Looks like worst seems to be over. Last quarters they said that they will pass on price hikes to their client starting Q1, which seems to have aided margin.

Current reduction is oil prices shall help them slightly in term of RM cost, but not much.

There are number of reports stating that supply chain issues (container shortage) are easing along with reduction is prices. This may help them in coming quarters.

China’s big player have started PAP production last quarters and hopefully they shall get supply from them from Q2/Q3. Additionally Sadhana Nitro also started producing PAP domestically. Once they stabilises their plants and get approval to supply to Granules, this should ease of pressure on Paracetamol API Considerably in coming quarters.

So, H2 profitability shall be considerably higher than H1 profitability as they pass on more prices and supply chain issues are eased.

KSM & Freight rate stablising now. Sailing time to USA has doubled leading to higher inventory levels across the value chain.

PAP situation improved with the largest company in China coming back on stream in July and two domestic companies starting production in India. Leading to better prices for the company

Paracetamol capacity running at almost full capacity

DCDA (ksm for metformin) got PLI approval with a capacity of 8000 tonnes pa. Estimated investment 100crs, company expects a cost savings of 10crs along with supply security for the company. Company expects the capacity to become operational in 2 years time. To be used for captive consumption. Once the capacity is absorbed company will double the capacity and strat offering PFI and API to other companies

CMO services to start from oncology block

Setting up a fermentation lab with an investment of 75crs (20crs already deployed). Biotech acquisition was to bolster this capability.

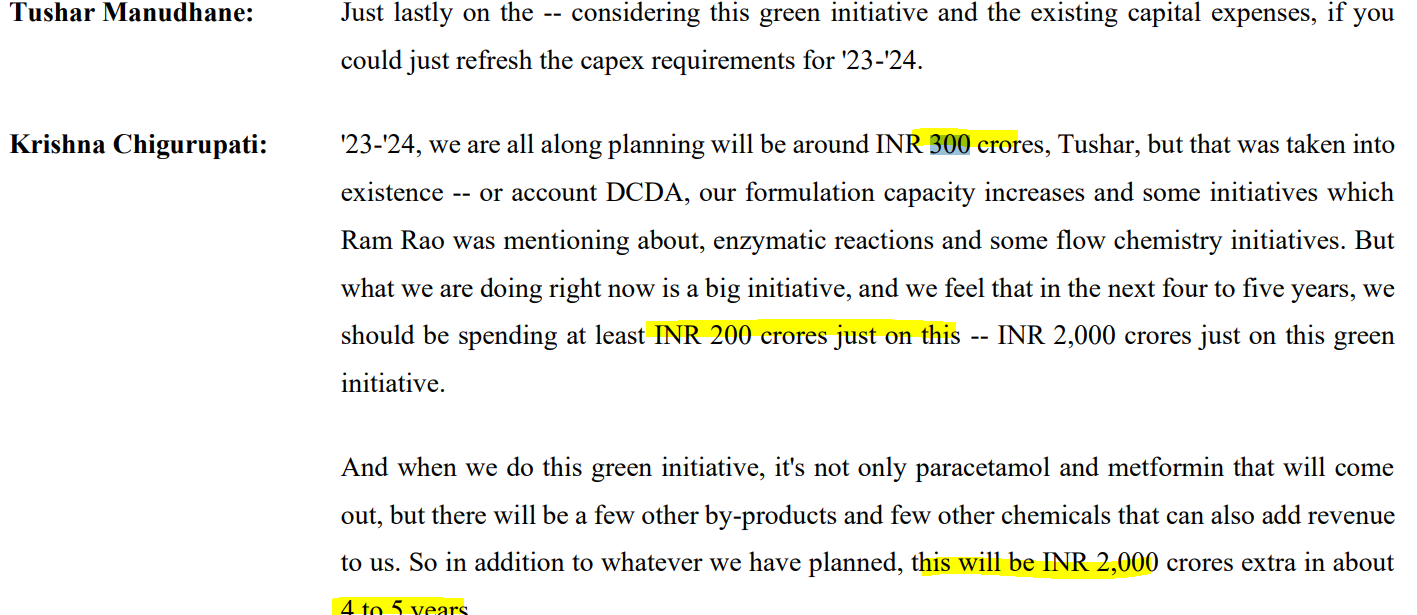

Total capex for FY2023 & FY2024 will be 600cr. FY’22 capex was 400crs

MUPS block commercialisation has started with couple of products and various other products are at different stages of approval.

Paracetamol prices will go down in the future commensurate with the fall in PAP prices. Margins will be maintained.

EBITDA to improve Q-o-Q on the back of volume growth.

Non core compounds have grown from 17% last year to 18% of total sales. Company will start to look at cost optimisation.

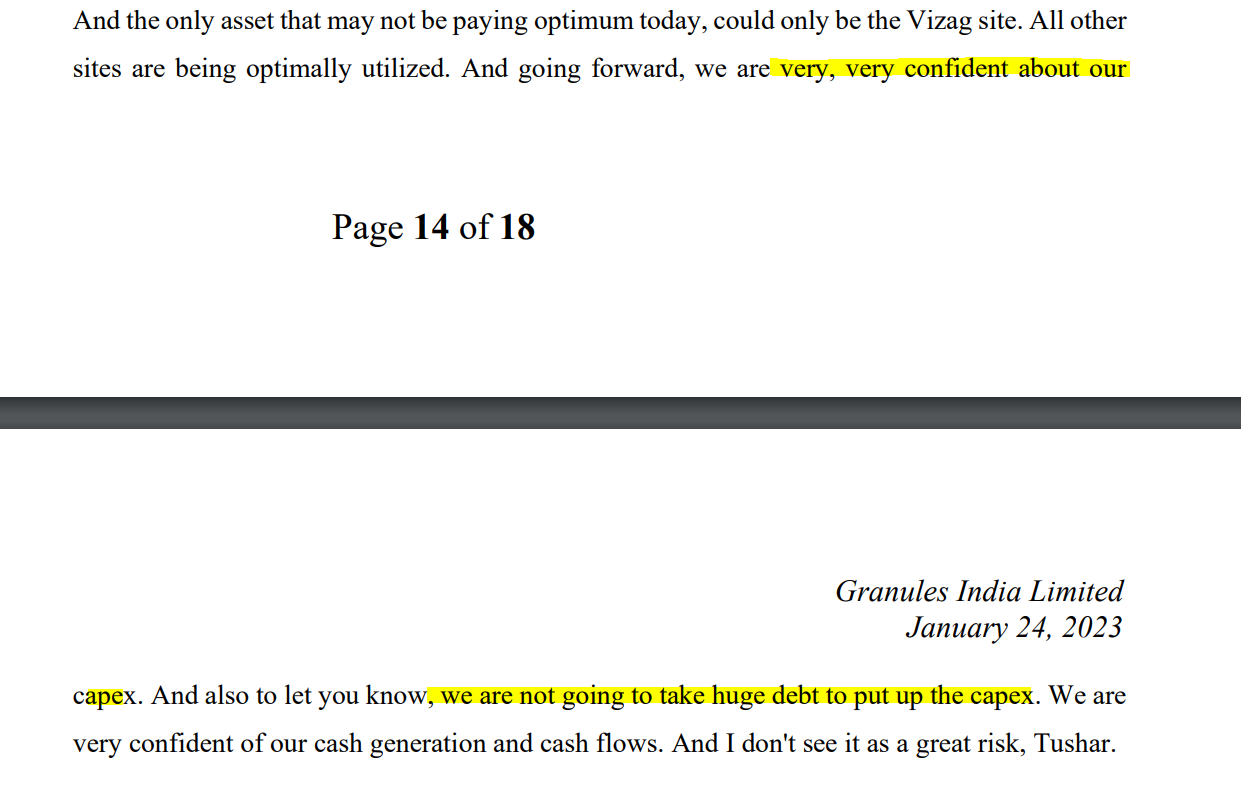

Long term debt is expected to be zero in 2-3years time. Total debt will fall this year even after the buyback. Expect positive build up of cash every quarter.

OCF of 180crs vs 75crs in Q1. FCF at 98crs (expect cash flows to improve further).

Concall Notes from Aug 10 2022

Things look positive from here. The management wants to focus on FCF generation.

Key Raw material PAP prices have started to come down. Availability has improved. Company would also source from Indian Suppliers apart from China based on who provides better rate and stable supply.

There was a rise in Working capital in the past because of the Supply disruptions and company had to stock more inventory. This should normalize and company is focusing on FCF generation

250 Crores allocated for Share buyback and promoters also would participate in buyback

Capex plan for FY23 is 300 Crores. 100 crores for DCDA plant. 75 crores for acq of Biotransformation plant and lab. This will help in Enzyme led projects

Current debt at 613. Long term Debt is 300 crores. Earlier it was prudent to save the money rather than repaying debt because of better reates at that time. Now since the interest rate is increasing, company wants to reduce it. There will be no long term debt in 2 - 3 years.

Company got approval for PLI scheme in DCDA manufacturing at 8000 tonnes per month. This will help in Backward integration for Metmorfin. Primary purpose if for internal consumption which will reduce the cost than importing from China

Cash to Cash cycle had a hit because of larger inventory owing to supply disruption and aiming to bring it normal

Margin improvements - won’t be able to hit 30% but will be able to maintain with lag in passing of Price increase and decrease.

Focus areas - Biotransformation and Enzymes

Focus Geos - Europe, South Africa and LATAM for next 3 years, Launching paracetamol in Europe

That’s not encouraging sign. If promoters have confidence they will stay away from buyback and as a result that will increase their holding percentage.

It is not necessary that promoter participation in buyback is a negative sign. Granules’ promoters have a pledge on ~4.45% shares as of June 2022 (source: ValueResearch). If the money from buyback is used to release the pledge then it bodes well for the stability of the promoter’s holdings.

More than the promoter participation, I find Granules’ buyback a bit difficult to understand given that they have 1000 crores debt on their books.

Not sure why debt reduction hasn’t been given a priority if Granules has free cash, especially in the current environment of rising interest rates.

Though I agree that, Debt reduction comes first that Share buyback , they are also cognizant about debt reduction.

They discussed this in the call " * Current debt at 613. Long term Debt is 300 crores. Earlier it was prudent to save the money rather than repaying debt because of better reates at that time. Now since the interest rate is increasing, company wants to reduce it. There will be no long term debt in 2 - 3 years."

They have been trying to maintain D/E ratio at 0.3

Per this news there is a shortage of Adderall in US. Adderall and recently Granules got the ANDA approval for this in Dec 2021.

[Granules Pharmaceuticals, Inc. Receives ANDA Approval for Amphetamine Mixed Salts (IR Tablets)](https://Granules Pharmaceuticals, Inc. Receives ANDA Approval for Amphetamine Mixed Salts (IR Tablets))

This might give a short term boost to revenues. Someone should ask mgmt about this in the upcoming concall on 20th.

Fright costs have not reduced considerably in Q2 but will impact positively in Q3 onwards.

Science/Tech initiate will increase R&D- It will be 40 to 45 cr in each quarter from now on

Capex spend 94 cr.

Paracetamol margins are less.

Due to the good availability of raw materials, Para sells more. Demand was not the problem for Para.

Successfully converting a lot of API customers to FD.

Gross margin 2/3 years

- 21 and 22 are an aberration.

- EBITA slowly creep up YOY. The target is 25%

- Going for high-margin business, and we will see higher-margin business. Rely on Granules 2.0 up and running.

Container rates $14,000 to $ 12k $8.5k. Pre covid container rates- $4500

-Fright cost will offset the increase in R&D in coming quarters.

Top 5 customer concentration - around 30-40. The top 20 are not more than 60%.

10 % of imports are from the US.

The whole world depends on China for Metformin Intermediary .

PAP- Buy from India/China.

H2 will focus on Working capital, inventory, receivables and payables management.

High Potency API

- FOCUS ON Oncol formulation.

Enzymes/Fermentation - The pilot looks good; we will launch is soon.

Bio-Tech investment is 13 cr so far.

See commercials for the product in the next couple of years.

In Biologic, we will be an investment.

Capex could be higher after next year onwards (FY 25 onwards)

Europe

European product launch will happen in Q3 through our partners.

European Para launch is happening in Q3. They will be launching our own brands/FD in two countries.

Next quarter, Metformin will launch in Q4. (OK growth)

MUPS

Some of the more important ones are yet to be approved. It may be in Q4/Q1.

Going a little slow.

Number of MUPS launches - 2 in Q4- increasing market share and one more in Q1 next year.

US

Continue to see double digits price erosion. This is offset by launching more products and more in other markets.

3 already launched, and 2 more to go in US.

Decent market share in Metformin. Would not like to increase market share at cost.

There is shortage of Paracetamol and Ibuprofean due to sudden changes in China’s Zero covid policy. People in neighbouring countries like Singapore/Australia is sending these medicine to their relative in mainland China as per the NYTimes report.

Additionally,France is also reporting shortage of paracetamol. Granules does not sell their products in China/France directly, but they are planning to sell Paracetamol in Q3/Q4 in Europe. As winter session in Europe/US is middle, it will take few months to normalise situation.

Based on this, it seems that paracetamol/Ibuprofean prices will remain high, boosting Granules sales/Profit. I wont be surprise if they post highest ever quarterly profit in Q4(Sept 20- PAT 164cr).

PAT was impacted due to missing revenue as well as penalties due to a lack of timely deliveries

A couple of million dollars (FD sales) missed sales. A substantial portion would have flown to EBITA.

Once supply sort out margin will improve.

Expect to see the validation of enzyme-based API by Q3 next year (Dec 23)

R&D - 23 cr. Going forward, 32-35 cr. Reduction is due to less filing. From next year onward, we will focus on high-value R&D

Net cash reduction in the case due to buyback of 310 cr. Hence net debt increased in Q3.

Paracetamol business is growing, and we shall grow double digits. We are canonicalizing other suppliers (e.g. taking market share from others)

Supply security is driving sales for Para for big pharma companies.

The Q4 interest cost will be slightly higher.

Cost of funds- 5%

MUPS block is going to be commercialized in the next few months. That is going to make a large difference in the utilization of fixed blocks.

CRAMS

Until green makes a difference, we may not be able to offer this in a meaningful way.

Capex

300 cr Capex-

MUPS (280-290cr). This shall have 2.5 to 2.9 asset turn very shortly

-Vizag site not being optimally used. All other fixed blocks are utilised.

Future Capex funded through internal accrual.

US

Deferred sale due to 3PLS- couple of millions of sales in Q3- Not sure how much will come in Q4.

Price erosion- YTD - 12-15 % price erosion on a blended basis A couple of quarters look challenging. But price erosion may be lower than it is now.

Some of Para API will be converted to FD going forward.

As more FDA approval was coming in, companies were fighting for a market share of the existing product hence price erosion. However, FDA has started inspecting, and companies will not fight as much as they will focus on launching new products. Hence price erosion shall be less going forward

Greenko

Starting Para/Metformin

90% of raw material in the house at one location.

Proposed to setup additional capacities to setup capacities to cater to 50% of global capacities for Para/metformin.

They will supply us with chemicals.

Economic scale is a big advantage. All in one place.

Cost of chemicals supplied by Greenko shall be same as grey scale chemicals

Capex- They are going to incur major CAPEX. Capex is for ten year.

Electrolyzer technology is making rapid progress so we shall see some benefit

On top of the existing 300 cr/per annum Capex, Granules will be doing an additional 400 cr/year Capex on average over the next five year. The additional Capex is mainly for Green ventures.

They are making a long-term contract with Greenko to purchase raw materials such as Ammonia and eventually produce an intermediary and then API for paracetamol and metformin.

Although they are working on the right things, it is fraught with huge risks. I doubt if anyone has produced paracetamol/metformin API following green chemistry. Today there is a lot of hype around the hydrogen ecosystem, so time will tell how it unfolds or how it takes off.

Going forward, Granules has to invest significantly in terms of money as well as research efforts. As per management, they are spending around 30-40 cr/per quarter on R&D, but most of it is towards filing US ANDA. Additionally, this R&D amount has remained in the 120-140 cr/per year level for the last 4/5 years (despite management claim that they are double down on R&D). So they have to up their investment significantly in R&D and are still fraught with risk.