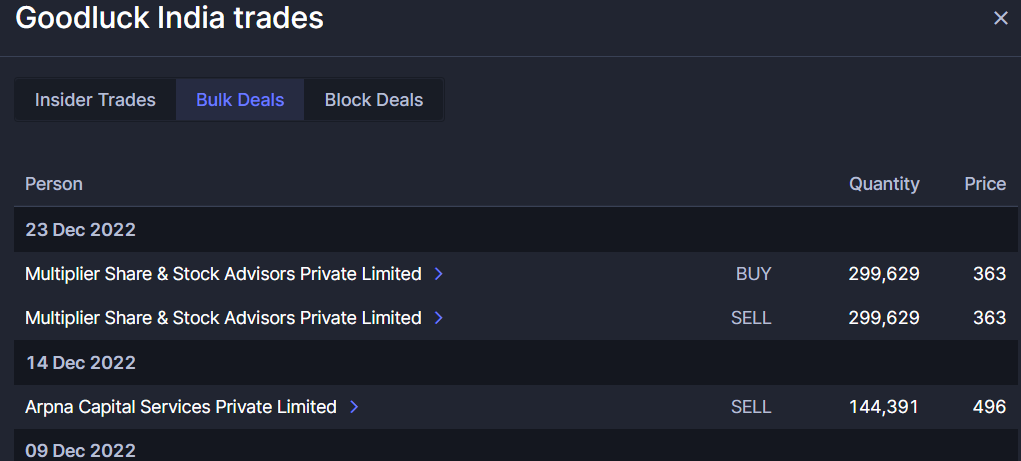

Thanks for sharing. It seems they might have off loaded completely yesterday?

They had even sold some quantity on 14th Dec 2022

Thanks for sharing. It seems they might have off loaded completely yesterday?

They had even sold some quantity on 14th Dec 2022

Disclosure by Arpana Capital …Diposal in Nov

As Per Prabhudas Lilladher Management meet report.

If we see the margins Precision tubes has 24 % of the revenue but contributing about 42 % in EBITDA.

Recently received Letter of Intent (About Rs 2 Bn) from L&T on the first Bullet train project in India for supply and fabrication of special bridges required for high speed tracks.

Total forging capacity is ~32ktpa from 12ktpa earlier enabling volume growth - Added one fully automatic metal pressing unit with Rs 400 mn.

This addition in the capacity also helps in increasing the margin of the company.

Need to see how this will play out. Please add/correct me if I reported any wrong numbers / information.

The above mentioned information is from the ‘Management Meet Update’ by ‘Prabhudas Lilladher’ on July 31st 2023

Remarkable report by prabhudas liladher is available for free on their website:

glin-31-7-23-pl.pdf (909.1 KB)

Disclosure: Have a position, biased

Can you please share your thesis for investing in this?

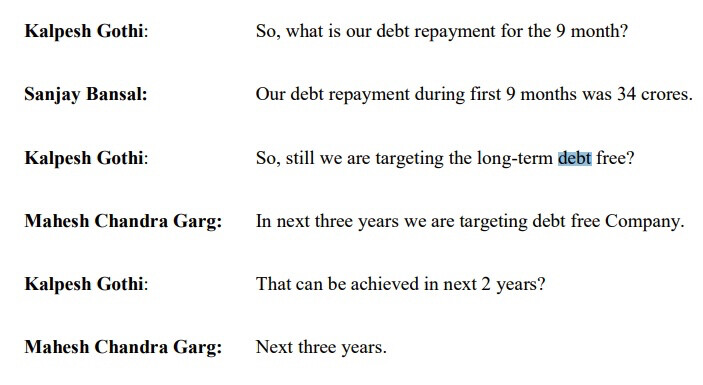

Correct me if im wrong. As per their previous year concall, they are planning to reduce long term borrowings.

As per the screener their longterm borrowings are reduced.

Does this mean company is moving in right direction?

Also I saw only two concalls in last year , is there a reason why they are not conducting more concalls?

Just to add.

Exercise of Preferential allotment is also pending.

22,54,600 shares needs to be exercised within 18 months i.e 1st half of 2024.

If converted shareholding will move by 3%.

My notes on Goodluck India:

GI was started in 1986 by Mahesh Chandra Garg, operates as a diversified engineering conglomerate involved in the manufacturing and distribution of a wide range of engineering products.

Without beating around the bush lets get straight to the point

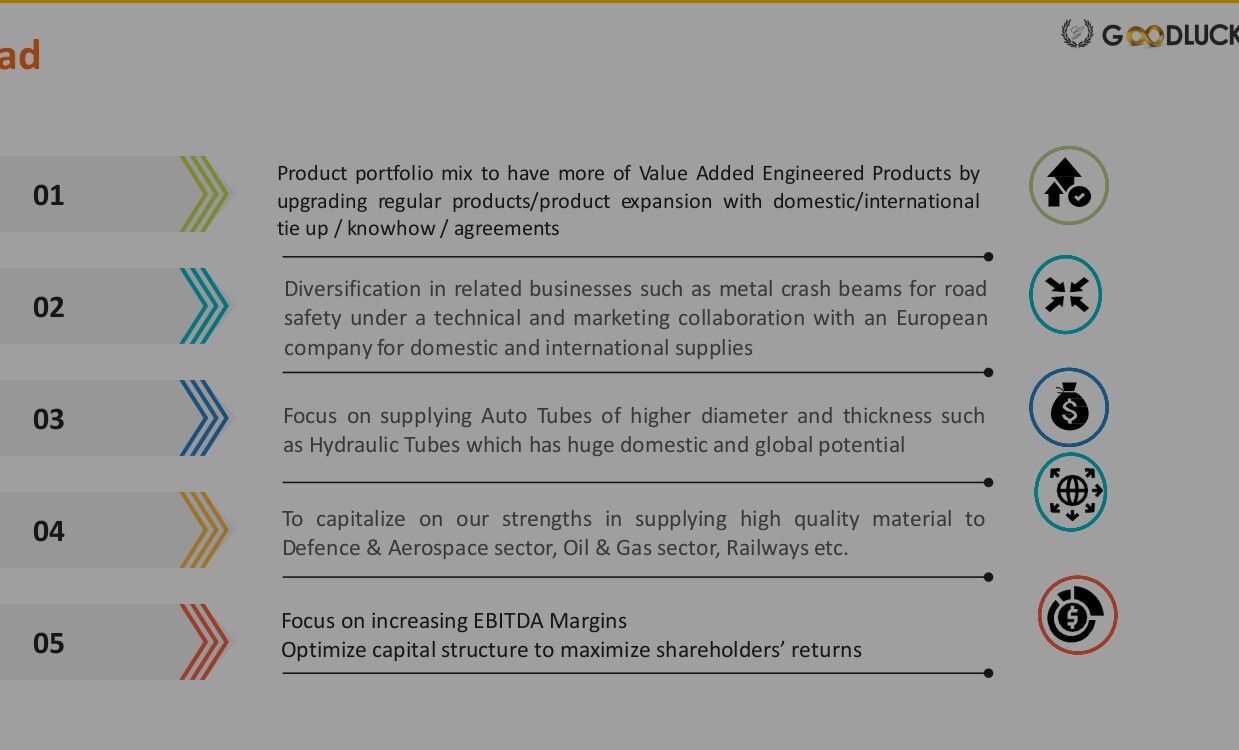

Company has 4 segments that drive most of the revenue in:

The company also excels in producing structures tailored for Roads and Highways, encompassing Bridges, Signage, Light Pole structures, W Beam Crash Barriers, Security Towers, Telecom Towers, Foot Over Bridges, and Under Bridges.

Recent updates:

A structures unit has been established in Kutch, Gujarat and the supply of materials to L&T is already in progress, and the management anticipates that it will take approximately 12-15 more months to fulfil this order. Company is a category-1 supplier to critical components required for various projects of L&T in the domestic infrastructure space.

Management commentary: “There is a huge scope of growth and expansion in this segment and we envision an order book of over Rs.1000 crore in the next 2 to 3 years”

This segment contributes 15% to the overall revenue and 16% to the entire EBITDA.

Management commentary: “The segment is a substantial contributor of export revenue to the Company. We are supplying to some of the most respected brands across the world in both in Roads and off-road auto segment (BMW, Audi, Mercedes etc). The Company has been gradually consolidating its export business. The excellent range of products and services have enabled us to extend our presence in hundred countries across the globe with a base of over 600 customers. The current domestic to export revenue stands at 58 to 42”.

This segment contributes 14% to the overall revenue and 22% to the entire EBITDA and this might increase going forward.

Management commentary: “If you talk of forging Bharat Forge, very big name, we are very distinct cousin to him are making 10,000 tonnes. We are making 2000 tonne. But definitely we aim to. So, basically, we were on the defense side, so it will take some time to really identify the products. But the machinery is there and government has also to identify which products they want to source from India and what are the critical products they are they have to still import from overseas.”

“forgings, we are having a visibility of almost 5 to 6 months orders”.

This segment contributes 47% to the overall revenue and 20% to the entire EBITDA and this might decrease going forward.

Management commentary: “One other sector is CR coils, pipes and tubes, which is our oldest sector here. We manufacture ERW pipes and tubes that find application precision tube, support structures and other infrastructure, agriculture, auto and many more”.

Disc- Invested

Goodluck India Precision Tubes are TESLA, Mercedes, Porsche

approved products. A good probability it’s tubes.

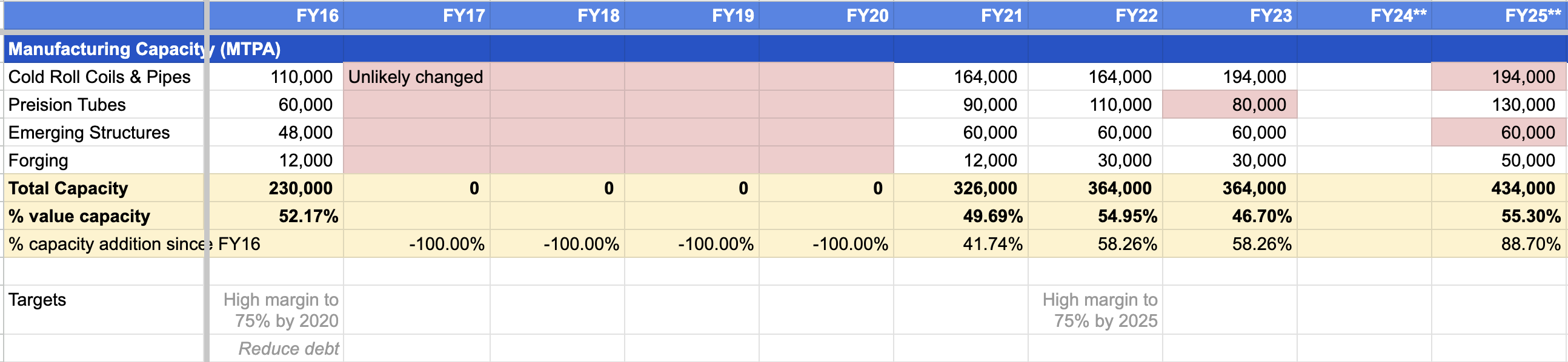

It’s interesting to see how the management dealt with the downcycle and trying to achieve targets from 2016.

** Anticipating the future. Actual data could be different

Disclaimer: Not a BUY/SELL recommendation. Please do your own research. I often go wrong and change my views without sharing. No investments in Goodluck India to date.

Goodluck India.pdf (569.5 KB)

Issue of Warrants.

dc649b46-fba5-4db3-b51a-9f4a167bfdf5.pdf (832.7 KB)

Warrants to Promoters @Rs.600/- of 5lakh number & Non-promoters @Rs.600/- of 11lakh.

Management targets 4200 cr revenue by FY25 and I assume the co would grow 15% in FY26, taking the revenues to ~4800 cr.

In Q3 FY22, the management expressed their intent to become longterm debt free in 3 years, i.e. by FY25 and and the debt at the time was ~480 cr. The debt in fact to increased to 577 cr by end of FY22 and stayed same at 586 cr in Fy23. So, the execution in this direction is not good. However the co issued 12.5 lak warrants and 22.5 lakh equity shares in FY23 at 450 per share (total amount around 157 cr, but AR mentions equity infusion of 77cr (25% of warrant price and full price of equity shares should be higher than 77cr).

The co today issued 5lakh warrants to promoter and 11 lakh equity shares to non-promoters at 600 rs per share. Total amount would be 96 crs.

The amount raised from these warrant and equity infusion would help bring down the debt partially and also would fund growth.

The management indicated the EBIDTA margins to be in the range of 10-10.5% (by FY26) as the product mix improves toward more value addition (currently ~8%).

From this EBIDTA expansion, operating leverage and lower interest cost (as % of revenue) may lead to Net Profit margin of 5% or more (2.9% for FY23 and 3.4% for Q1Fy24), as per my esitmates

So, the Profit would be 4800*5% = 240 cr, where as the current Market cap + Debt = 1694 + 586 cr = 2300 cr. add 171 cr to this to account for equity shares to be issuesd.

So, EV is ~2470 cr

So, the co trades at ~10x EV/Profit in FY26. So, I expect the share price to perform well in near futures and double in next 2.5 years (considering 20x EV/profit in FY26).

Downside risks:

Possible Upside:

Overall a decent opportunity for medium term (2.5 - 3 years timeframe), with equal upside and downside risks and a way to play the Indian Manufacturing and Infra theme

you need to check the break-up of debt. long term debt is decreasing from 128cr. to 91 cr. from fy21 to fy23 . whereas short term debt is increased by 373 cr. to 507 cr. i think management intent is to reduce long term debt . because currently 50% + business is value added so they have to maintain high inventory in these segment . so working capital is always remains streched . due to this short term debt can further increase from here because they are target 75% business from value added in fy25 . Its more of a nature of business ( pix , racl and other high inventory value added business ) .

Hello Ashok

Thanks for correction. I checked the transcript and it seems the target was long-term debt free and working capital debt would be there. People like you add value to the community (Thanks again)

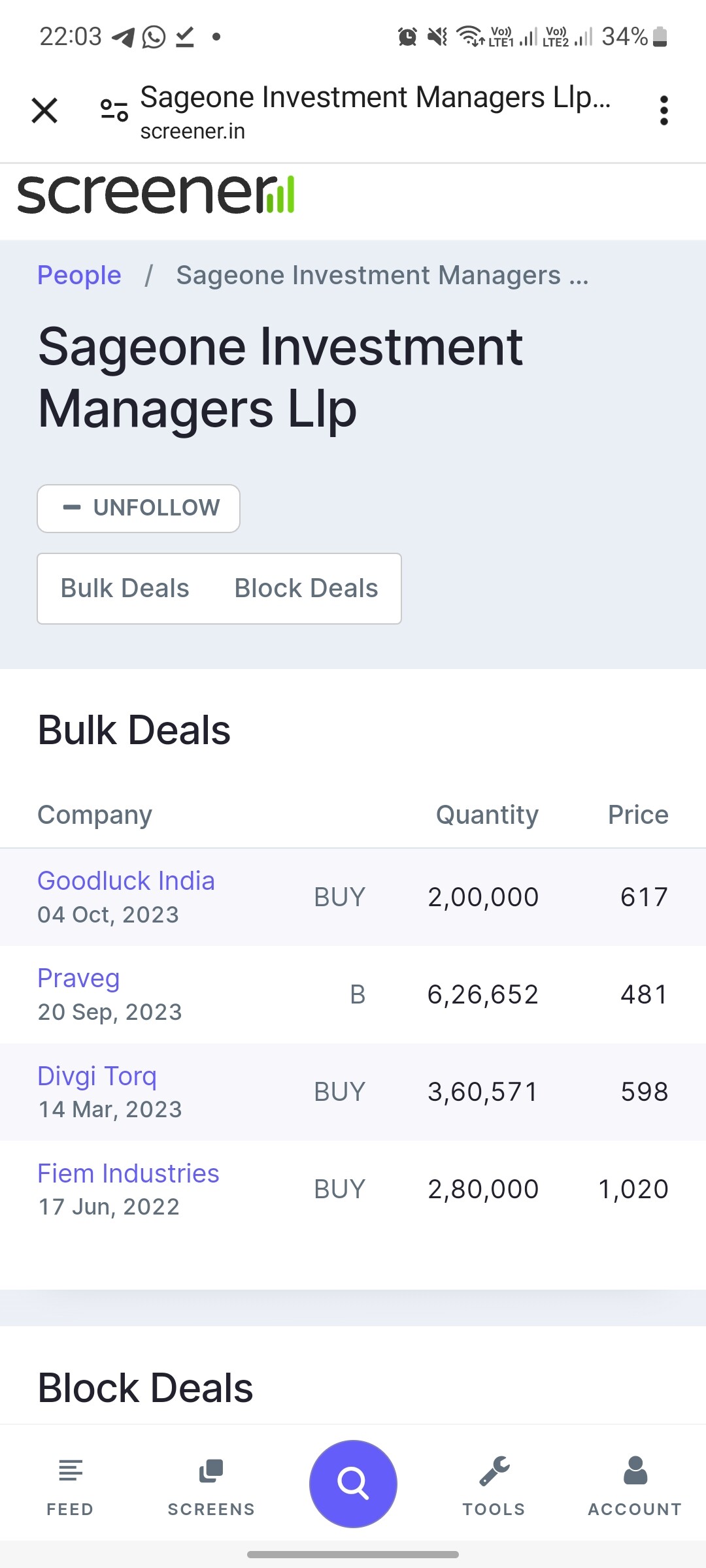

Bulk Deal:

Sageone Investments (CIO Samit Vartak) bought 2lakh shares today at 617rs per share.

Info from @LearningEleven on twitter (Sorry info not yet appearing on NSE or BSE website)

How the money will be utilised, The company explained here, in the latest Press release.

Few Insights from Jan FY22 Concall :

But recent managemet meet, the the target for FY25 is mentioned as 4200 cr. If they can grow at this rate they may achieve the 5000 cr target by FY27 or slightly before

Interview with ET now: link

I’ll update this post after listening to latest concall again and add more notes from management meet posted above. Plan to use these as KPIs to see if management walks the talk or not. But they seem to be on track, as long as the current demand environment continues