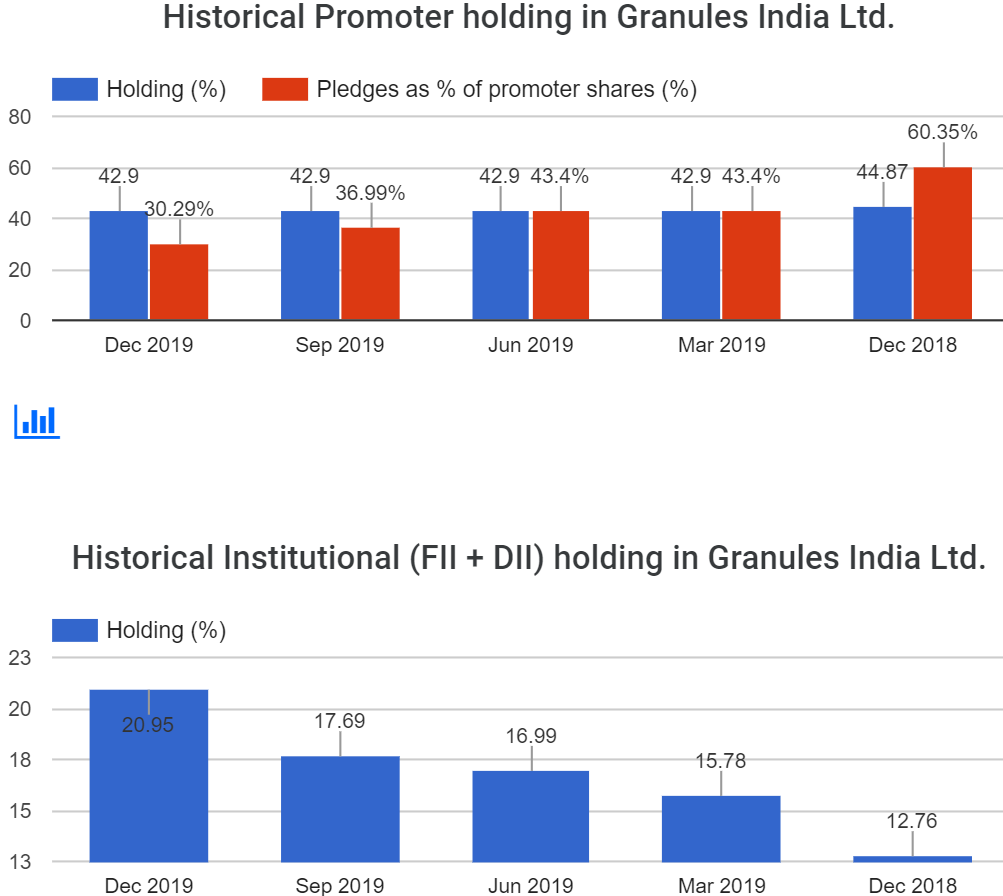

Pledge of a small quantity is not a good sign, it shows financial stress

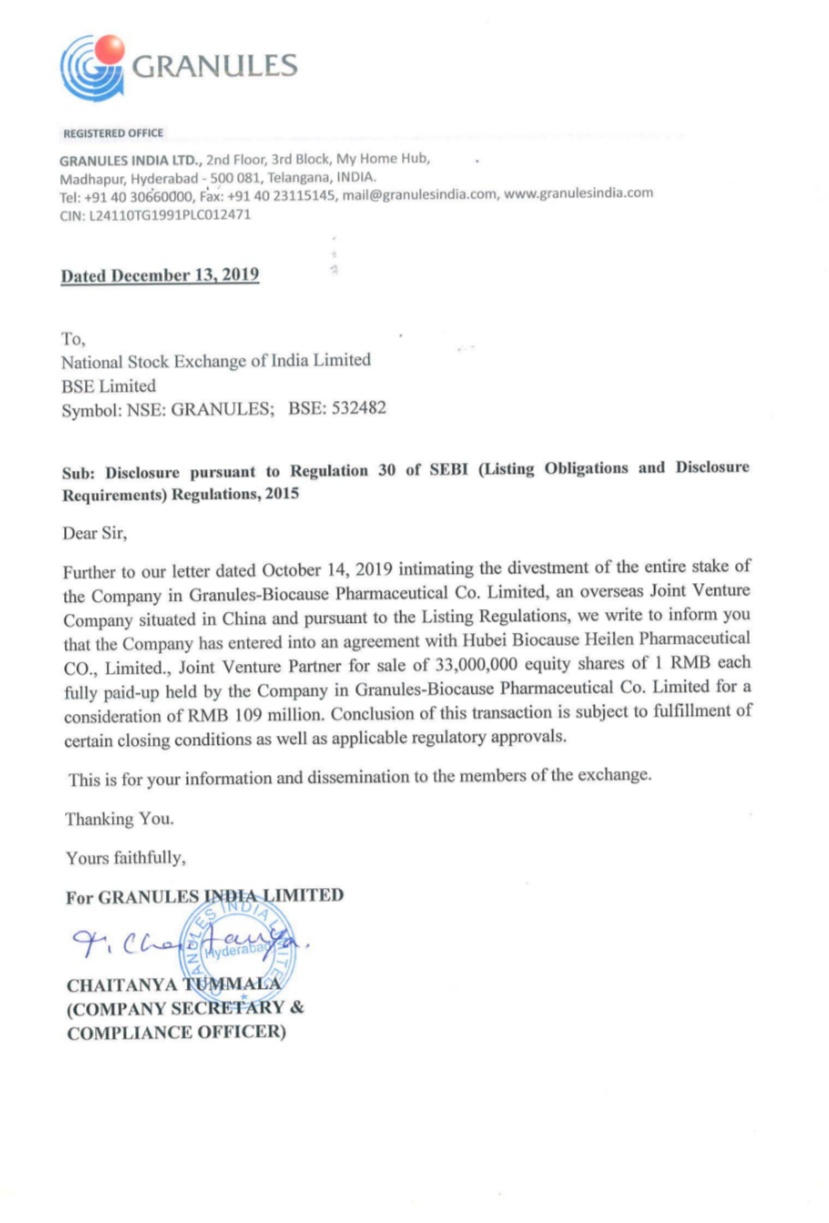

Granules India to sell stake in China JV to Hubei Biocause for ¥109 m

Interesting time ahead

Seems to be Rerating Candidate

Disc:- Invested

1 Like

Good interview on Bloomberg quaint. Most of the things the said was already in the public domain and con call.

On R&D capitalising

- Last year Granules expense out 50%.

- This year they expense out 65%.

- From FY 21- they will be expensing out everything- no capitalising.

3 Likes

Key points from the interview

- Expecting more approvals from FDA

- New products in US have market of 400 mn & Granules target 15-20% (they are pushing old guys in the field & few are expected to move out … if it happens Granules share can go upto 50-60%)

- Expected cash of 220 CR from JV sales

- Exploring Europe as well

2 Likes

The company deserves to trade substantially higher from the current levels.

Don’t know when this’ll happen. Granules has been a wealth destroyer from 2014 to date so now’s the time to claw back.

If they can keep walking the talk and do an EPS of 20 by fy21 with impressive roe, nothing like it.

Management doing all the right things

Reducing Debt and Pledge

Prudent Allocation of Capital

I’m expecting EPS of around 15-16 for FY20, FY21 EPS Maybe 20+

At CMP 130 it’s still trading at much attractive Valuations.

2 Likes

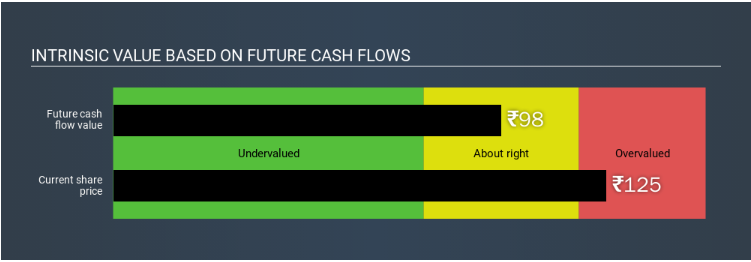

Using a two-stage DCF model, which, as the name states, takes into account two stages of growth. The first stage is generally a higher growth period which levels off heading towards the terminal value, captured in the second ‘steady growth’ period.

The detailed analysis still comes up with intrinsic value of 98/- based on future cash flows

Output is based on the inputs used to compute DCF.

2 Likes

He moves out of board. Good message from promoters.

Bayer has similar product & it clocks approx 64 Cr USD per annum. The opportunity is huge. Had anyone seen management commentary around internal targets / expected hit in topline

As best of my information, Management yet not given any guidance for Volume, but heard they guided to start Production & Marketing in next two Qtrs.

Things are moving in right direction.

Disc : Invested

Good to see promoters coming up quickly with clarification on news items which are misleading as always. The clarification reads following

Ranitidine is being recalled by various producers from the US market as they contain

unacceptable levels of N — nitrosodimethylamine (NDMA). Granules India Limited is

recalling this product voluntarily. The voluntary ongoing recall is a class II recall.

The quantities being referred in various news websites at this point of time is the last one year sale from Granules India Limited to Granules USA, Subsidiary of the Company. The

Company is in the process of recall from the channel partners and the exact quantities are being estimated. The Company believes that this will not have any material impact on its

financials.

2 Likes

If I recall, it was mentioned by Granules earlier that they have no NDMA in their Ranitidine. Wonder how this has no impact? Likely this was just an intra-company matter, and they will now sell this stock elsewhere and so recover the money. Stock remains happy.

1 Like

Is it right to sell defective drugs in alternative markets with lower compliance standards?

I wouldn’t support such a move in the name of retaining profitability. Better to recognize losses and move on.

3 Likes

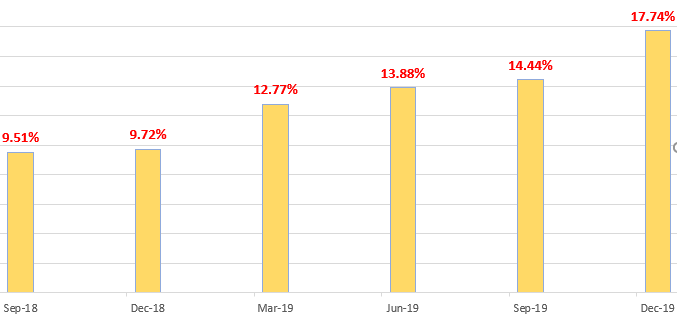

Interesting changes in SHP

-

FIIs increased holding

-

Retailers (approx 6000) decreased

5 Likes

Great Announcement

GRANULES INDIA: BOARD MEETING ON JAN 21 TO CONSIDER SHARE BUYBACK

1 Like

Granules has got more than 200 cr from divesting stakes in the subsidiaries and they are not going to reduce debt. They are bound to something and here they go…

If you are rational capital allocator, why would anyone wants to buyback shares when the stock price is touching all time? On top of that, they have to pay new buyback tax imposed by the FM in last budget.

I won’t be surprised if the promoters set a high buyback price and then offload some of the shares to book profit, and reduce their pledge.