Seeing results fundamentally very strong company with reduced DE ratio. Only concern is why DII holdings is almost ZERO

2 Likes

Any idea about the present level of promoter pledge in granules ? Has it been fully liquidated ?

Mr Krishna Prasad has still pledged 90 lac shares which is 8.64% of total promoter group holding.

2 Likes

4 Likes

ASM is clearly stragulating the stock. Hope this is resolved.

1 Like

Finished dosages

2 Likes

2 Likes

-

When does Granules come out of ASM stranglehold.

-

I assume it is consolidating right now and would take out 500 ceiling right before next quarter results.

-

More visibilty on PE deal, should come by now as it is already one month.

2 Likes

I read on some public forum that the remuneration of directors of a public company (combined) should not exceed 10% of net profit

granules has following figures for H1 of current FY vs last year

H1’19 PAT : 179 Cr

H1’20 PAT : 275 Cr

PAT increased by 53.63%

H1’19 Managerial Remuneration : 21.79 Cr

H1’20 Managerial Remuneration : 43.98 Cr

Managerial Remuneration increased by 102%

Even if it is within specified limits but seems the growth in remuneration is too fast and doesn’t match with PAT growth

5 Likes

Atleast there is tax to be paid in full on salaries & reduces chances of siphoning.

2 Likes

Per the NSE regulations, long term ASM is revised after 60 calender days. When was granules moved into ASM long term category I?

2 Likes

Around 14Oct, put under ASM

Granules India Q2 concall highlights -

- Highest and best numbers in the company’s history. A validation for company’s differentiated business model ( greater backward integration and manufacturing excellence ).

- Today Granules is a 22 product company, up from 5 products a few years ago. Company believes in having fewer number of products but achieve excellecnce and cost competitiveness in them, through backward integration into APIs. ( this is what I like the most about the company ).

- Company guiding for PAT growth for FY 21 at 80 pc . Next yr onwards, they are guiding for a PAT growth of 25-30 pc with FY 21 as base year.

- MUPS technology ( used for extended release tablets ) based ANDA with in house APIs - next growth driver, approvals and launches expected in Q3 and Q4.

- Q2 sales - 858 cr vs 700 cr YoY, Gross Margins at 58 pc vs 49 pc YoY due greater share of FDFs, EBITDA margins at 30 pc vs 20 pc, PAT at 164 cr vs 96 cr YoY. Company confident of maintaining atleast 27 pc EBITDA margins going fwd with an aim to keep clocking 30 pc.

Covid related expenses - 9.9 cr in Q2. Total in FY 21 - 19.3 cr.

- Company is encouraging a few speciality chemical manufacturers to manufacure some key KSMs like - Para Amino Phenol ( for PCM ) and others with assured contracts ( to reduce China dependence ). Since, these are Spl Chems and not APIs ( plus capital intensive ), company does not intend to make them in house.

- Contribution from core molecules at 70 pc, to go down to 50 pc over medium term. Core molecules - Ibuprofen , Metformin, Paracetamol, Methocarbomol, Guaifenesin. New molecules where the company is ramping up include - Losartan, Cetrizine, Fexofenadine. CAPEX for this yr likely around 400 cr. ( around 80 cr for APIs , rest for MUPS block and FDFs ). Better estimate for further CAPEX by next yr. CAPEX not going to stop. However the company is concious of its ROCE profile and would maintain it above a particular threshold desipte the Capex.

- Current revenues from Europe ( FY 20 ) at 500 cr. Expected to go upto 1400-1500 cr by FY 23. Europe expected to be a major growth driver going fwd. Company agressively working towards reducing dependence on US and increasing the contibution form ROW, LATAM and Europe. US revenue share likely to be around 40-45 pc by FY 23 ( present share at 53 pc ).

Disc : invested.

7 Likes

Board approval to set up new plant for Formulations.

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=4ea6f361-a9be-49b2-a7d9-282c9c1414a9

2 Likes

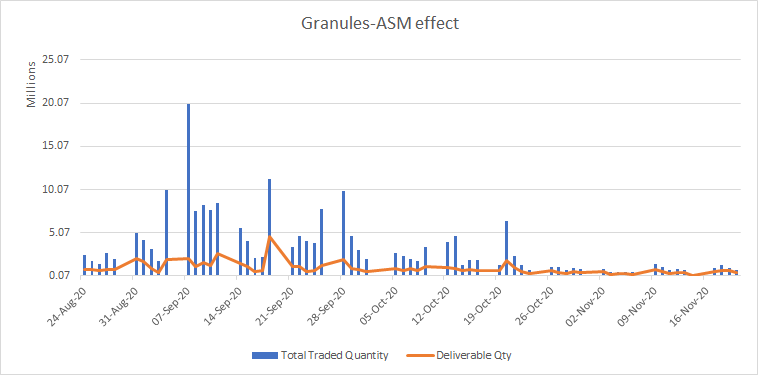

Mid October, Granules went into ASM stage-1, which increases the margin limit having direct impact on volumes. Following graph of volumes on NSE tells us the story

Nest review is due mid-December and we need to watch next action of regulators

5 Likes

Does today’s volume have an impact on ASM rating in December?

Please refer Granules India Ltd for conditions which can lead to continuation of ASM or moving to next stage with more stricter surveillance by regulators.

hardly one percent of total shares changed hands, i do not think that is big enough to have any impact

1 Like

I understand that the ASM review is based on average volume for the period under review. Last 2 days have heavy volumes.