Few important points

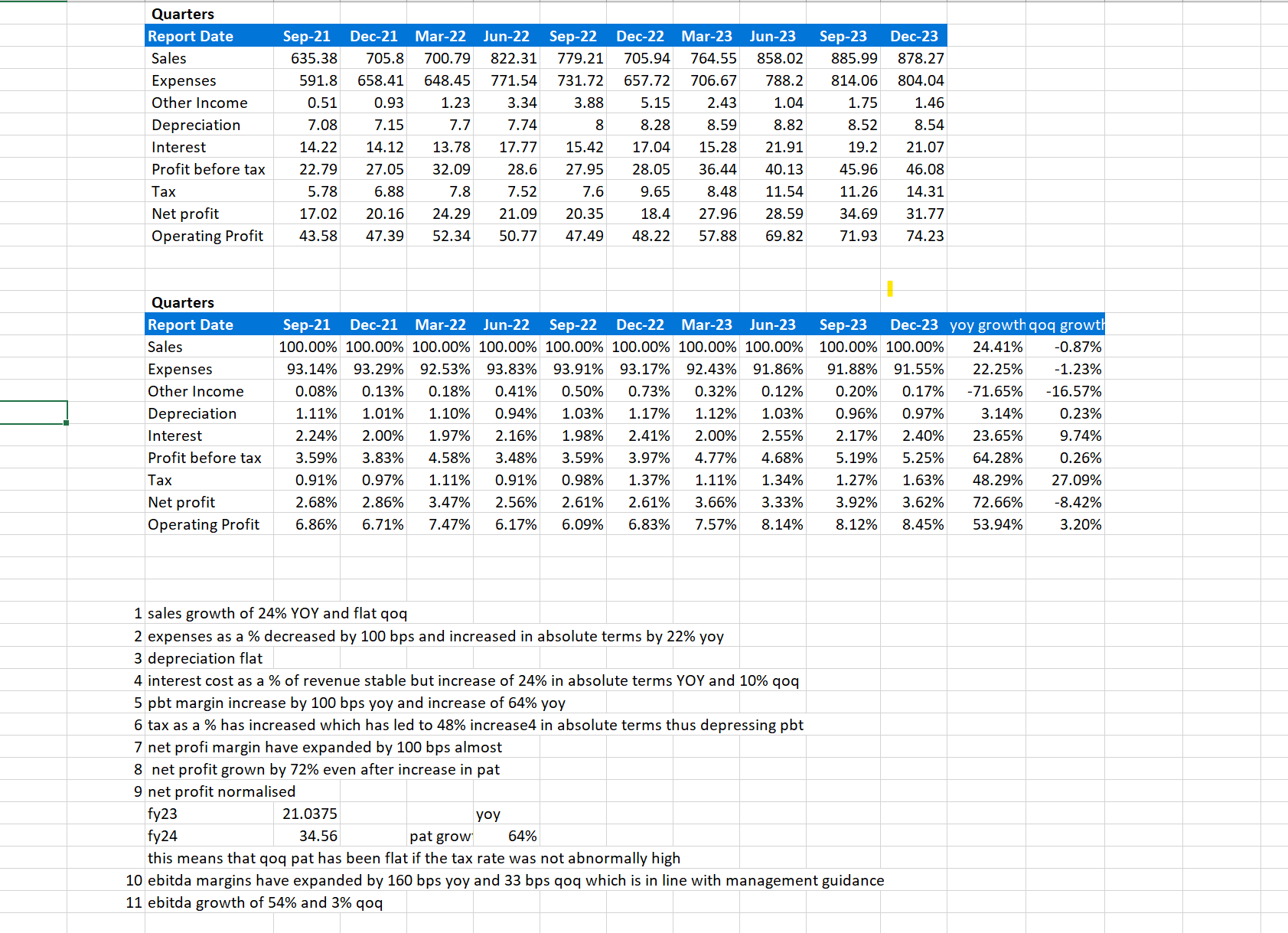

- Freight cost are not passed to any customer in any of the business division(Ref 1)

- Hot rolled tubes raw material prices can not be passed to the customer of CR Sheets & Pipe & Hollow Sections. They are short term contracts. The margin that the company earns in short term contract busines is dependent upon the raw material prices.(Ref 2)( Ref 4)

- Zinc raw material price is not passed to Pipe & Hollow Sections customers as it is a short term contract. Pipe & Hollow Sections is the regular low margin, short term contract based business.

- In case of structures business also Engineering Structures, there is partial cost passing in some of the products(Ref 2)

- Precision tubes business there is direct passing of the cost of zinc and other raw materials. Though there seems a limit upto which they can pass through the prices.(Ref 3)(Ref 2)

- While negotiating new order contract for the their value added products, it does not seems they have considerable power. If the prices of the raw materials remain in certain range, there business is supposed to do good, as it brings some pricing power to them in value added products. Though if the material prices increases very sharply there margin in the value added products gets impacted for the existing orders. The impact in the margin of the CR coils and other regular product is huge as it is more of the commodity business.(Ref 3)

- As it is a low margin business, even 1 percent point increase in margin, is like more than 10 percent point increase in operating profit. Therefore, it is equally important as the new capex utilisation.

In the near term(upcoming 1 or 2 quarter results) it is more important than the capex in precision tubes and forging.

- I tried to find the percentage in volume of zinc is utilised in CR Sheets & Pipe. It seems the percentage in terms of volume is 1-1.5% and in cost terms it is 4-6 percentage of the raw materials utilised. I have assumed the zinc coating to be 20 µm thick and the wall thickness of 2 mm to calculate higher end percentage. Also I am assuming that all the CR sheets and pipe will require galvanisation.

- Freight cost is nearly $2- $4 per kg per 1000KM through sea route for the items shipped based on my estimates. This can be way off though. In percentage terms, it is low. It can not be passed to the customers.

- They buy the materials on month on month basis. Therefore if they have the order book of 6 months, the margin might get fixed considering that time raw material price. If it is high earlier, then there margin might expand in coming quarter and two. If was less earlier, there margin might contract in coming quarter or two. The effect of the margin change mostly occur due to their old regular business of CR Sheets & Pipe(commodity business) and structural division(little cost passing).

-

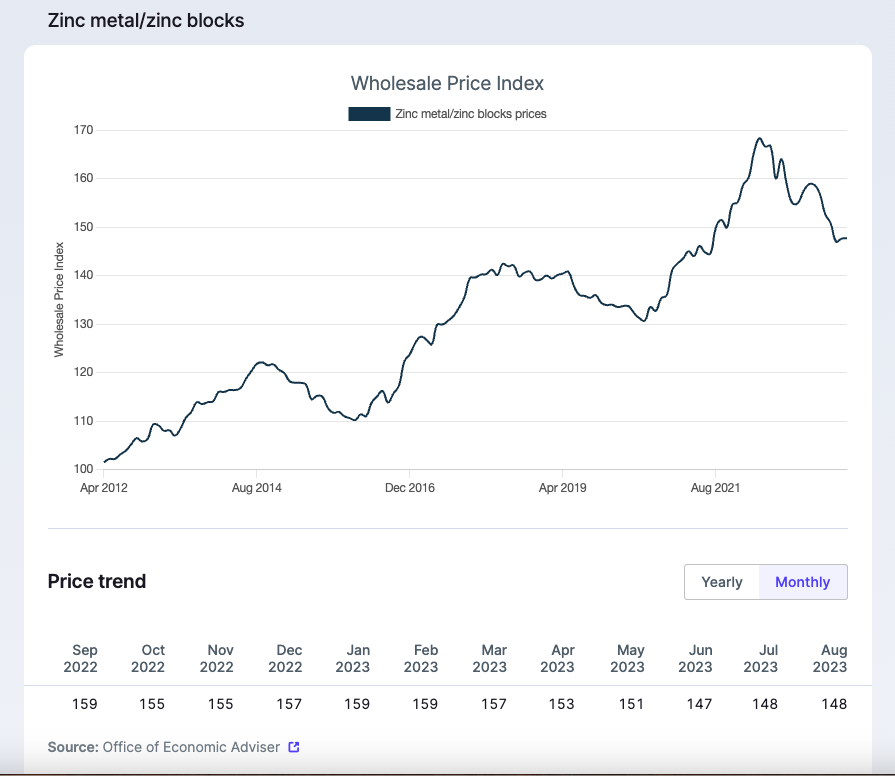

Price trend of zinc over months

Price trend of hot rolled coils

As from the graph we can see the price has cooled down for this JAS quarter, hence we might be looking at the margin expansion in the coming quarter by near to 1 percent point. It will mostly help them in the structure business for which they have fixed the price as per high raw material prices. Also there will be margin revival in the regular business.

- They also get impacted by the anti dumping duty on their raw material HR coils. Capacity of HR coil in India is low and hence they are dependent upon import.(Ref 5)

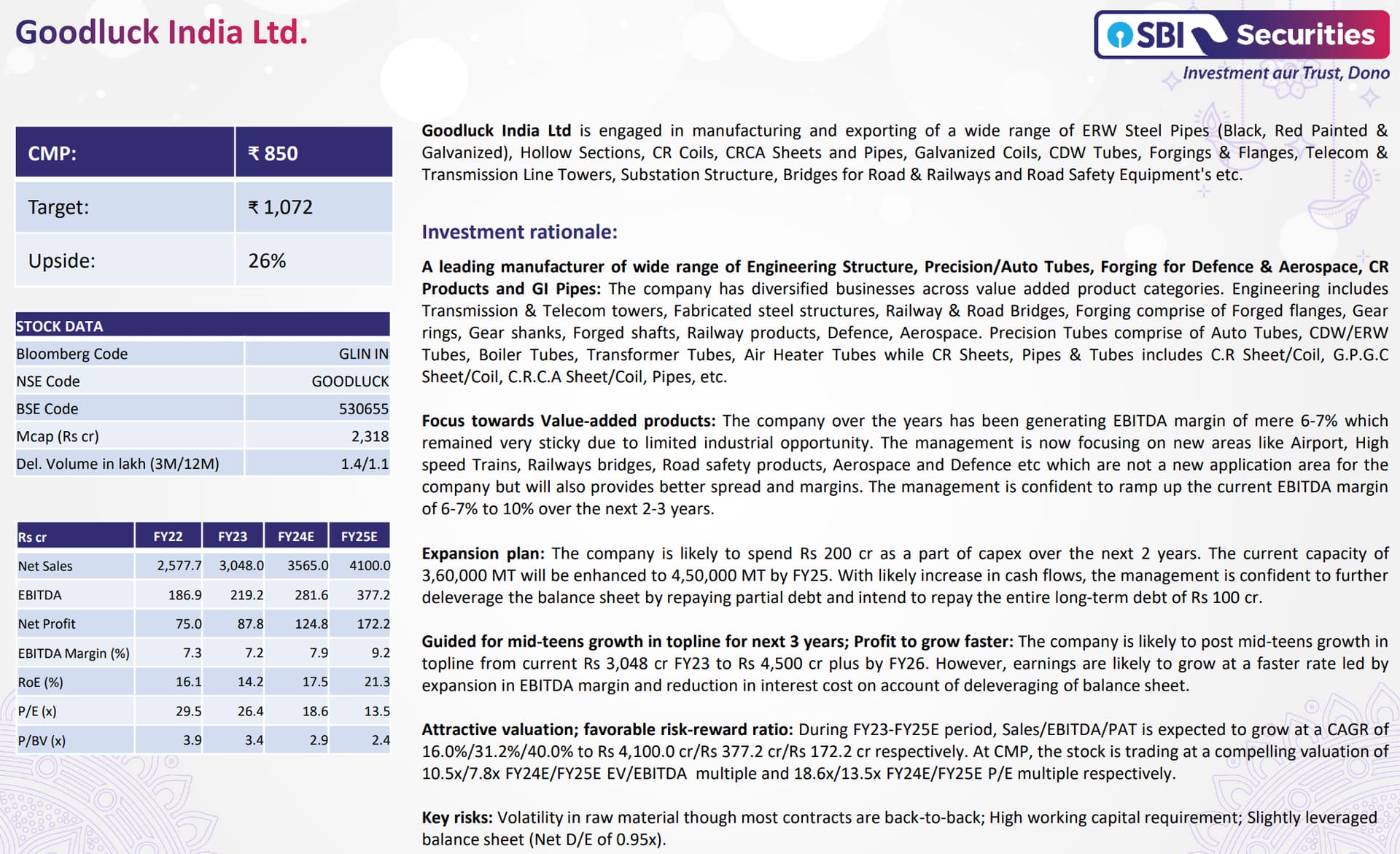

Valuation

-

The reason this business gets low valuation is that thier more than 50 percent of the business is directly impacted by the raw material prices. Structure business margin though gets impacted for only 1-2 quarters(until they start getting new orders) but the impact on the regular volume business seems, is kind of permanent until and unless the raw material prices corrects due to its commodity nature.

-

The margin impact on the structure division might go over 1-2 years also. As there is whole bidding process. Currently we are in tailwinds due to low raw material prices.

-

If there sales from the precision tubes and the forging division grows, it might bring the stability to the business. For few coming years still the impact due to their regular volume business will be there as when raw material price increase.

-

In short term as china going through the recession kind of thing, hence the raw material prices has decreased and it seems that china might take atleast some time to recover this time. Helping them in the commodity business of theirs.

-

Engineering Structures & Precision Fabrication might eat their cashflows as the vendor with which they work with to get the contract have very bad payables days like L and T. Hence I don’t like this division.

-

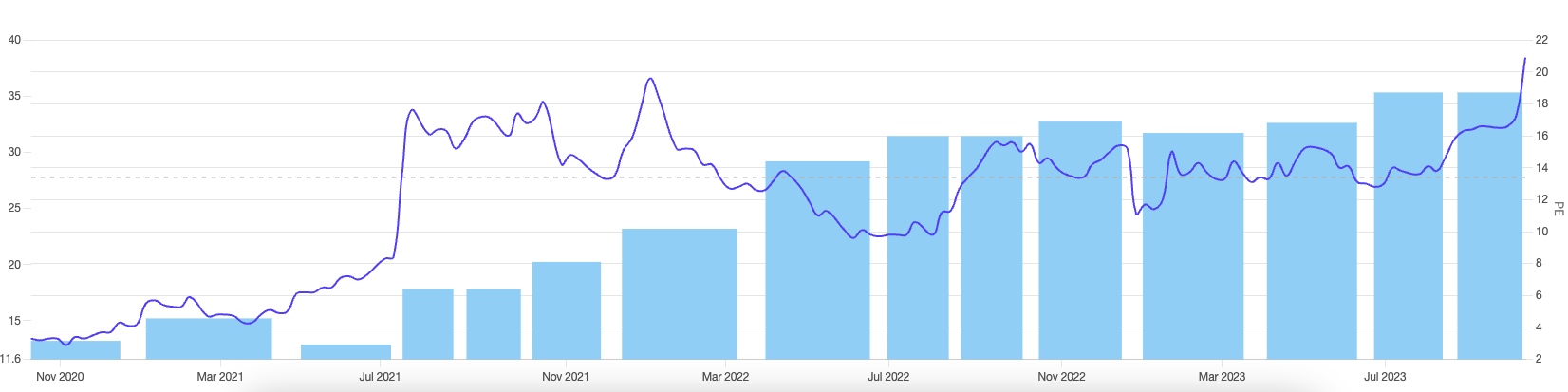

Change in PE Ratio with time, see it in compared with the raw material prices. It gets the valuation of the cyclical industry.

References

Ref 1(Q2 and H1 FY2022)

It impacted greatly. We have been negotiating with our customers to pass on the freight, but

we are an exporter of the last 20 years so we have to honor our commitments and some of

the customers have obliged us. Of course, it will in the subsequent times the freight they

will have to pay but for some time we have taken a hit on the freight also.

Ref 2(Q1 FY18 Earnings)

Look, I tell you the auto tube division is totally insulated, we get the price variation. Structure division, only some of the products like lattice has a price protection, but solar division does

not have any price protection because the order tenure is very short. As you think of

percentage, it could be 50-50 almost, you can assume as a whole for the company. But one

thing I can tell you the price volatility of our raw material prices definitely impacts us. In the

long run, neutralizes when the prices go down, so we get the advantage. When the price go up,

we take some hit, but on a long-term basis, we will see it does not impact. On a month-to-

month or quarter to quarter, it may have an impact, but one quarter it will have a negative

impact, the other quarter will have a positive impact.

Ref 3(Q3 FY17)

Margins reduced 9.6 to 6.44 QoQ

Mr. Garg has pointed the third quarter results, the rampant unrelenting

increase in raw material prices by as much as 30% to 40% coupled with a mega event of

demonetization has impacted demand badly.

Price increase is normally passed through with a

time lag, but this quarter is unique because every month raw material prices have been

increased and price increase could not be settled by major auto and OEM customers. Heavy

price increase month after month has affected our net sales margins, it was difficult to cut

through steel weights, all the price increase affected by the steel producers.

Ref 4

When asked about the margins of different products at different timeframe.

In Q4 FY16

Cost of the raw material prices Q4 FY16 with the

Crude WPI near 60,

Hot Rolled (HR) Coils & Sheets WPI near 90

zinc WPI near 120

Like if you talk of railway work it is between 15% to

16% but if you talk of this transmission and towers it will be only 10%. And

solar if you talk it may go to 14% to 16%. And this is a demand dynamics. If

demand is more we can get more prices.

Basically now we have this value added segment, it has moved to 53%. So in this sector the margins are in the range of 10% to 15% but in the regular Good Luck Steel Tubes Limited sector of pipes and cold rolled sheets ERW pipe what we were discussing it is

in the range of 5% to 6%

In Q2 FY22, when asked about the margins of different products when

Hot rolled pipes WPI → 160

Zinc WPI → 170

Crude WPI → 170

The structure is almost 10% EBITDA and

our CDW Tube it is 14%, forging again 14% to 15% and the precision tube section it takes

9% to 10% and our regular volume product, it gives almost 2% to 3%.

Ref 5(Q3 FY17)

From concall

Sir, let me clarify, there is no MIP on HR Coil as on date, there is only minimum price which

government has set below which we cannot import, that is $471. And as soon as we import at

$471 then we are involved with the custom duty and safeguard duty and anti-dumping. Antidumping is already in place for HR coil for three years, safeguard is also there for three years.

On HR coil it is already in place, there are other products of steel which government is thinking

of putting the duties. So, HR coil anti-dumping regime exists today. MIP is not there. But today

landed price of HR coil from international market is much lower than what we people have

priced, there is no threat of import to HR coil manufacturing in the country. So they have got

absolute pricing power and we will there, they have increased prices unwarranted in a very,

very aggressive manner which has affected the processing industry as a whole.

Disclaimer

Please verify it from your end. I am invested and biased.