Share buybacks have lost lustre after FM proposed 20% tax on buybacks

The 20 per cent tax on share buybacks, introduced in the Union Budget for 2019-20, has altered the way companies reward their shareholders. Companies have repurchased shares worth Rs.16650 Cr on so far in 2019-20, a 56.2 per cent fall as compared to the same period of 2018-19. The bulk of the buybacks done in 2019-20 were announced before the Union Budget in July 2019 when Finance Minister Nirmala Sitharaman had introduced the buyback tax with the intention of removing the tax arbitrage between dividends and buybacks. Buybacks worth less than Rs. 2000 Cr have taken place during the second half of 2019-20. Tax experts blame the change in tax dynamics for the sharp drop in buybacks. Companies are expecting the rollback of the buyback tax in the Union Budget for 2020-21.

Considering above report, this activity by Granules management is surprising. As the tax outgo remains similar even a one time dividend could have benefited shareholders. Although my view is that the accumulated money by JV exit could have been used in a better manner.

Dividend or buyback now are equally good/bad, tax-wise. I would prefer buyback since pool of shares is reduced and everyone benefits including future buyers. Though process is more cumbersome, it gives option to not participate, democratic.

But here they should payback their loans instead with the 200 Cr. Should reject buyback after voting, hopefully.

Midcaps are known to blow up cash in pursuing overpaid inorganic growth (and the Goodwill that exists on paper mostly) or divert money to subsidiaries/ private companies of promoters etc.

When the shares were trading lower, the management didn’t have cash to buyback. When they have the cash, there’s LTCG on the stake sale topped by the buyback tax is a painful double whammy.

In a way, it is better to buyback than to blow cash up by getting seduced into doing different things. But paying off debts is always safer.

I hope that they take all shareholders on board and exhibit good corporate behavior in dealing with this. If the prime motive is to reduce pledge by cashing in on a high buyback price, the stock’s post buyback price move may get impacted.

Next few days till 21st are going to make Granules investors busy / fingers crossed.

Q3 result and analyst / investor call is scheduled on same day, which confirms that results will be declared during market hours. As per management guidelines, the results should be good to ignite more fireworks.

Granules most of the debt is in foreign currency and has very low interest rate. Management has clarified this many times that it doesn’t make sense to pay off this debt instead if they do deposit, it will fetch higher returns. Since Granules is done with majority of it’s capex, the only few options were divided, buyback or fd. With the kind of growth company has shown, the stock is still undervalued. Still 30% shares are pledged. With this buyback and good growth in coming quarters, management might be thinking that market will take stock price higher and then they should be able to release few more pledged shares. I don’t think this is a bad move.

Is Granules in the business of drug manufacturing or earnings interest income on bank deposits? If it was so simple, why other Companies are not practicing this simple trick?

I read here that the company itself admits to not disclosing interest costs but putting them under head of capital expenditure. There is some commitment from them to reduce this in order to stop doing this fully by FY21.

Doing simple arithmetic then indeed it looks to be 2-3 % interest rate but that is almost equal to Libor. Do not think they are the Bank of America to borrow at par with Libor or lower. Their rate is Libor linked but premium to that. I suppose it will work out easily to almost double or more of Libor. It should reasonably be 7% around. Or else they should be invited to teach other Indian companies facing borrowing crisis.

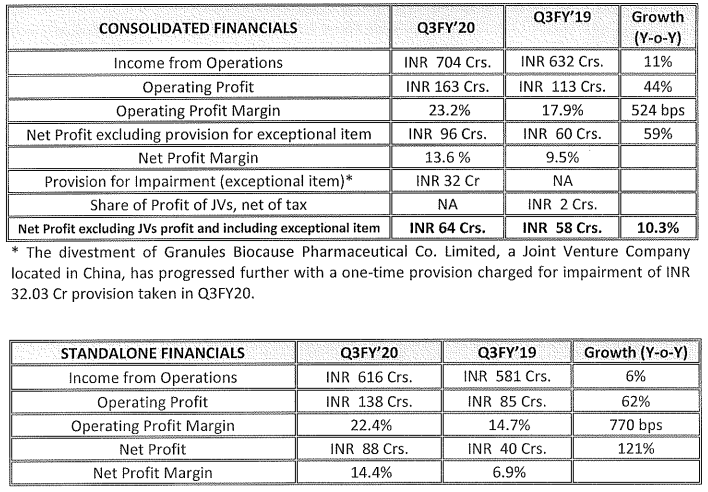

Net Profit during the quarter was impacted due to a one-time impairment of ~INR 32.03 Cr provided for Biocause.

Declared third interim dividend of 25 paise per share of face value of Re. 1/- each representing 25% of paid-up capital for the financial year 2019-20;

Fixed the record date as 31st January 2020 for the purpose of payment of third interim dividend for the financial year 2019-20.

Good results overall, and good to see that despite selling off both Omnichem and Biocause, the earnings growth has not slowed down. Some notes

1- During Capex cycle last 3-4 years multiple times there was doubt if the management is taking multiple risks in one shot. However now it seems that the risks taken have started paying back.

2- One can question if doing away with both JVs was right decision. But now we are past it. And I guess no one can deny that this disinvestment would help management focus on mother ship better.

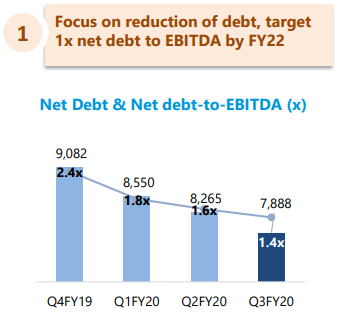

3- I am confused about the decision of buy back. With 900 crores of debt on the books I still think that the right thing to do would be to reduce the debt. But then I am not an expert. All I know is that if the Crude again goes up to $80 and above ( which has happened couple of times in last few years) then even paying 3% of interest would start weighing down the earnings considerably.

4- Keeping buy back aside, I like few things company is doing - focus on free cash flow, debt reduction and pledge reduction.

5- Formulations have gradually gone beyond half mark contributing to the business. So Granules the company which provides APIs for generics is changing fast.

6- The current upthrust in topline and bottom line should sustain for next couple of years because of sales moving from EMs to regulated markets and better sweating of newly built assets. The better mix towards FDs, selling OTC drugs in US, and new drug launches should also help. After two years the Onco APIs should provide the next kick.

7- Key risks in my opinion are

Crude prices going up

High debt on the books. Working capital increase will make it look worse.

Poor execution of plan including launch of Onco APIs ( tough nut to crack based on the little I know about this segment).

MGT said in the concall that their pledge will come down to negligible 5 percent, but rough calculation shows that they still have 4 cr shares pledged , so out 25.42 cr eq, they have 43 percent holding ,sothat comes to 10 cr shares now come to buyback which is 5 percent so they are entitled to 50 lakhs shares so roughly they get 100 cr from buyback now pledge of 4 crshares amt to 350cr if v take price of 90 that math MGT is saying is not matching as per my calculations , correct me if i m wrong , views invited

Ballpark numbers:

Today’s market cap Rs 3800 crs

Same pledge was there when share price was roughly half (c. Rs 75-80) i.e. c. 1900 crs

Value of promoter pledged shares at that time 1900*43%*37% = 300 crs

Typical cover on loan against shares 2x, roughly INR 150 crs loan outstanding at promoter level

In buyback promoters will get 10 cr shares * 200* c. 5% = 100 crs

Loan remaining c. Rs 50 crs

Pledge required @ 2x c. Rs 100 crs

As a % of promoter shareholding 100 / (3800*43%)= c. 6%

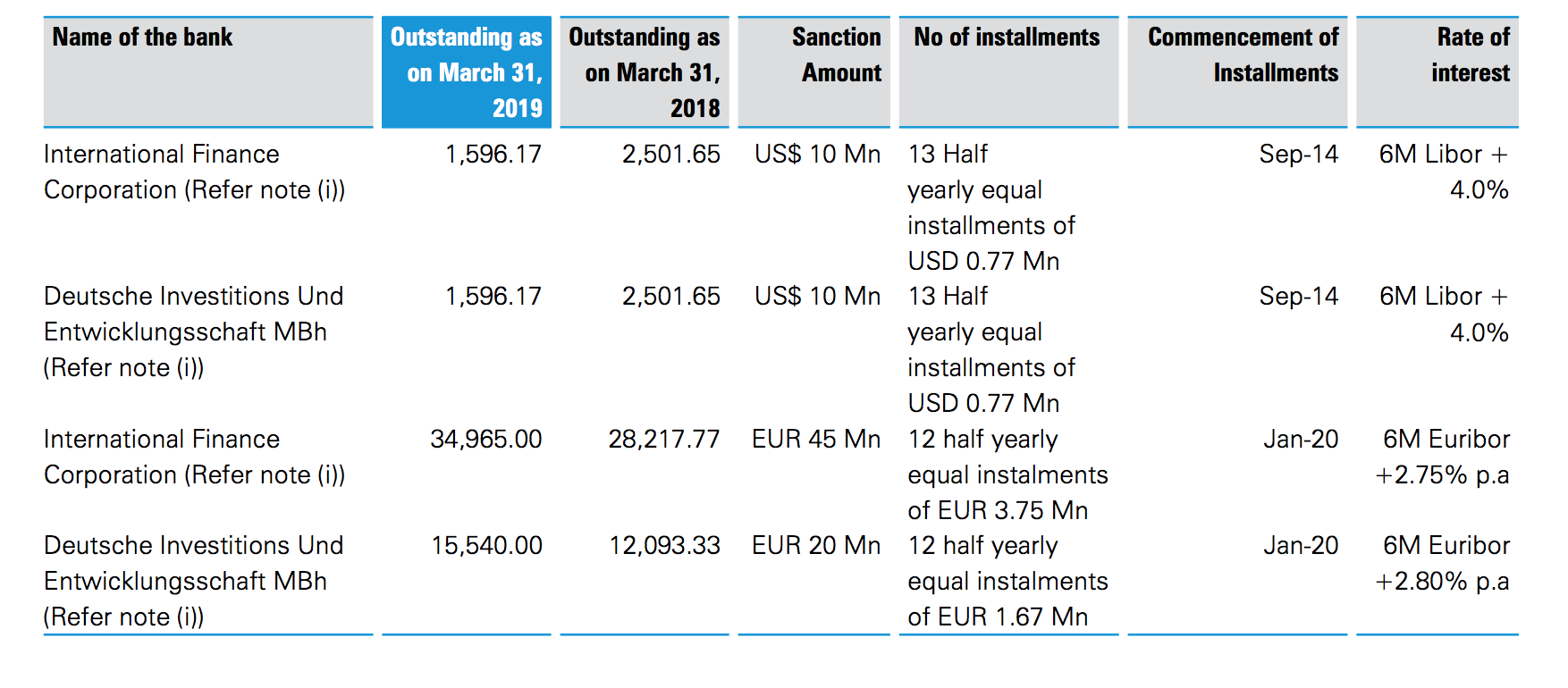

As per the AR18-19 following are the outstanding loans. Loans taken before 2014 have rate of ~Libor +4% and latest loans have rate of ~LIBOR+2.75. But, Mr. Krishna Prasad mentioned in the latest call that interest rate is around ~1.5%. Wrote an email to the company. Let’s see what they will say.