Businesses

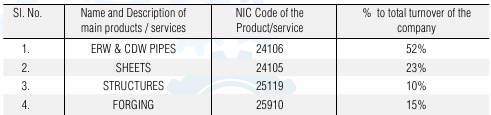

Goodluck Steel tubes is engaged in manufacture of Steel pipes and sheets diversifying into more valued added products like forged components for auto & railway industry and structures for power, telecom and solar industry.

Expansion

GoodLuck Steel Tubes has lined up following expansion over next one to three years.

- 30 crore expansion of new Structures unit. Should start production by March 2016. This expansion will expand companies margin.

- Setting-up a new Auto Tubes, Heavy Support Structures & Forging plant in Gujarat at cost of 260cr.The project will implemented in two stages first will be Auto Tubes & Heavy Support Structures and second stage will forging.

Financials

Q2FY16

Long term Debt = 76 cr

Short term Debt = 220 cr

Cash = 8.4 cr

Current Assets = 382 cr

Current Liability = 307 cr

Key Concerns

- Future profitability depends up on the managements ability to successfully diversify into more value added products.

- Implementation of expansion projects in-time will be critical for growth of the company.

Key Positive

-

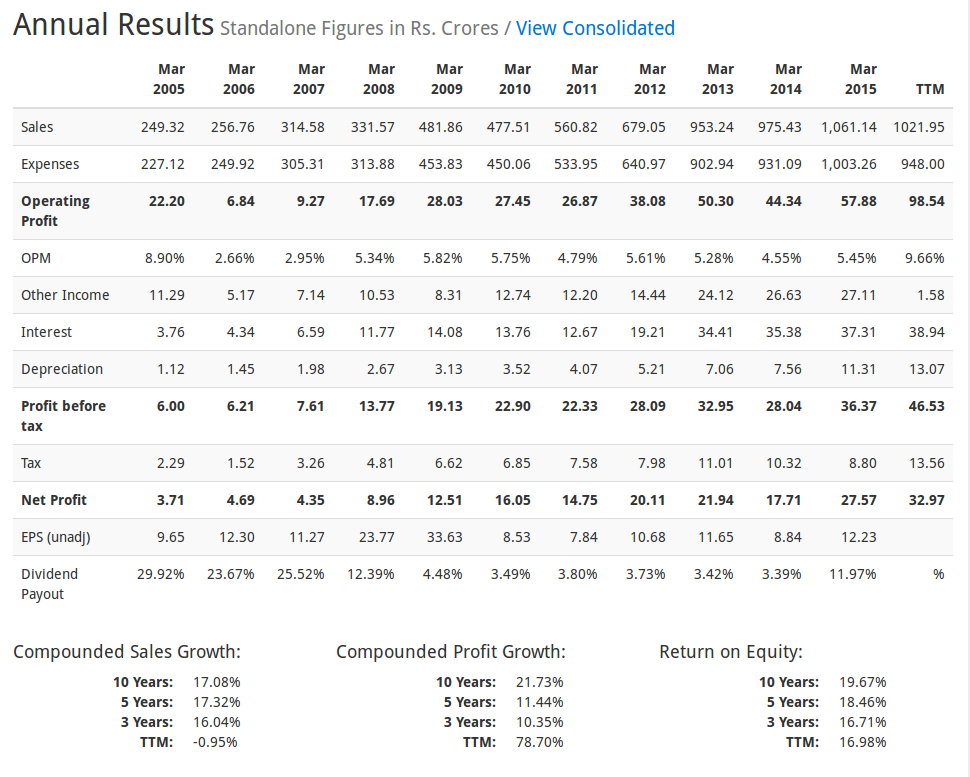

Investment at current market price provide good margin of safety. TTM PE = 5.95

-

Company is showing improvement is OPM over several quarter from 5.x% to 9.x%

Disclosure

Invested with tracking position