They have spent 84 Crs in first half, they are adding capacity in existing plants rather than Green Field.

This new capacity will be fully utilised by 4-6 Qtrs.,

It’s in transcript page 13-14

Thanks Amit for pointing to transcript, which provides more clarity.

My understanding is that the CAPEX in India (GIL) is only maintenance & most of the allocated 150 Cr CAPEX planned for current FY is for USA (GPI). Following details from earlier concalls may help in understanding it better way.

Indian facilities remain under utilized & management expects to achieve 100% utilization in next 6-8 quarters.

2 Likes

Any idea or access to VCCircle to tell what they are telling?

1 Like

What’s going on here? After exiting two joint venture, promoter now wants to sell their controlling stakes.

As per article at a valuation of 4000 cr which is 23% premium to current market price.

Are they not selling at cheap valuation?

What would be the effect of an acquisition by PE funds on Granules’ future ? Would it upgrade the company to a higher level ? Obviously additional funds for investments would be no problem but what about the quality, of new management. Are these funds strong in management ?

Not having succession in place seems to be reason quoted.

Was waiting in sidelines to enter but not sure now should wait post this development.

Priyanka Chigurupati (Daughter of Krishna Prasad Chigurupati?) is an executive director of GPI. She actively participating in con calls. So there is nothing like no succession plan. May be KP is looking to sell some stake which he got by warrants few years back in order to reduce the pledge shares.(speculation). In last call he said, complete money raised by pledge were used for warrants so now he don’t have much options but to sell his stake to reduce pledge.

Disclosure: holding since few years.

1 Like

Private equity firms Blackstone Group, KKR & Co, Apax Partners, Advent International and Bain Capital are reported to have initiated initial talks to acquire Granules India. Advent has acquired Bharat Serums recently in pharma space. The Chigurupati family holds 42.9 per cent stake in Granules, which is one of the largest contract research & manufacturing companies in the country. The founders are reported to be keen on a control premium, valuing the company at Rs 4,000 crore. Geojit Financial Services and few others have also published enterprise value around similar levels. It will be interesting to see the premium demanded / acquired by promoters on enterprise value. Kotak Mahindra Capital is reported to be managing the sale process.

The transaction indicates the rising interest of PE funds to undertake control deals in India to ensure that they can drive decisions, strategy and corporate governance in their portfolio companies. At the same time, Indian promoters have also become more willing to cede control to a financial partner to boost growth. The reason of exit is reported as succession plan, although we have Harsha & Priyanka actively working for more than a decade with company. in certain cases, second generation of the families are not too keen to run the business and have been wanting to exit it altogether.

Historically entry of PE firms has generated greater value for share holders.

Company had reported to have series of discussions with various investors in last few weeks, but none of the names reported by The Economic Times match with BSE filings. Till now promoters or company has neither commented nor denied this information, which suggests that something is brewing (just my guess).

Even if this turns out to be false, I guess that promoters are planning something to come out of pledge. They have already confirmed that they wish to reduce pledge. Regarding debt they are at comfortable level (1.5xEBITDA) and we haven’t heard any further plan to get rid of that.

Interesting scenario when Granules is hitting 52 week high & is approx 20-25% away from all time high

3 Likes

The stock appears very cheap based on the earnings and management guidance. If the first family is pegging the EV at just 4K cr, it means that either there is no future growth or the news may be speculative. EV of 4K crores means that the current market price is the cap and upside is limited.

I attended the AGM and didn’t find anything great in Harsha. Priyanka didn’t attend.

If the news is fairly true for argument sake, how can PE funds run the company? merely installing an executive CEO to dance to their analysts’ tunes is a sureshot recipe for disaster. Obviously a specialized management is warranted with enough skin in the game.

Pretty concerning news especially at a time when the management had begun to put its act together and things seemed to take off.

My confusion (if the news is true) is simply on the 4K Cr valuation by management vs. the current market EV.

1 Like

Markets / investor behaviour and pricing patterns are very much interesting subject to study.

Price goes down (remain beaten down due to pledge) & when promoters get it released (read details) , it again gets a beating. Hopefully we recover back &these actions get reflected in prices as well.

Another interesting set of report is shared by company, where they have shared Financial Goals for next 2-3 year as following :

Revenue CAGR ~20%

Steady-state EBITDA of 21+%

PAT CAGR ~25%

ROCE of 20%+

and we know that promoters have good habit of walking the talk. Current promoter pledge is 30.25% and they have committed to make pledge zero by FY21.

Am I missing something (I am aware of EIR for GPI in last week & consider that as positive as well)

3 Likes

I must say the latest report (link in the above post of @mrai74 ) is one of the best Granules has produced in the last 2/3 years at least. It has summarised in a few pages, what the company is, what are they doing, and segment-wise profitability. Agree, they have provided these details in various forms, but the current presentation is very detailed with lots of important information for making an investment case.

If we go by what promoters are saying (I have no reason to suspect), the profitability is set to double in the next three years. From 225 cr PAT (2019) tp 450 cr(FY22) and the additional contribution from high margin FD (which is set to grow to 73% from 47% in FY 19).

There are visible signs in term of higher profitability that investments are paying off. Moreover, the Granules is focusing on FCF, which was not there focus earlier.

So from an investor point of view, they are doing what one expects a good company should be doing. And the market will reward the company will better multiple/pricing, sooner or later. So it is just a matter of time before Granules will revert back to it’s historical PE of around 15 (my guesstimate based on screener). No one knew when it would happen, but if the company keep doing what it is doing, then higher prices will be achieved sooner rather than later.

As per new reports, they are asking 30% of higher prices, but if Granules deliver another two-quarters of solid performance, the price which promoters are seeking (around 170-180) has a high probability of reaching. So in a sense, management is trying to get a premium which the company can potentially achieve in next few quarters.

The things which kept nagging me is the company has made the most significant investment they have made, and it is on the cusp of reaping the rewards.

Keeping this in mind, I am wondering why management is considering exiting the business when the rewards are very near? Is there anything I/we are missing?

2 Likes

Finally management clarifies on rumours of stake sale

I would like to invite views of community members on following

-

Does company have any impact of Karvy issues where Sebi has taken stringent action against them. Please note that Karvy chairman is an independent director of the company

-

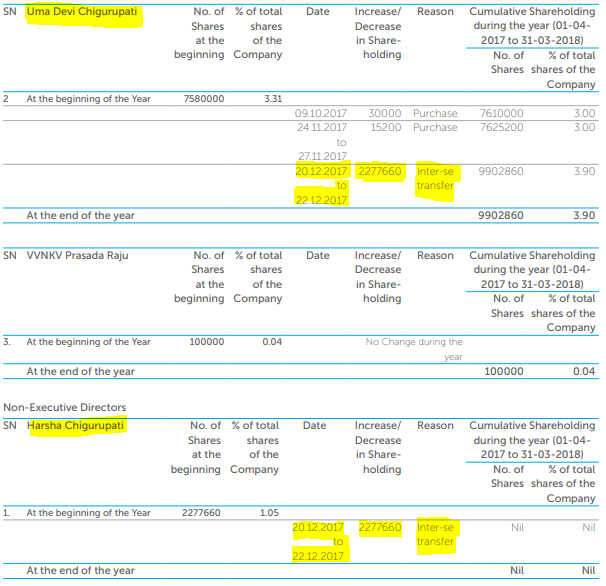

Harsha being Executive Director had 1.31% share holding 2-3 years back but now doesn’t hold even a single share. Infact his holding was transferred to his Mother (earlier he sold off approx 0.25% in previous year). Any specific reason behind this (I see that Priyanka & Pragnya hold atleast some part. Although Priyanka is active but Pragnya is not visible in routine operations)

despite management denial… analysts don’t want to leave it… There is no smoke without fire ![]()

https://generics.pharmaintelligence.informa.com/GB149415/Granules-May-Be-Next-Private-Equity-Target

Karvy replaced. Parthasarathy pledged 405k shares

Read it online somewhere, can’t find the source now.

Secondly just saw that karvy renamed itself, so the registrar is not changed.

Seems he doesn’t own the shares itself… wondering how can he pledge

The pledge by Karvy (Partha is from Karvy) may be related to recent concerns of Karvy & don’t think it has to do anything with Granules

No worries with karvy name change

This shows 405k shares as “pledge invoked” for Comandur Parthasarathy, just 0.16 % of equity

https://trendlyne.com/equity/insider-trading-sast/all/GRANULES/488/granules-india-ltd/

1 Like

Not sure if indeed the pledge was done by a promoter then there would not be a notification of it on the bourses. But I could be completely wrong. In any case the number looks relatively small ( 4 lacs shares is 5 crores rupees,and the pledged money would be a fraction of it) and not something to be overly concerned about. <As I posted this message, I saw that our friend Vikas has provided a link which clearly mentions the pledge creation. Thanks Vikas!>

The last few months have been full of exciting events for Granules - New facility of Metformin getting nod for the exports to the regulated markets, announcement of sell off of two JV entities, and then this rumour of promoters looking to sell-off. Of course the last one is the most spicy one in the near term. Quoting from BM’s book - 'shikaar hamesha shikaari se mehnga hota hai ( the entity getting sold always gets premium). And so if indeed Granules would be sold off then I would not expect it to go for any lesser than at least 25-30% premium to its current market cap. But then I would like to remind myself that at best it is a rumour which has been even denied by the promoters.

Cheers,

Krishna

3 Likes