Business Overview

a. 43% growth in revenue in Q2;

b. Order book of approx. 200 cr

c. EBITDA margin of 20% in Q2 FY 26; EBITDA margin guidance of 19 to 22%

d. Transitioned from a natural diamond in-store jewellery company to a major supplier of LGD Jewellery. LGD contributed 90% of overall sales. My notes – This figure was 34% 2 years ago and 76% 1 year ago.

B2B business

a. Despite LGD contributing 90% to revenue, for the larger retailers in US – LGD is less than 30% of their sales. Lot of headroom for growth.

b. Currently growth has come from increase in wallet share among key customers. Also added some Corporate customers in US My notes – Online LGD contribution has remained flattish on YoY basis; focus has been on increasing presence, having wider presence in instore LGD sales

c. Confident of healthy double-digit growth CAGR over next 2-3 years

d. Higher Inventory buildup, in preparation for holiday season in US in Q3 and also due to US casting model. Likely to normalize in Q3.

e. Gross margin likely to have fluctuations QoQ basis; due to factors like volatility of RM price (booked at one price and sold at diff rate).

Growing acceptance of LGD in Other Geographies

a. Seeing very robust demand globally

b. Started with new customers in Israel, Middle East and in Australia

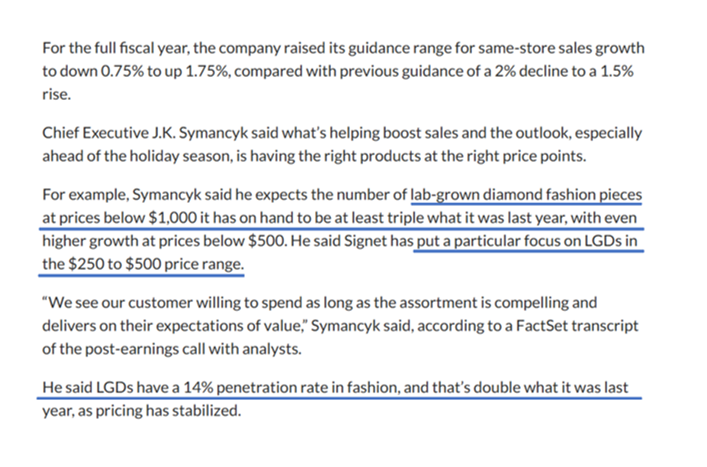

My notes: This is what Signet stated recently – Traction in LGD fashion pieces at price point below $1000

US origin Casting model

a. Casting of raw gold into unfinished jewellery pieces in the US, cutting and polishing done in India and then shipped back to US. Casting cost is incurred. Have been able to pass on the cost to customers. Likely to have a Gross margin advantage over other players. (slightly higher prices)

b. Helped in minimizing tariff impact. My notes – This is a strategy which some other players like Renaissance Global have also adopted (Country of origin UAE casting model) in order to minimize tariff impact. Would be interesting to see what strategy Goldiam adopts if tariffs were to normalize

Fund raise of 202 cr

a. 190 cr is unutilized still

b. Provides capital for launch of about 50 to 60 stores. All under COCO model.

Origem

a. Now operates 11 stores

b. Older stores like Bandra, Borivli, etc are doing well

c. Few have achieved Break even, most Inching to break even,

d. Stores in Delhi & Bangalore also doing well.

e. October saw strong festive demand

f. Aspiring to be a national brand in LGD; having presence across geographies.

Store economics

a. 2.5 to 3 cr is the inventory requirement per store. (40% is gold value)

b. Break-even levels are approx. 20 lakh revenue per store per month.

Origem store launch plan

a. 15 to 18 additional stores are in various stage of negotiation and launch

b. Targeting 20 to 25 stores by FY 26 end.

c. Focus is on best-in-class location.

Marketing campaign

a. Working on many exciting marketing campaigns to boost awareness

b. Evaluating, having a celebrity as brand ambassador as well

Competitive Edge

a. Only brand which is vertically integrated.

b. Having distribution (national store fleet and presence) likely to be a differentiator in next 12 to 18 months going forward, vs other younger LGD startups which are coming up

c. Global product designs also a likely differentiator

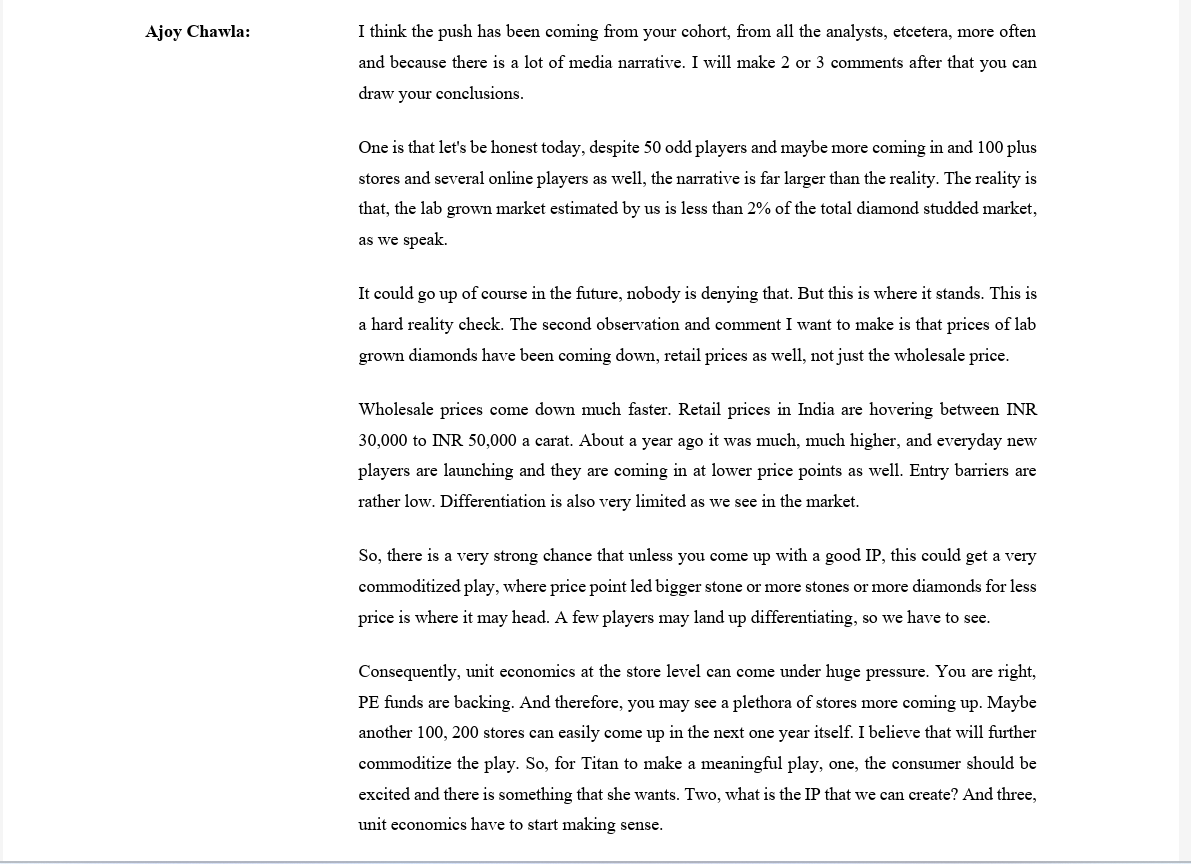

Other organized retailers entering LGD retail space

a. Will only help boost LGD awareness among customers and help in actually growing the category as a whole

b. Consolidation may play out in the segment, in coming years; and smaller players (below 10 stores) may not remain relevant in national scheme of things & fade away

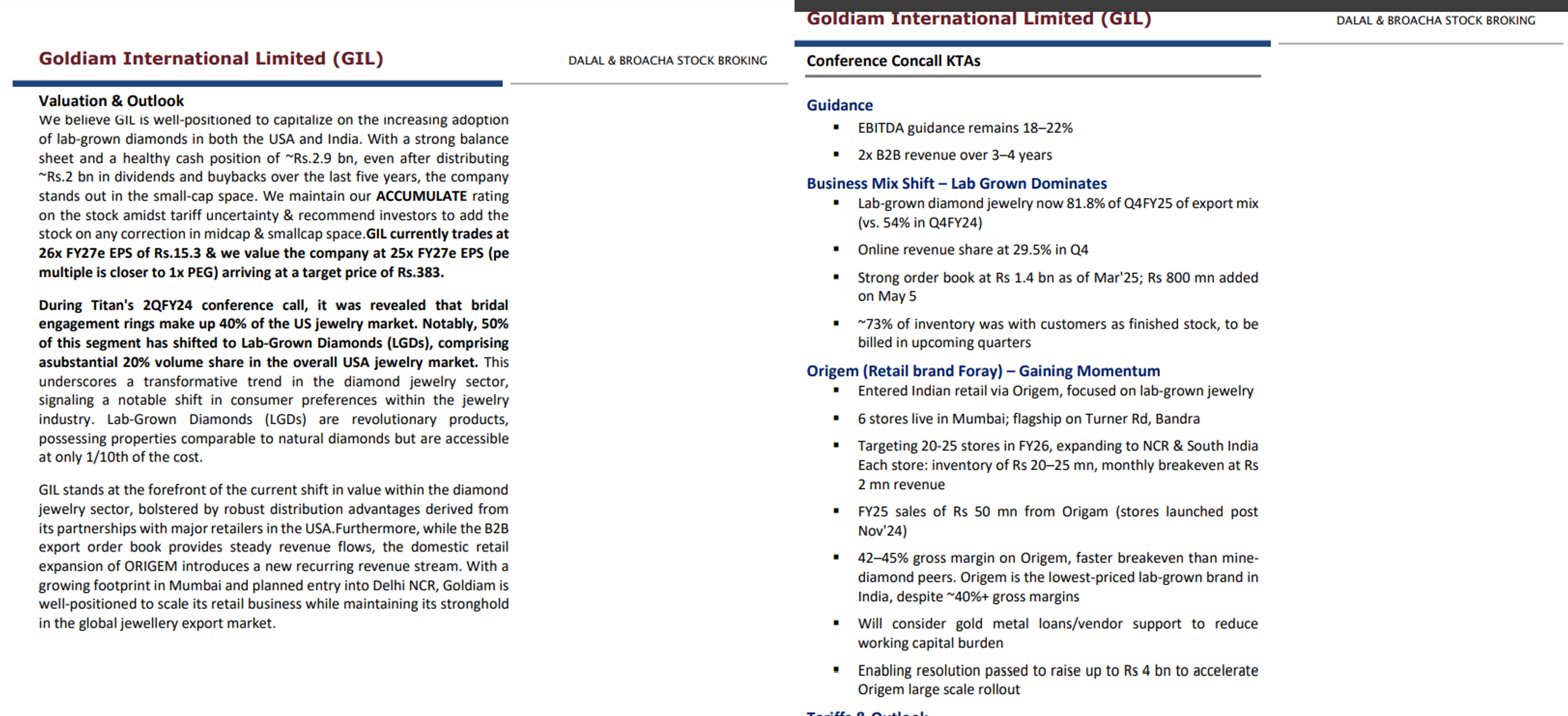

Interestingly, Dalal & Broacha has a bullish view on Goldiam. Posting a key extract from their report, after Q4 FY 25; not sure if we are allowed to post the report.

On a separate note, an interesting take on the disruption caused by LGDs, from the CEO of a leading jewellery company having over 100 stores across US.

These big daddies will enter in the fray the moment market for LGD jewellery grows…Maruti was giving the same logic for EV…but now launched EV Grand Vitara…Titan themselves invested in LGD co. USA…

Again Trent, Tata co. also launced LGD brand POME here…Just now Titan defending their market of natural diamond jewellery with such a narrative but sure they are keenly watching and will be first one to jump the gun once market size grows…

Fair enough. In a way, because the established players are reluctant or delaying their LGD foray, the field is full of newbies who are ready to try and are lured by the huge market opportunity. But then, most of what Titan Mgmt. said also appears true, going by the newsflow.

50 odd players and more joining along with several online stores. Everyday new players are launching and coming at lower price points. Low entry barriers with limited differentiation.

Prices of LGD is coming down (of course so is that of ND) but i don’t think there is any chance of LGD ever recovering from this cycle of cost & price erosion. ND? Maybe:MaybeNot

PE funded, store expansion is happening as we speak. But we know at some point the funding tap stops and then the differentiation happens.

While evaluating Goldiam, we have to keep these aspects in mind. Rest, when Titan and other biggies come into the market, the nature of the market itself may have changed by then. We don’t know who will be still standing.

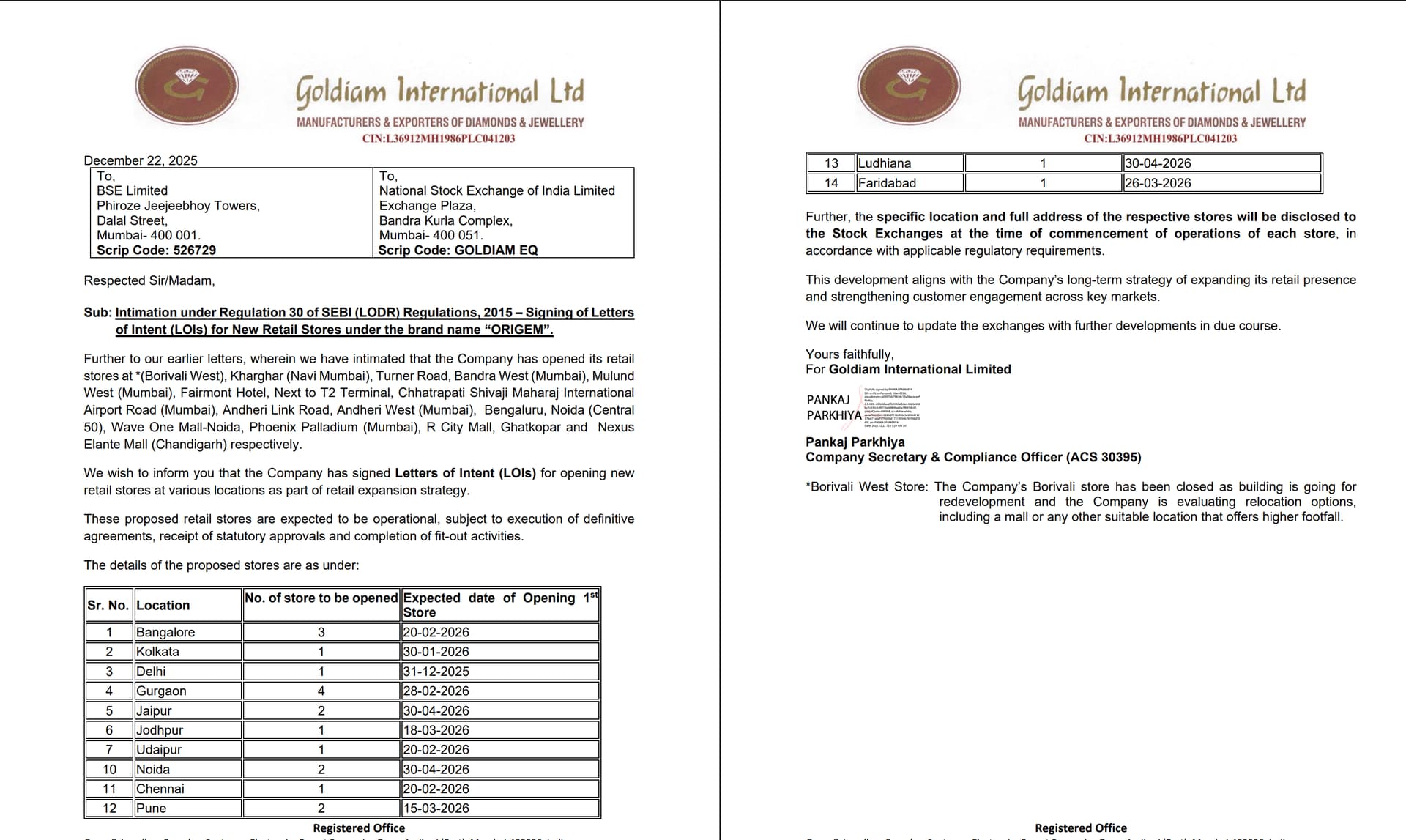

Just when they were about to reaching breakeven at their first store (Borivali West), the store is closed, whatever may be the reason, what cost implications can it have?

It will be very interesting to see the price point Titan tries to enter at - there is fairly high difference in per carat rates charged for LGD diamonds by various brands from 20k to 80k. Under their Pome brand (under Westside), the prices are on the extremely lower end (probably below 20k per carat).

On a separate note, a prestigious business house such as Titan entering in LGDs will end up helping the industry as there is still lot of confusion among customers with respect to authenticity of LGDs. With their behemoth marketing budgets, players like Titan can rapidly enhance the education about LGDs. Interesting times ahead.

Announcement of Titan’s entry in LGD space for sure going to expand overall LGD industry size. For Titan, it may be another new growth area specially when Gold Prices have sky rocketed and there could be (if any) some moderation in Gold Jewelry demand.

But with deep pockets, strong brand recall, consumer trust, country wide distribution network → Titan can make life (business profitability wise) difficult for other LGD players.

Yeah that is when big players get in FOMO too. Read somwehere (may be concall or CEO’s interview) and he was utterly bearish on LGD’s. Curious what made change their stance?

On a serious note, Titan in their concall mentioed that the people who are buying LGD are people who hve bought naturals earlier and are now experimenting. The only people this might affect are first time buyers perhaps.

Short summary of the Goldiam International Q3 FY26 updates,

Strong Financials: Revenue grew by 18% and net profit increased by 37%, supported by a ₹500 crore cash reserve and a dividend declaration.

Tax Strategy: The company maintains high margins by casting jewelry in the US, which allows them to bypass import duties by labeling products “Made in America.”

New Competition: Titan has entered the lab-grown diamond market with its brand “Beyon,” offering significantly lower prices per carat than Goldiam. To stay competitive, Goldiam is introducing lower-priced 9-karat gold jewelry and entry-level diamonds while expanding its footprint into the Middle East and Europe.

Retail Challenges: Their retail brand, Origin, saw an operating loss this quarter due to the high capital required to stock inventory for new store openings.