They said this is a flagship project in Bangalore and now EC stands cancelled. When I had looked closely in 2018 I wondered how could this be approved even. They also dumped debris in the lake catchment area.

Godrej Properties acquired prized land in very Good consideration.

Payment for acquisition in phased manner, so Cash Flow will be taken care.

Great Co in the Business

hi All

Godrej Properties has been a fairly tough company to understand since real estate, with its multi year development and payment cycles, is not amenable to conventional accounting disclosures. I have tried to look at the company from various vantage points and below are my observations –

- Most important metrics

Since revenues are booked only on completion of projects, the accounts are almost 3 years behind the actual construction and selling since receipt of cash starts from launch itself, in which case the investors tend to look at the square feet booked and the value of bookings –

| Particulars | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| msf Booked | 1.38 | 3.2 | 2.4 | 4.1 | 2.82 | 3.9 | n/a | 3.1 | 6.3 | 8.8 | 8.8 |

| Increase by | 132% | -25% | 71% | -31% | 38% | 103% | 39% | 0% | |||

| Bookings in Crores | 1,071 | 1,563 | 2,469 | 2,438 | 2,681 | 5,038 | 2,020 | 5,083 | 5,316 | 5,915 | |

| Increase by | 46% | 58% | -1% | 10% | 152% | 5% | 11% | ||||

| Realization per msf | 3,348 | 6,510 | 6,021 | 8,645 | 6,874 | 6,516 | 8,068 | 6,069 | 6,722 | ||

| increase by | 94% | -8% | 44% | -20% | 24% | -25% | 11% |

Following observations can be made –

- The company’s bookings in square feet as well as value have grown significantly in last 3 years on account of company’s focus on top 4 regions – Mumbai, NCR, Pune and Bangalore, along with aggressive launches.

- Bookings too have crossed 5,000 crores in the last 3 years on account of similar reasons. It is important to note here that changes in realizations per square foot for the company do not affect the fundamentals in any way.

The asset light joint development model, Godrej brand and quality execution have been some of the attributes of the company that have made it a significant value creator. But how does one determine whether the numbers fit this narrative or not.

So I started looking at the cashflow statement in order to determine how much free cash the company has generated –

| Particulars | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | Total |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Cash from Operating Activity | -342 | -445 | -1,226 | 121 | -689 | -941 | 490 | -566 | 1,156 | 479 | -230 | -2,193 |

| Int. Received | 72 | 15 | 11 | 12 | 9 | 10 | 20 | 72 | 87 | 130 | 80 | 518 |

| Interest Paid | -66 | -4 | -2 | -7 | -4 | -5 | -408 | -312 | -298 | -295 | -301 | -1,702 |

| Net OCF | -336 | -434 | -1,217 | 126 | -684 | -936 | 102 | -806 | 945 | 314 | -451 | -3,377 |

| Capex | -7 | -24 | -22 | -21 | -61 | -12 | -24 | -9 | -150 | -74 | -67 | -471 |

| Acquisitions | -6 | -192 | -162 | -3 | - | -773 | -547 | -796 | -2,478 | |||

| Disposals | 39 | 0 | 41 | 2 | 201 | 0 | 283 | |||||

| Proceeds from Shares | 429 | - | 460 | - | 694 | - | - | 35 | 3 | 1,000 | 2,066 | 4,687 |

| Debt Adjustments | -20 | 235 | 1,142 | -408 | 914 | 902 | -98 | 611 | -197 | 265 | 208 | 3,554 |

| Dividend | -15 | -28 | -36 | -27 | -36 | -40 | -40 | - | - | - | - | -222 |

As can be seen from total column above, the company has not generated any free cash over the years, but has relied significantly on diluting its equity to grow its business. Even interest payments in most years has been paid on by taking even more debt.

While it can be argued that the working capital of the business is bound to be stressed as projects near completion and the company is increasing its launches, it can be equally argued that the cash received from buyers at the launch and later, ought to be adequate to cover it.

With the cashflow statement being the ultimate indicator of a company’s operations, and the same being unsuitable for us to analyse due to the company being in high growth phase, I moved on to the Income Statement.

Till 2018, the company recognised the costs and revenue on % completion basis, after which it moved to completed contract method due to regulatory requirements. Despite its long term stated target 35-40% EBITDA margin, the company has not delivered the same in any of its last 10 years –

| Particulars | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Revenue | 243 | 452 | 770 | 1,037 | 1,179 | 1,843 | 2,123 | 1,583 | 1,604 | 2,817 | 2,441 |

| increase by | 86% | 71% | 35% | 14% | 56% | 15% | -25% | 1% | 76% | -13% | |

| EPS | 8.8 | 9.4 | 6.3 | 8.9 | 8.0 | 9.6 | 7.4 | 9.6 | 4.0 | 11.0 | 10.6 |

| increase by | 7% | -33% | 41% | -9% | 19% | -23% | 29% | -58% | 175% | -4% | |

| Book Value | 58.5 | 65.3 | 92.4 | 91.5 | 90.5 | 92.6 | 83.0 | 92.6 | 55.9 | 107.7 | 190.6 |

| increase by | 12% | 42% | -1% | -1% | 2% | -10% | 12% | -40% | 93% | 77% | |

| EBITDA | 7% | 23% | 21% | 28% | 24% | 14% | 6% | 16% | 0% | 6% | 14% |

| EBIT | 6% | 22% | 20% | 27% | 23% | 13% | 6% | 15% | -14% | 6% | 13% |

| PBT | 67% | 45% | 26% | 28% | 29% | 18% | 11% | 18% | 7% | 12% | 17% |

| Tax rate | 24% | 30% | 35% | 32% | 32% | 28% | 30% | 27% | 26% | 27% | 45% |

| PAT | 51% | 29% | 13% | 13% | 14% | 10% | 8% | 13% | 5% | 9% | 10% |

Not only have the margins been below LT target, its EPS has remained rangebound on account of continuing dilutions. I have not looked at the Balance Sheet ratios on account of large Securities Premium in the Balance Sheet as well as bulk of the company’s value coming from future projects.

However, the company has made a lot of adjustments directly in the net worth, as can be seen from below –

| Particulars | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 |

|---|---|---|---|---|---|---|---|---|---|

| Opening Net Worth | 747 | 842 | 1,365 | 1,351 | 1,694 | 1,747 | 1,687 | 1,896 | 1,102 |

| Profits | 98 | 138 | 159 | 191 | 160 | 207 | 87 | 253 | |

| New Issue | 451 | 671 | 4 | 4 | 990 | ||||

| ESOP trust / Amalgamation Adjustments | 10 | -122 | -427 | -138 | 133 | ||||

| AS 115 Impact | -880 | ||||||||

| Dividends | -27 | -36 | -47 | -47 | -48 | ||||

| Others | -9 | 6 | -13 | 43 | -309 | 2 | -0 | 9 | |

| Closing Net Worth | 842 | 1,365 | 1,351 | 1,694 | 1,747 | 1,687 | 1,896 | 1,102 | 2,354 |

As can be seen from above, losses above include losses on amalgamation written off over the years directly from networth. These losses include the exit given to PE players who had invested in the individual projects and construe financing costs and should have formed a part of P&L account. Further, amount of 880 crores in 2018 is one time adjustment on account of the company moving to completed contract method. This assumes a lot of importance since the profits booked by company from 2010 to 2018 are 1,294 crores , 68% of which are reversed.

Further, 309 crores written off in 2016 are on account of restatement of accounts in 2017, details of which I was unable to locate.

Further, gain of 133 Crores in 2016 is not a gain since it represents consideration paid through shares for taking over a group company JV. Instead of booking the purchase at the market value of shares issued, the company has booked a profit by accounting for shares issued at the face value (8% of share capital was diluted)

This was also discussed in one of the calls going all the way to 2013, wherein the management did not give an adequate response –

Analyst: So how are you accounting for those assured exits, for example isn‟t the PAT over stated due to non-recognition of your effective financing cost because effectively your PE deals I understand from the industry is at around 17% to 18% assured return exits to a lot of the PE Funds. Last year also even despite a reported profit of about Rs. 140 crores your effective net-worth is actually down in FY13 over FY12, so is that because you are accounting for, is it fair to assume that Rs. 150 crores is the amount of effective financing cost that you have borne on account of assured returns to these PE exits because that is the amount by which your net worth is actually effectively gone down?

V. Srinivasan In all these subsidiaries, essentially it is checked for impairment and only along with the return if the value of the project is lower than that you need to provide for the impairment. So it is not correct to say that we are not expensing it out, the project is able to bear these kind of costs and as far as the net worth reduction is concerned which you said about Rs. 122 crores as we have mentioned in the notes to the account has been adjusted on account of this scheme of amalgamation which is approved by the court.

Source: Q4 2013 Concall Transcript

It would be wonderful to have forum views here. Thanks!

Discl: I am not a SEBI registered analyst nor is this a Buy / Sell recommendation. Pls do your due diligence before taking a call.

11 Likes

Good analysis.

Here is the presentation for Q4FY16 which has FY16 booking area as 4.32m sqft on page-20: https://d1jys7grhimvze.cloudfront.net/backoffice/data_content/investors_event_presentation/results_presentation_q4_fy_2016_invp.pdf

I remember another analyst calling the PE investments as quasi-debt around 2012-13.

I think you should add the year-wise business development, launches and the delivery in million sqft to the above booking data to get a clear picture of how the company is executing on its plans/promises.

1 Like

Conference call takeaways

Strong Business Development-led outflow expected for H2FY21 – to be funded by debt.As a result,

net debt to increase by Rs20bn and net debt/equity torise and stabilise around 1x; this is inline

with our expectation,highlighted in ourCOVID-19 company update report(Click here).

Collections to improve in H2 FY21.

H2FY21 expected to see a couple of launches

Bandra and Worli projects delayed; to be launched in FY22 (expected).

Ashok Vihar project to be launched by Q4FY21/Q1FY22.

Expects to adhere to launch pipeline timelines during FY21; H2 may see better launches.

Incremental business developments to be undertaken primarily in Bangalore followed

by MMR and NCR.

GPL will explore ‘plotted development’ opportunities across geographies.

Key projects – Ashok Vihar, Bandra, and Worli – have made progress; in approval/preplanning stages.

https://www.hdfcsec.com/hsl.docs//Godrej%20Properties%20-%20IC%20-%20HSIE-202011262336359868764.pdf

Godrej Properties Ltd (GPL) is a sectoral bell-weather with an innate capacity to build homes. Over the years,it has metamorphosed into a seamless home manufacturing machine with the shortest production time from land acquisition to approvals to launches and sales. In this journey,it has gained market share and emerged a crucial challenger in the respective micro-markets;it is on its way to becoming a leader. Given strong brand, robust financial capacity and strong execution capabilities, landowners/Tier 2 developers have been partnering with GPL for JV opportunities. The growth journey is expected to crystallise further with the regulatory landscape changing over the years, in favour of organised developers. We believe GPL only constrains itself,and that is its biggest strength or weakness. … we initiate coverage on the stock

1 Like

-

Finally Real Estate cycle starting to turn,affordability is good and demand has picked up.

-

Inventory levels are low,very little new supply coming up.

-

Maharashtra Stamp Duty Cut being time bound forced the customers who were on the fence.

-

Sector is very important for employment and economic growth.

-

Sector is extremely fragmented(10000+ players) and consolidation will happen in favor of leading developers.

-

High commodity prices a concern but will mean demand uptick and ultimately passed on to customers.

-

Timing of launches linked to regulatory approvals

-

Price hikes are long overdue.

-

Have hiked prices in some projects where demand is strong.

-

Expect pricing to improve significantly in the next couple of years.

-

Added 50-60 Million Sq ft of space to the portfolio in the past 2 years when industry was in distress.

-

Looking at strong sales and net cash flow generation.

-

W.r.t Commercial real estate the jury is still out but in 3-5 years expect it to do well.

-

Have dynamic strategy for projects:

If land prices are low we would like to acquire land like in the past 2 years and

If land prices go up then we will look at Joint Development model which is less capital intensive.

2 Likes

Godrej Properties Q3 FY21 Con Call Highlights

- Total value of Booking stands at 1488 Cr., up 25% on y-o-y basis and 35% on q-o-q basis. This is achieved through a Sales of 2236 homes with a total area of 2.4 msf.

- Cash Inflow of 1257 Cr. and Net Operating Cashflow of 445 Cr.

- Total Revenue – 306 Cr., Adjusted EBITDA – 96 Cr., Net Profit – 14 Cr. (All the reported sale numbers are net of any cancellations)

- Collections significantly higher than previous 2 qtrs.

- On Operations side, delivered 1.3 msf across 2 projects in the quarter.

- Govt. extended benefits on Affordable Housing by one year to boost real estate sales

- Maharashtra Govt reduced Stamp duties and premiums

- Project wise details:

a. At Godrej Hillside 3 in Pune, we sold 500,000 sq. ft., which is approx. 85% of the released inventory, with a booking value of 312 Cr.

b. Godrej Retreat, which is the first ever project in the Faridabad mkt., we sold 490,000 sq. ft., which is more than 95% of the released inventory, with a booking value of approx. 279 Cr.

c. At Godrej City in Panvel, we sold 370,000 sq. ft. with a booking value of 244 Cr. in the launch quarter - 12 projects lined up for launch in the coming quarter. If all 12 launches happen(quite unlikely), this would translate to the Highest ever sales in a quarter and further, lead to the highest ever annual Sales as well. However, even with a lower launch, the next quarter’s sales can contribute significantly to beat last year’s overall sales.

- Added 2 new residential projects with saleable area of 4.1 msf in Bangalore. Both are outright purchases of land. Breakup: Sarjapur project – 1.6 msf and Whitefiled project – 2.5 msf

- Expects the year ahead to be the Best ever year for the company across all operating metrics

Analyst Questions: - Price Increase due in the sector? – Yes, price increase likely in the next leg, now since demand has picked up, and company has looked at certain projects for such a price increase. However, no significant price hike, holistically, has taken place q-o-q for Q3.

- Have we crossed double digit mkt share? – Mkt Share has risen but Not yet in double digits. This will be likely due to mkt growing overall and consolidation gaining steam.

- Demand Drivers – Interest rates low, thus creating affordability and lot of pent up demand, Govt. initiative and new demand due to home preference caused by the pandemic

- Sustenance Sales Trend - Will be higher during the H2FY2021, driven by 4th qtr., as during new launches, the focus shifts to new sales which slightly impacts the Sustenance sales efforts.

- Capital Allocation – Sought Approval of Fund Raise 3750 Cr. Utilization will be to gain mkt share due to consolidation by maintaining sales momentum and heightened new business development.

- Revenue Recognition this qtr – Primarily from 2 Joint Venture projects - Godrej Air in Bangalore and Godrej 101 in NCR. Only Godrej’s share of profit gets reflected in the books as part of PBT.

- Approvals on New Launch Pipelines – Godrej Agrovet is in final stage for getting RERA Approval, Already received RERA Approval in Pune, final stage for getting RERA Approval for Godrej Encore project, Mumbai already launch Kalyan project-Phase 2, Approval for the Chandivili project within next 10 days, Sector 43 Noida project has a lot of approvals done and should be launched in Q4

- Mumbai QoQ highlights? – Comparatively less Launches in Mumbai; however good traction on Godrej RKS Mumbai project. Big launch this time was in Panvel where we have sold 244 Cr of inventory.

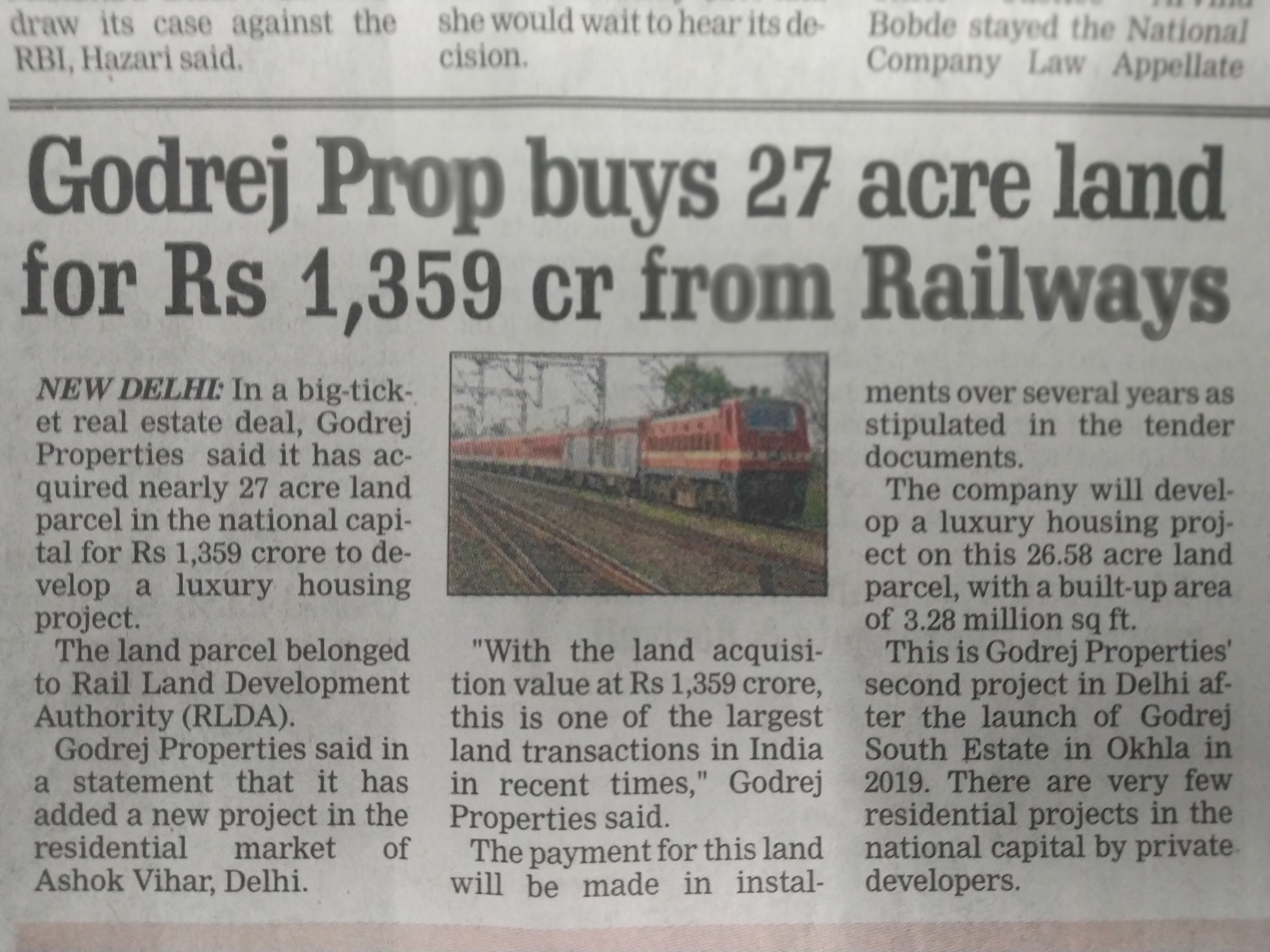

- Total Deferred Land Cost Liability for the entire portfolio? – Most of the outright land purchases have been paid; big deployment will be on the Ashok Vihar project to the tune of 1200 Cr. to be paid over the next 8 years.

- Updates on 3 biggest projects:

a. Bandra – Challenges with JV partners ongoing; however, capital exposure is pretty limited and return profile will be better with delays as with each delay, the share for Godrej will go up.

b. Worli(Slum Rehabilitation) – Designs are frozen and approval process is initiated; slums are 15% cleared. Launch in FY2022.

c. Ashok Vihar – Designs are done; fairly advanced stages of approval and hopefully the launch can be in Q1FY2022. - Strong emphasis on Digital sales – Backend fully automated and softlaunch of front end app has been done.

- View on Plotted Development opportunity – Big opportunity and quite attractive due to much shorter cashflow recovery cycle as compared to group housing; Will be a significant part of the group’s strategy over the next few years

- Construction Technology is a big differentiation and enables construction and sales to happen pretty fast; for e.g. precast technology, pre-built toilet set(instead of building it on site). This can save 6 months of construction time. However, not much infrastructure exists in India for the same; Godrej is trying to setup this infrastructure; however, constraints from the supply chain and contractor side.

- Operating Cash Flow - OCF Margin will be on an upward trajectory; Quarterly volatility will be there in Collections as Collections are connected with milestones(which are events led and not steady); Avg of last 10 launches will give an idea on OCF margins of new launches

- Hopeful to achieve significantly over 10,00 Cr. in annual sales over the next couple of years

- Hotel should start operations in FY2023; high likelihood to monetize this project later

- Collections Rate? – For new launches, it’s around 5-10% of initial money; for sustenance sales, it depends upon the stage of completion.

6 Likes

2 Likes

Spoke to a Real estate broker today who has a fairly decent size op in Mumbai.

-

Unbelievable demand in the residential real estate space.

-

Grade A developers only. That’s where most people are looking to buy from. Marquee developer projects are getting sold out in few months.

-

This time around a lot of the new demand is from salaried folks especially in IT or even otherwise. This was not the case before.

The low interest rates are the sweet spot nobody wants to miss. ( PS - These are floating rates, not fixed in case you’re planning).

-

One to 2.5 crores is the sweet spot in the MMR region.

-

Banks are refusing to fund Tier 2 builders. Nobody wants to work with them after the last cycle in which many defaulted and exited the system.

-

Mumbai based/ focused developers to benefit in a big way in this upcycle as ~ 20% - 25% of India’s unsold inventory is in Mumbai.

The biggest cost in a RE project is land and not the construction cost.

Grade A developers who had acquired land especially in 2018 - 19 will benefit in a big way.

However there are 2 Big differences in this new cycle which makes things more Interesting.

The last two cycles in Real Estate were - 1994 - 1999 and 2004 - 2009

Both cycles had one Common Point -

Both started and rose sharply because of External Investments.

India allowed NRIs to invest in India RE ~ 1994 and a lot of PE money came into real estate post 2004.

What this sudden gush of money caused is a very sharp increase in supply and land prices which were not sustainable.

Things became so crazy that at the peak of the last cycle - Land prices went up 5 times in 2007 alone.

What Makes this cycle much more Stable is ;

A - RERA has killed the cycle of unethical builders taking money for one project, diverting it into other deals and not delivering either on time. This has led to a lot of consolidation and only Grade A Developers can do multiple projects and gain Market share.

B - This time around the capital coming is smart capital - Domestic Real estate funds, much more Internal accruals from Grade A Developers rather than debt.

Both these points - Limited number of developers and Smart capital ( Low debt levels) make the current cycle much more sustainable.

From a markers standpoint, this is definitely a cycle one shouldn’t miss.

PS: Please do due diligence!

9 Likes

After announcing Rs 700 crore deal with a controversial (shady?) firm, Godrej has suddenly called off the deal, apparently worried by the negative reaction from stock market. How times have changed!

One wonders what Mr Godrej was thinking in this case. When you have a trusted brand and reputation that has taken years to build, you can not just associate with questionable characters, get into “rough & tough” segment of the market in pursuit of growth, and not expect collateral damage. Hope management of every company takes note.

2 Likes

Very aptly said a reputation built over years tarnished in a moment of madness

That apart the market reacted to what was perceived as a FUNDAMENTALLY ADVERSE change in business model, from an asset light developer with fast throughput and cashflow to an asset heavy builder, undifferentiated from the others out there, with concomitant decline in ROE and ROCE and ergo lower discounting

1 Like

The DB Realty fiasco gave a good opportunity to long term investors to enter this scrip at reasonable valuations. It is up 90% from the March lows. The good thing about Godrej Prop is that they called of there deal when they realized it was a mistake. They were not adamant about the same.

Also I like the way they are dealing with the faulty construction issue in Godrej Summit where they are buying back the apartments if the occupants are not confident on GP to resolve the problem. I don’t recollect any RE Co doing the same.

GP has solid land bank to last another three years at the current run rate. As a result they do not require to buy land at exorbitant prices to meet the demand.

Moreover, they have launched their own facility management subsidiary (Godrej Living) like Ashiana Housing to get feedback from users.

GP seems to be trading at fair value as per my back of the envelope calculations -

- FY2024E Bookings: 170.00 lsf

- per Sq Ft Rate: 8000.00

- Saleable Value: 13600 Crores

- Pre-Tax Profit (18% of Sales): 2448 Crores

- Post-Tax Profit (75% of Pre-Tax Profit): 1836 Crores

- Expected MCap @ PE = 25: 45,900 Crores

- Current MCap (08-Dec-23): 53,665 Crores (1930/share)

Please note this is NOT a buy or sell advice. I am NOT a SEBI registered adviser.

1 Like

Godrej Properties have delivered another stellar quarter with bookings of 4.34 million sqft having value of 5720 Crores.

I have updated my valuation calculations as per the current quarter results. It seems to be trading at slight premium to fair value.

- FY2024E Bookings: 160.00 lsf

- per Sq Ft Rate: 10000.00

- Saleable Value: 16000 Crores

- Pre-Tax Profit (18% of Sales): 2880 Crores

- Post-Tax Profit (75% of Pre-Tax Profit): 2160 Crores

- Expected MCap @ PE = 25: 54,000 Crores

- Current MCap (09-Feb-24): 62,750 Crores (2257/share)

Please note this is NOT a buy or sell advice. I am NOT a SEBI registered adviser.

1 Like

I think you can’t allocate all the profit from these sales to GPL, only for the ones where they own the land. For other sales they get a portion of the profit, the rest is shared with the land owner.

On the other hand, they are building a commercial portfolio(example: Godrej One & Two) which will give them a steady stream of income.

Their TTM(last 12 months) booking stands at Rs17,059 Crores. FY24 booking value should be higher than this, judging by their recent(Q3) con-call.

And they have been saying that the new launches have a higher margin profile.

Disclosure: I am NOT a SEBI registered adviser. This is NOT a buy/sell recommendation. I am invested & biased!

I agree with you that the bookings include JVs as well as projects where GP is development manager. However, this is just a back of the envelope calculation to arrive at a rough fair value. I tend to purchase only when there is at least 20% margin of safety.say at a MCap of 43,000 Cr (1550/share).

Having stated the above, if one has got the purchase price right, GP is a hold for the next years and a half at a minimum. I believe there will be surplus inventory in 2 years.

Please note this is NOT a buy or sell advice. I am NOT a SEBI registered adviser.

1 Like

Defence Ministry points gun at Godrej’s housing project with revenue potential of Rs 7,000 crore in Mumbai

Read more at:

Godrej Properties Q1 FY2025 Analysis: Key takeaways!!

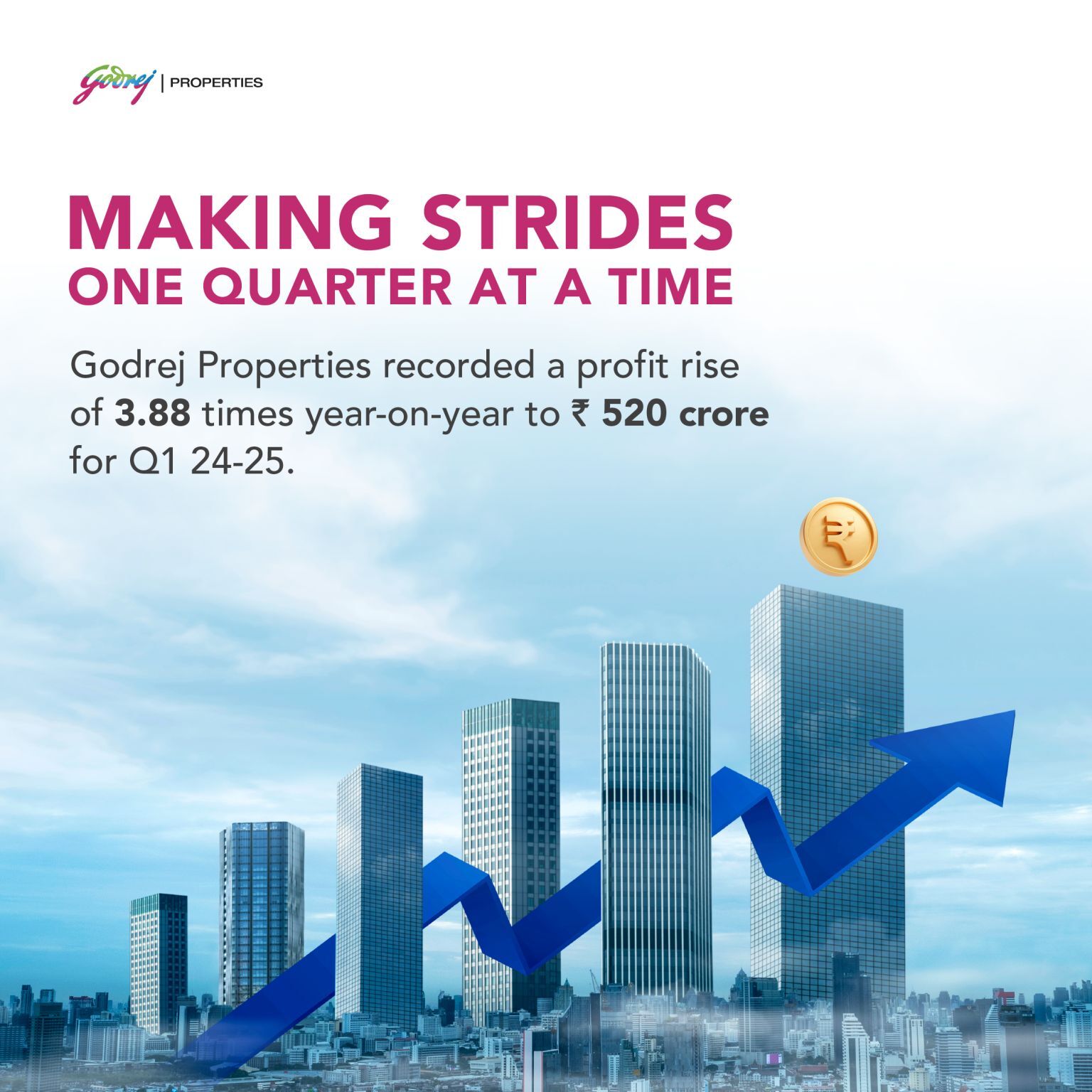

Godrej Properties delivered an exceptionally strong Q1 FY2025, with multi-fold growth across key metrics. The company achieved its highest ever quarterly net profit of INR 520 crores. Booking value grew by 283% year-over-year to INR 8,637 crores, while booking volume reached 8.99 million square feet - the highest among listed developers in India. Management is confident about maintaining this growth momentum through new project launches and strong sustenance sales.

Strategic Initiatives:

- Focus on premium locations and mid-sized projects (10-15 acres) to drive higher returns

- Standardization and centralization of procurement for key materials to achieve economies of scale

- Mix of top contractors for large projects and trusted partners for mid-sized developments to ensure timely execution

- Expansion into plotted developments as a complementary offering, targeting 10-15% of overall sales

- Continued emphasis on business development to replenish rapidly selling inventory and fuel future growth

Trends and Themes:

- Strong demand across key markets, especially for projects by reputed developers

- Price appreciation in most markets, with potential for further increases in some regions like Pune

- Consolidation in the industry favoring organized players with strong brand equity

- Growing importance of end-user driven demand for sustainable sales

Industry Tailwinds:

- Robust economic growth and rapid urbanization driving structural demand for housing

- Low mortgage rates supporting affordability

- Increasing preference for home ownership post-pandemic

- Government focus on housing and infrastructure development

Industry Headwinds:

- Potential cyclical downturn in the medium term (4-5 years)

- Rising input costs impacting margins

- Regulatory challenges and approval delays in some markets

Analyst Concerns and Management Response:

- Execution capabilities given rapid sales growth: Management highlighted investments in engineering capabilities, strong contractor relationships, and a site-head operating model to ensure timely delivery

- Gearing levels: Company comfortable with current gearing (0.71x), expects strong operating cash flows to support growth

- Project delays (e.g. Ashok Vihar): Management acknowledged delays but emphasized enhanced returns due to price appreciation; confident of launch by Q4

Competitive Landscape:

Godrej Properties has emerged as a leader among listed developers, achieving the highest quarterly booking value for two consecutive quarters. The company’s brand strength, execution track record, and financial capabilities are allowing it to gain market share in a consolidating industry.

Guidance and Outlook:

- FY2025 booking value guidance of INR 27,000 crores

- Collections guidance of INR 15,000 crores for FY2025

- Embedded margins slightly higher than FY2024 levels

- Expect strong business development momentum in Q2 FY2025

Capital Allocation Strategy:

- Maintain gearing in the range of 0.5x to 1x

- Focus on high-quality land acquisitions in top 4 markets (Mumbai, NCR, Bangalore, Pune)

- Open to larger land parcels if returns are attractive

- Potential for equity raise if valuation is favorable and growth opportunities exceed internal accruals

Opportunities & Risks:

Opportunities:

- Market share gains in consolidating industry

- Expansion into new micro-markets within existing cities

- Potential for margin expansion through price increases

Risks:

- Cyclical downturn in real estate market

- Execution challenges in rapidly scaling business

- Regulatory hurdles and approval delays

Regulatory Environment:

The company faces some regulatory challenges, such as the ongoing approvals for the Ashok Vihar project and recent issues with the Chandigarh commercial project. Management is confident of resolving these issues but acknowledges the potential for delays.

Customer Sentiment:

Strong customer response to new launches, with projects like Godrej Woodscapes (Bengaluru) and Godrej Jardinia (Noida) achieving record sales. High collection efficiency (94%) indicates positive customer sentiment and financial ability to honor commitments.

Top 3 Takeaways:

- Record-breaking sales performance with INR 8,637 crores booking value in Q1 FY2025, positioning Godrej Properties as a leader among listed developers.

- Strong execution capabilities and strategic focus on premium locations driving growth and profitability.

- Robust business development pipeline to sustain growth momentum, with potential for market share gains in a consolidating industry.

3 Likes

Godrej Properties secures prime land in Greater Noida:

The company has emerged as the top bidder for two land parcels in Greater Noida, with a combined bid value of Rs 842 crore. This acquisition will add ~3.75 million sq ft to its development pipeline and has the potential to generate over Rs 5,000 crore in revenue.

This move strengthens Godrej Properties’ presence in the NCR market.

1 Like