FY 21 PAT will be double of FY 20 and FY22 onwards 30% with base of FY21

PAT growth of 80% in FY21, 30% CAGR over it for next few years (earlier 25-30%).

Change in Product mix and operational efficiencies helped margins in Q2

400cr capex in current year & next year

Company spent 9.9 Cr in Q2 for covid related safety expenses on employees

ROCE increased due to better utilization of plants. PAT growth is higher than revenue growth: Due to good product mix, price realization - New launches, new approvals and price realization resulted in good growth and will continue in the upcoming period

Vizag facility expected to come up next year

Willingly delayed launch of 6-7 products due to COVID

3-5 new launches in H2

FCF before working capital is 281 cr

Working Capital debt increased by 31 crores

60 Cr of CAPEX in this quarter

Increase in inventory due to extra stock in US. We need to build up inventory of 3-5 months with every new product launch, else if we can’t fulfil demand, we may face penalty

Raw Material:

KSM is still imported from China, but no challenge in availability / prices stability

Also partnering with small players, by delivering them technology and accessing the basic chemical

Core molecule contribution in Revenue reduced to 70% and plan to bring it down to 50%.

Gross Margins: Combination of product mix and price realization. EBIDTA and PAT margins is expected to be maintained

Supply credit working capital will continue to go up and some of it is financed by payables. It will be managed by combination of internal accrual, increased receivable days due to shift in process of selling product in US (which has better margin but longer payment terms)

ROCE will be maintained despite capex from internal accrual

Oncology APIs are launched but the impact on top line and bottom line will take some time.

No COVID related demand in the core products except paracetamol (which contributes 16-18% in PAT) - no plan to increase paracetamol capacity as better opportunities are available

One big product launched . Increase in new customer was the key benefit - hence this margins improvement will be from the new product.

Future revenue share will be from new product rather than core molecule

Majority of growth is from US market but to reduce dependency on US, focus will also be on rest of the world. Europe will be a key market.

US will grow in absolute numbers, however the expansion of growth in Europe market is what company eyeing for.

Company will work with partners so that company will not have to be at front end, company will not have to hold the inventory. This will improve the working capital

Launching formulation in Latin America, and the margins in Latin is better than other area.

Though the company sells API, most of it is used for internal accrual. Company also buys some of it from China.

As Company ran out of capacity it has built up the capacity that will last till the end of next year. By that time new plants will be ready.

New PFIs coming up that will be launched in Latin America and rest of the world.

MUPS technology: Most of the company is using this technology. Expansion will continued in the coming quarters and pellets are produced for gastro purpose

1 MUPS ANDA approval expected in Q3 or early Q4 - launch product in Q4

Subsidies will be given on the mix API, however this would be on green field, and it would be difficult for companies too open green field to avail the subsidy as it could be small part only

Conclusion:

Company is focusing to foray its market in different geographies.

PAT and EBIT margins are expected to be on line (key focus here).

Pipeline is expanding and new products will be key driver of growth in future. CAPEX will include majorly new product only.

Note : Please consume it as per your own risk appetite. I may have overheard certain part or there could be typo errors as well

Thank you @mrai74 and @mparadkar FY 21 PAT will be double of FY 20 and FY22 onwards 30% with base of FY21

They’ve basically laid out the expected price and upcoming bull run for the next few years for us. If they do the above(and they usually underpromise) this is definitely on board for a huge EPS expansion and re rating. Also, worries regarding china were addressed appropriately and capex for new product is very welcome and decreases dependency on their core products and adds more growth drivers.

Disc: invested about 8.5 percent of my portfolio. Will add another 4 to 5 percent if there is a dip next few days

Granules earning increasing due to its foray into ANDA like a mainstream pharma co. What PE would one assign ?

Still lot of juice left.Tailwinds quite strong for pharma sector

-Due to less price erosion in US & other regulated mkt,

-Indian pharma cos learning from the mistakes & are more quality conscious & shud clear FDA audits in a better manner,

-India supplying 40% of world demand of worlds formulation as each batch of medicine gets expired necessitating manual supervision helping Indian pharma cos tks to low cost manpower & enabling ecosystem ,

-Pharma after under performing for last 5 years outperforming only since last 5-6 months having lot of under ownership

Post covid importance of Indian pharma cos reaffirmed in the eye of world

China plus 1 policy too helping a lot due to geo political factors as well

Company is launching new products in US market. To avoid any disruption post the launch given Covid times, company has accumulated some inventory. Should normalise over next 2-3quarters.

Hey @vagator10 There could be plenty of reasons for the stock price being sideways post results.

I have a friend who works for an institution that deals in high volume trades. He has always emphasised how they book some profits on days of good results so they have enough volume of buying due to the good results to counter their volume of selling hence preventing a drastic fall in the stock price and letting them cash out at high prices. It’s one of the reasons you see stock prices rise on bad result days. There’s enough selling volume for them to buy good Companies in large volumes for the mid to long term.

Then there’s the buy on rumors sell on news where the good result is already factored in and hence the price remains stagnant for a bit. There are plenty of other reasons too(one of which could be less volume due to asm) but I’d rather not question why since we have enought info for the medium/long term.

Either way this will just be temporary… never question the day to day with the market since there are too many moving parts. Considering the commentary from the concall there seems to be literally no bad news atm(apart from the sale rumors) so this just looks like an opportunity for us to add more without having to pay extra for new information(including results and commentary for FY 21 and next year!) which is a gift that I don’t want to question too much tbh.

@mrai74 . I’m not sure if you are agreeing with my comment about eps expansion or disagreeing haha. Either way I standby my comment of both eps and re rating expansion. Granules looks set to hit EPS of approx 26 like you mentioned. That would give it a PE of approx 15 at CMP end of FY 21. Market had already given granules a re rating of around 26 post Q1. So just with earnings growth we could see a rise from CMP by 75 percent. For FY 22 they are expecting approx 30 percent increase… so that in itself will lead to a price of around 900 by end of FY 22 with jsut earnings expansion at current PE ratings. If they pull this off over the next 6 quarters there’s a high chance of a re rating above 26 too. Optimistic scenario (il admit there’s an overhang of the rumor of sale to PE investors over the next few quarters and the chance of results not meeting expectations ) but management has given no indication of overpromising past few years so I’m optimistic and bullish too. With capex in new products, increased and sustainable margins and entry into new countries it looks like we have a long runway of growth now so worries about de rating long term doesn’t seem to be an issue anymore

@vagator10 If I’m not mistaken stocks under asm are checked bi monthly by sebi and upon review for volume fluctuations until they are removed. So it can happen at any time without a fixed period as such. During this period margin is fixed at 1x only so gaining volume is a bit tricky and I can’t remember any stocks in asm breaking big resistances or supports. Infact the purpose is to keep them in range and protect investors after sharp rises/falls so what’s going on now is as expected.

Another reason is sectoral rotation btw… pharma is now near support after a big correction. I’d assume as more companies results come in pharma and granules will get more attention. Alembic pharmas results come in today and it’s expected to be a doozy and should give more attention towards pharma which is near support levels in 11300 range atm. Earnings season has led to meaningful rises/resistance breaking last 2 quarters for pharma and can see the same happening now since most pharma companies management sound bullish. Granules hasn’t broken any supports yet and when it does participate in the broad pharma rally its all time resistance is just 6 percent away. If it does break a resistance without the help of margin traders it will have set up a strong support with legitimate big buying( not reliant on margin) and it’s giving us a chance to buy more now so it’s a good thing imo. All that we need is patience

I think ASM is the major reason. Granules has enough reasons for a clear re-rating…tying it up in ASM is not justified. There are many bhangaar stocks that hv a free run and nothing happens to them.

Price has ran up way ahead of the financials so now I feel price movement will take a breather and will allow the earnings to do a catch up. I expect the stock to consolidate in this range till next results. Considering sharp run up in past 6 months, it may not be such a bad thing.

Yes @Marathondreams That’s exactly why stocks go under asm too. Sebi would have noticed this and done the same. A lot of pharma /Chemical companies (aarti, gmm pfaudler etc) have had similar runs of price seperating from earnings. It’s par for the course when a dormant sector wakes up after years of being beaten down. With granules things are a bit different since even after its amazing run it’s still cheap at PE 22 and with management guidance is currently trading at PE 10 to 11 or so for FY 22. So the run can continue for a while. Their earnings will catch up and I’m sure all of us here have long term goals with granules anyway. Btw since sebi does bi monthly reviews there should be one scheduled by end of month. Post these results I’d bet their next review will clear it from the list since the elation is somewhat justified by earnings. That being said if anyone wants to please go ahead and flag and delete my comments. Discussing day to day movements in a company as well set up long term as granules isn’t what should be a priority for this thread. I apologise for the same

Would just like to add that the result for me isn’t the trigger. The commentary is. Last quarter Mr. KP guided for 20 to 25 percent growth and not much visibility post FY 23. Now we have 100 percent growth for FY 21 and 30 percent there on with a new base formed with new products, capex, countries, approvals in place to facilitate the same. That’s the trigger for me.

Note: just to add more value to this post… granules just received US fda approval for potassium chloride tablets for treatment of patients with hypokalemia as per bse filing.

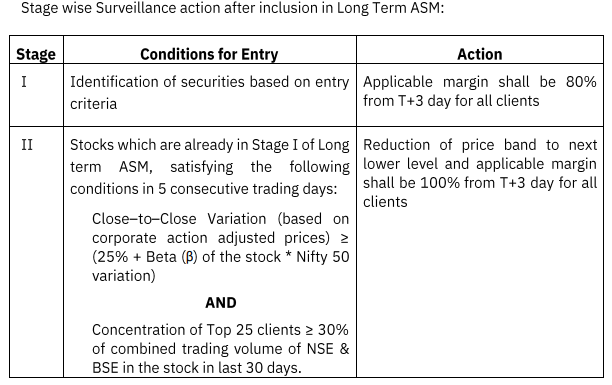

ASM is implemented based on an objective dynamic criteria covering the following parameters:

a) High Low Variation

b) Client Concentration

c) No. of Price Band Hits

d) Close to Close Price Variation

e) PE Ratio

f) Market Capitalisation

Regulators are NOT bound to publish the reason of moving any security under ASM, but certainly they found Granules to be meeting ONE of above criteria.

Granules is currently under STAGE I and surveillance actions applicable for them are following:

They will be moved to Stage II, if regulators are not satisfied with parameters followed during current stage

The shortlisted securities shall be further monitored on a pre-determined objective criteria

and would be moved into Trade for Trade settlement once the criteria gets satisfied. During Stage II, when the security is shifted to trade to trade settlement wherein the settlement shall be on gross basis i.e. delivery based.

Conclusion : Most of the retailers are surprised with Results beyond expectations and more on price movement post result. Tagging each price movement with specific event is toughest (& impossible for me) job. I understand that learned people are following limited approach to ensure that Granules doesn’t move to ASM Stage II or further… it will make their life tough… till we move out of ASM, its good to consolidate, gather more positives (We had first MUPS approval today & expect commercialization and launch later in current FY itself), which will certainly make the fundamentals more stronger for next upmove

EPS expansion is directly related to management guidelines for upcoming future and doesn’t change based on mine or yours agreement or disagreement.

Regarding PE rerating, I don’t see it reflecting in various research reports published by brokerage post Q2 result. Seems we have to wait longer for that.

If we consider EPS expansion, PE rerating and entry of Private Equity firms keeping current management responsible for execution… we are set for a good future