promoter group infused capital (Rs.1462 cr warrants + Rs. 300 cr pref issue) at Rs. 585 share.

- This will help with debt repayment and capex, which will flow directly to the bottomline

- The Gagillapur Facility

- The Gagillapur Facility was operating under constraints due to FDA remediation and is in the final stages of normalizing[4]

- As most of the fixed costs have been absorbed, as utilization picks up operating leverage can hit (with margins improving)

Disc: Biased. Just seeing positive shoots in a business I have been tracking since a very long time.

4 Likes