Godrej Properties has expanded its land bank with the acquisition of a 90-acre plot in Khalapur, Maharashtra. The company plans to develop approximately 1.7 million square feet of residential plotted development on this land.

1 Like

Hi,

does anyone here understands how cash collection doesnt relate with Revenue in P&L statements of real estate companies?

For example, as stated cash collections here in the Q1 FY25 investor presentation, it stands at 11436 Crores:

So, my mind makes sense that Revenue for the period has to be more or equal to 11436 Crores as this is the money coming in. But strangely, revenue is as follows: 3036 Crores (taken from screener.in)

Revenue is like 1/3rd of cash collections. And even lesser to bookings. So what parameter actually adds up to the top line in a company like this?

If anyone understands the industry/accounting wizardry here, do enlighten please!

This would help in understanding what variable to exactly track. As right now, if we track cash collections, guidance seems to be 31% growth. But if that doesnt relate to same growth in topline/bottom line, then its wrong variable being tracked.

1 Like

Real estate cos in India follow contract completion method where revenue gets recognised when the project is completed and handed over. Earlier it used to be % completion method but they changed the accounting. Therefore, reported topline is historical and an academic figure.

2 Likes

Thank you for this insight ![]() @bheeshma . So what variable, according to you, is best to track? Cash Collections, Booking value, or something else?

@bheeshma . So what variable, according to you, is best to track? Cash Collections, Booking value, or something else?

Just want to know a variable that I can track that gives me confidence that topline will eventually be grown to same degree as this variable. As guidance seems to be lacking over revenue or PAT, but seems abundantly and transparently displayed on above stated variables.

If you are looking at financial statements then operating cash flow less interest is the most reliable number to assess the health of the co as good cos generate good cash flows. For reasons not very clear to me interest expense is part of cash flow from financing even though it’s a part of business operations so you will have to take that out from there and deduct it from CFO.

Book value is also a good proxy but some of the figures on the balance sheet are hard to understand so the simpler way is to rely on cash flows

Pre Sales number and average realisation in Rs per sqft that is disclosed in investor presentations is what everyone tracks and gives a good sense of what’s happening in the co

2 Likes

Thank you @bheeshma for the insight. I’ll follow the guidance.

I’ll be tracking these numbers going forward. I have put up following in my notes.

Once again, Thank you for patiently answering my queries and helping out!

1 Like

I see below management Risk with GPL Need to investigate few :

- Defence Ministry Red Flag: The Ministry of Defence has raised objections to GPL’s ongoing residential project in Kandivali, Mumbai. The project is located near the Central Ordinance Depot, and the Defence Ministry has asked GPL to suspend the project1. This has led to a decline in GPL’s share price.

- Money Laundering Allegations: The Enforcement Directorate (ED) has intensified its investigation into alleged money laundering related to a housing project. Several key individuals from GPL, including directors and officers, have been summoned for questioning2.

- Ongoing Legal Dispute: GPL is involved in a legal dispute with Orris Infrastructure over a payment of Rs 202 crore for land. The Economic Offences Wing (EOW) of Delhi Police has registered an FIR against GPL and its top executives

Links below :

1 Like

Thanks for bringing this to attention.

Discl. : Invested. Small Position.

Godrej Properties | Concall Highlights

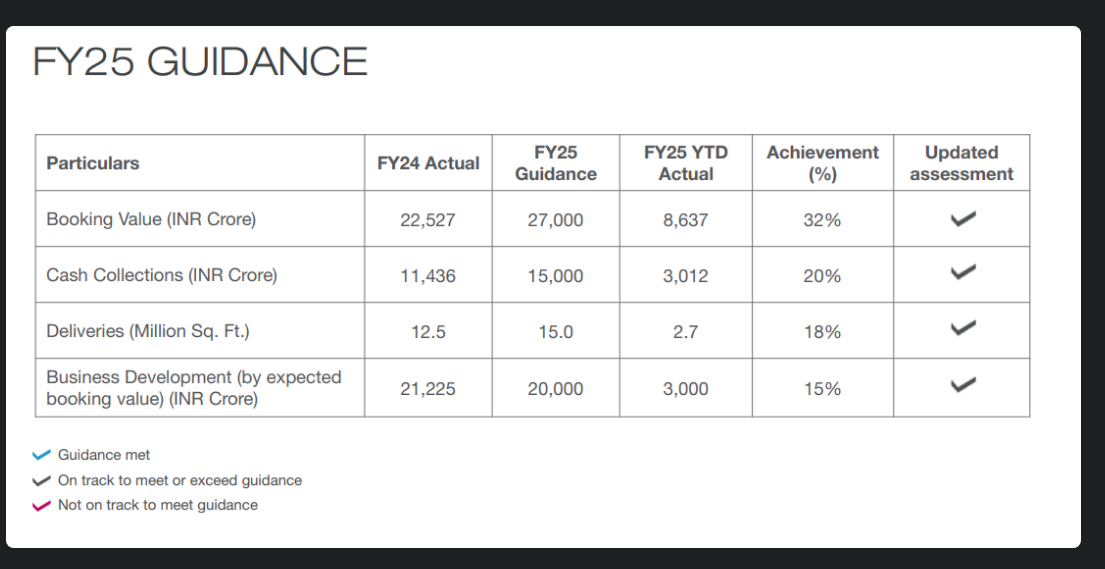

- Achieved 71% of FY25 booking value target; confident of meeting & exceeding full-year guidance.

- Initially targeted ₹20,000 Cr in new projects but has already added 12 projects with a ₹23,450 Cr booking potential.

- Confident in achieving guidance, backed by a strong Q4 track record & robust launch pipeline.

- Major Q4 launches planned, including a high-profile Sector 44, Noida project, expected to be a blockbuster launch.

2 Likes

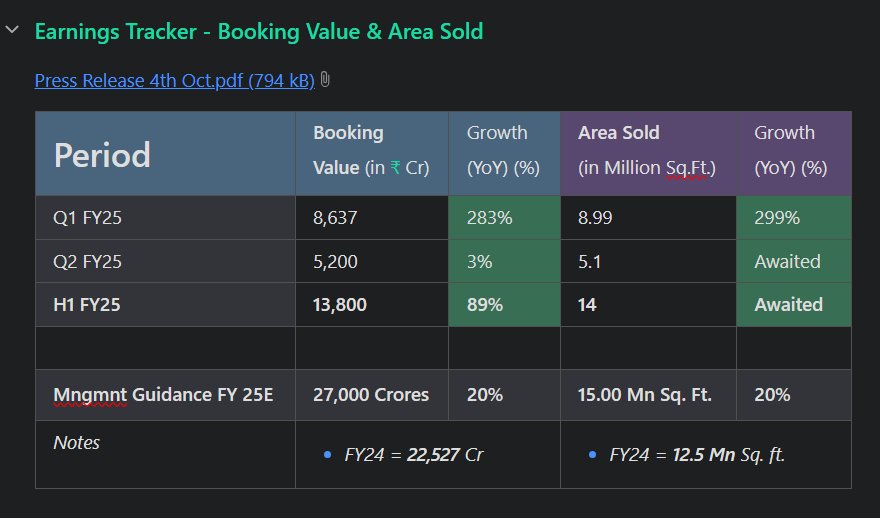

Godrej Properties have delivered another stellar quarter with bookings of 18.21 million sqft having value of 19281 Crores in the past 9 months.

I have updated my rough valuation calculations as per the current quarter results. Also reduced the forward PE from 25 to 20 as growth may slow down. Net Profit Margin is considered as 13.5% while the GP has committed to 15% in Concall. It seems to be trading at 12% discount to fair value.

- FY2025E Booking Value: 27000 Crores

- Pre-Tax Profit (18% of Sales): 4860 Crores

- Post-Tax Profit (75% of Pre-Tax Profit): 3645 Crores

- Expected MCap @ PE = 20: 72,900 Crores

- Current MCap (10-Feb-24): 64,000 Crores (2125/share)

Please note this is NOT a buy or sell advice. I am NOT a SEBI registered adviser.

2 Likes

What CMP have you taken for calculation of 12% discount to fair value?

Does any one has any idea - why the promoter group sold their share? I see a 12% decline from Sept 2024 to Dec 2024. Is it due to their low confidence in the stock and how are those funds being used?

1 Like

Hi Prashant,

The promoter did not sell rather they did a QIP issue.

Godrej Properties raised Rs 6,000 crore through qualified institutional placement (QIP) route by diluting nearly 8 per cent of equity. The issue price was Rs 2,595 per equity share, which was at a discount of Rs 132.44 (4.86 per cent of the floor price) to the floor price of Rs 2,727.44 per equity share. 2,31,21,387 equity shares were allotted to eligible qualified institutional buyers such as Singapore sovereign wealth firm GIC and SBI Pension.

Thanks,

Ranjan

2 Likes

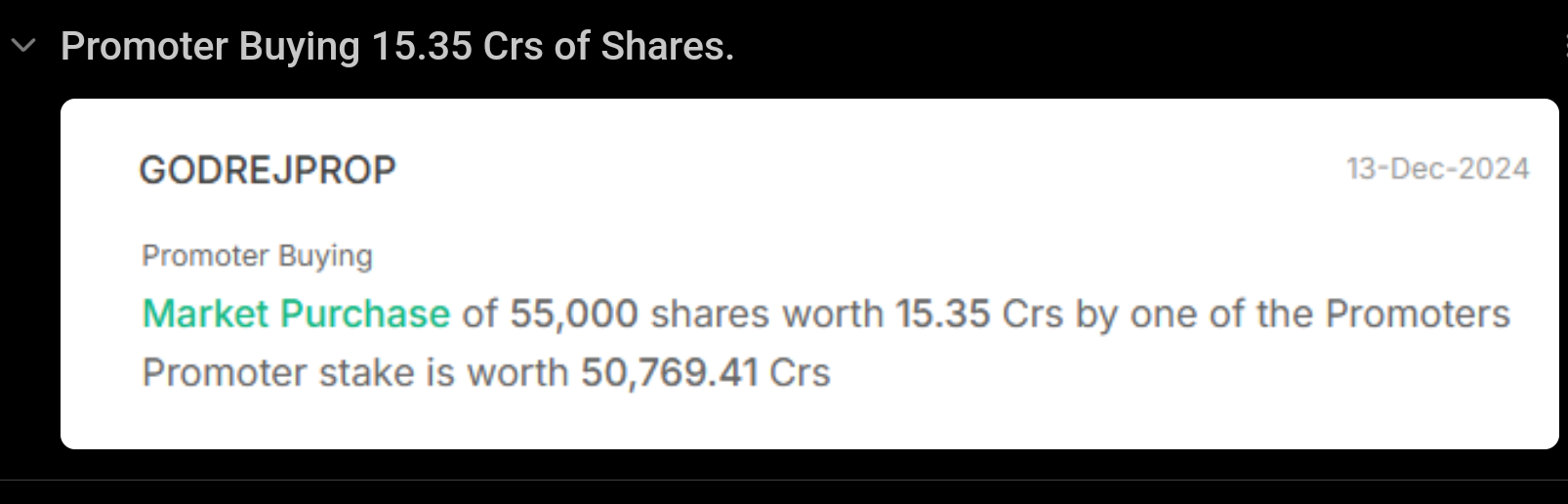

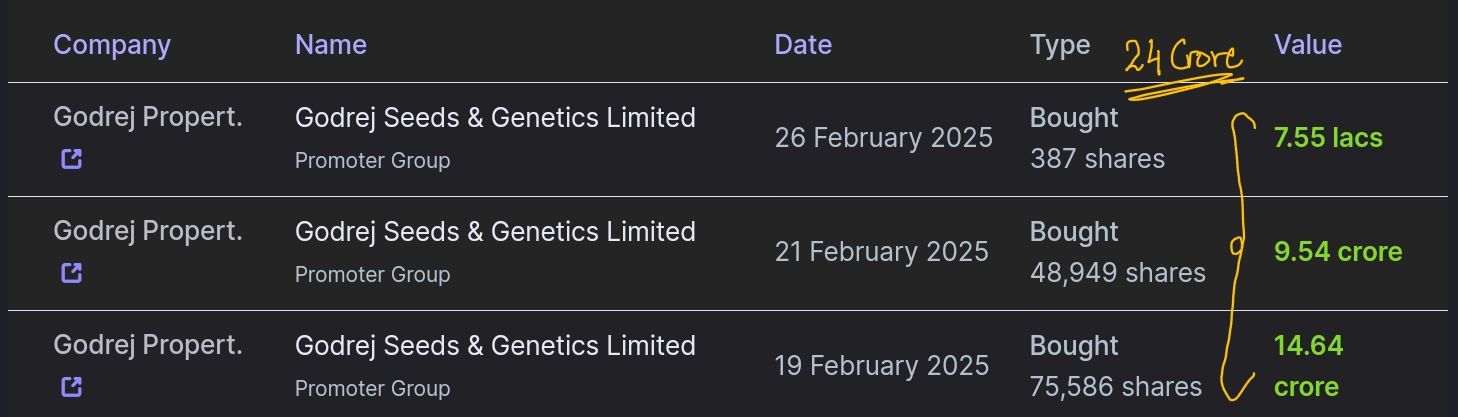

In Last 2 weeks, Promoter has done heavy buying. 24 Crores worth of buying.

And when I checked about Mutual Funds’ stance, they have bought too since the October High as seen below:

Addition to this, we know that

![]() Profits are rising every quarter when compared YOY

Profits are rising every quarter when compared YOY

![]() Management Guidance is 20% Growth in Booking Value

Management Guidance is 20% Growth in Booking Value

![]() In Last 3yrs & 5 yrs, EPS Growth > Price Growth.

In Last 3yrs & 5 yrs, EPS Growth > Price Growth.

![]() Stock is trading way below its Median PE

Stock is trading way below its Median PE

So it seems the safest bet to me right now amongst all stocks in my portfolio,

Disclosure: invested. Once booked profit at 3k price, entered again with an avg of 2.5K. Not a buy/sell recommendation.

2 Likes

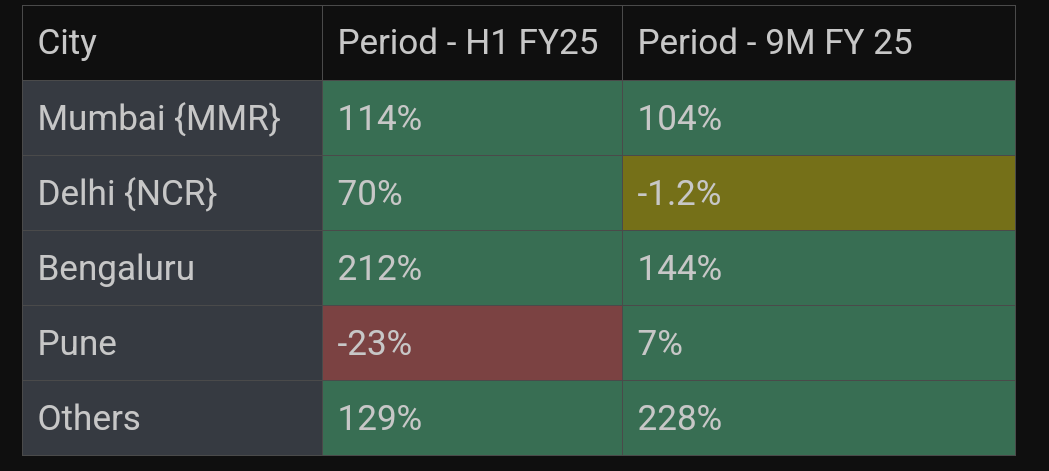

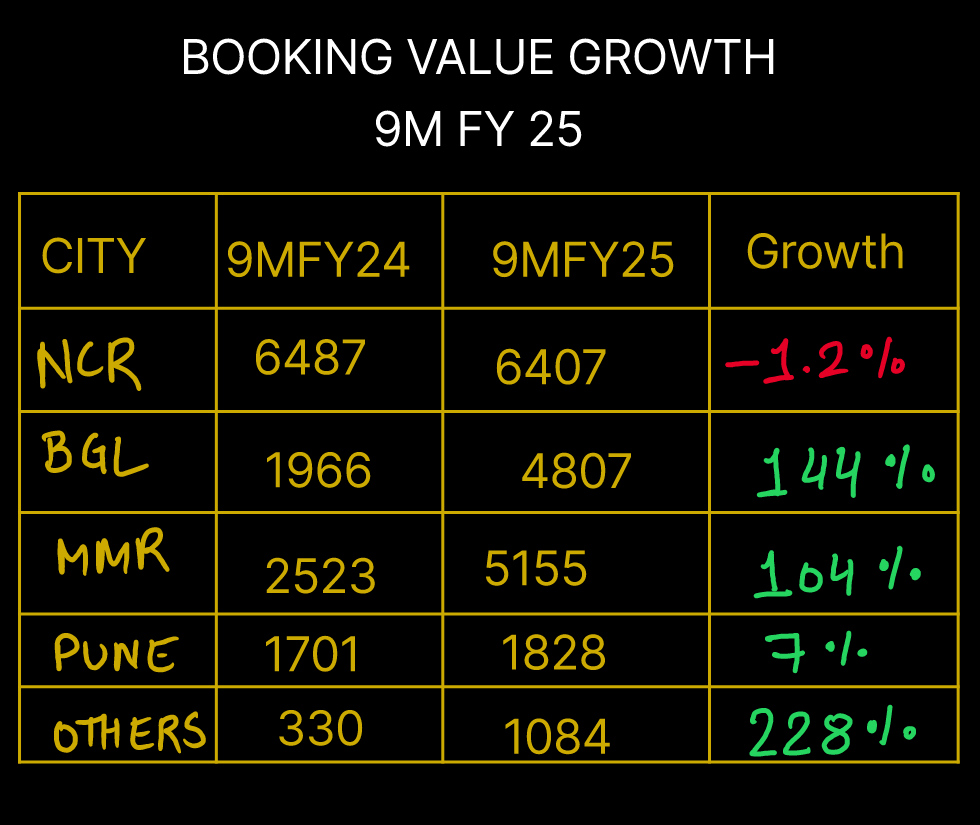

I did some city analysis for the Godrej properties and got some good Insights:

- The non core cities or Tier 2 cities have the fastest growth rate for the company. There is more than 3x growth in these areas in just 9M Fy25 over Fy24. From roughly 300 crore booking value to 1000 crore plus.

- Bengaluru is by and far considered the most attractive real estate market today where still there is a huge legroom for price appreciation compared to saturated market of Mumbai and NCR. And here the company is growing at roughly 2.5x rate which is phenomenal! From roughly 2000 crore booking value to 4800 crore plus.

- The saturated Mumbai (MMR) still had enough room for Godrej to grow in! The brand value must have been the biggest selling factor for Godrej in Mumbai. It is a market where competition of organised players in real estate is immense and yet Godrej is growing at 2x rate. Thats surprisingly assuring.

- NCR and Pune are pretty flat and seems to be a place where the growth is missing for now.

H1 and 9M analysis

Numbers of 9M

Others include non core cities -

Chandigarh, Nagpur, Indore, Kochi, Hyderabad, Kolkata, Ahmedabad & Chennai

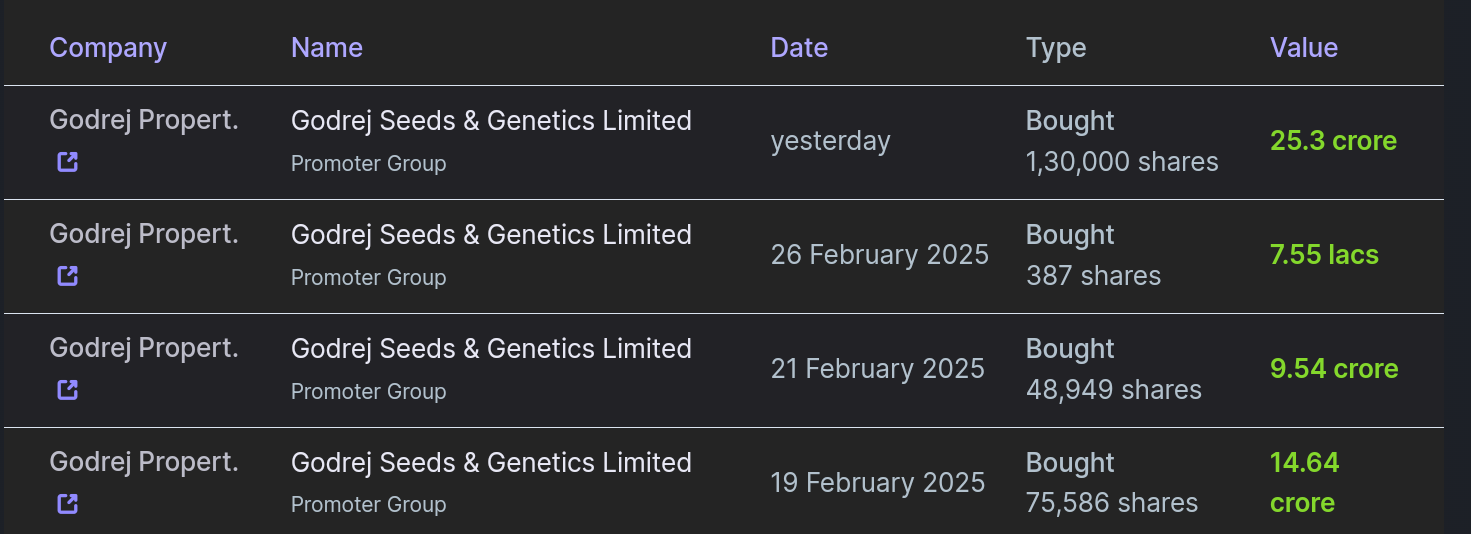

Promoter again bought shares worth 25 Crores.

Discl: Invested. Increased my investment recently from small portion of portfolio to not so small portion. Not buy sell recomm,

**

Update

**

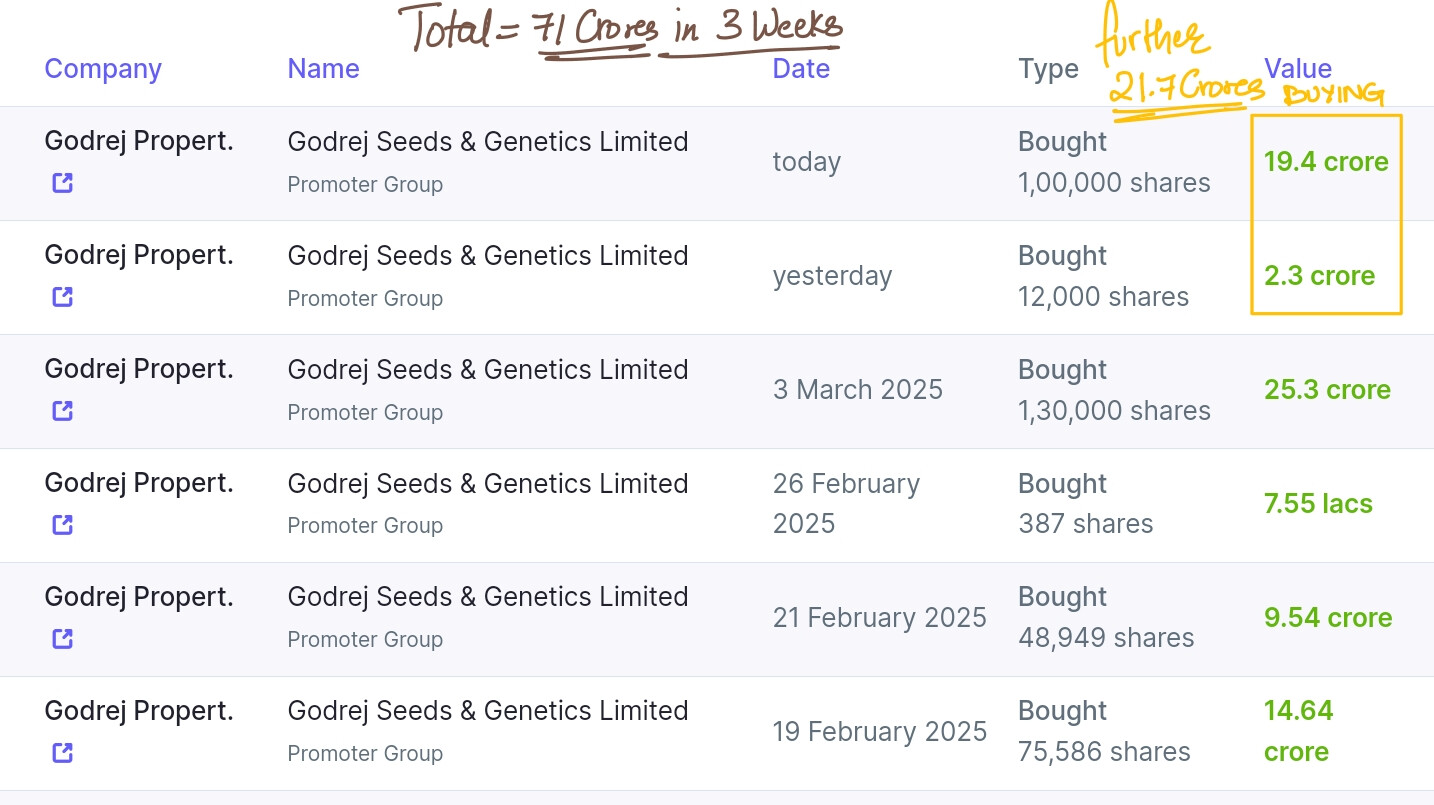

Further buying of 21 Crores, bringing the total to 71 crores of buying in 3 weeks.

PS: if they bought again, I wont be able to post in this thread! Cause valuepickr prevents more than 3 consecutives posts. :D Someone just react to these news so that we can track. :D

2 Likes

Where can i check the monthly shareholding data?

Which website or source you use for this information?