Can anyone help me understand that why NMDC, GPIL are falling even though iron ore prices are increasing sharply worldwide?(Indian market corrected till yesterday but today there is a rebound but still iron ore stocks are falling).Today the iron ore price is hovering around 112$ level. Is there any other angle which I am missing?

1 Like

Still no sign of fiscal stimulus from China—just the same old policy statements being repeated.

4 Likes

Could be the lingering effect on retrospective tax rule?

2 Likes

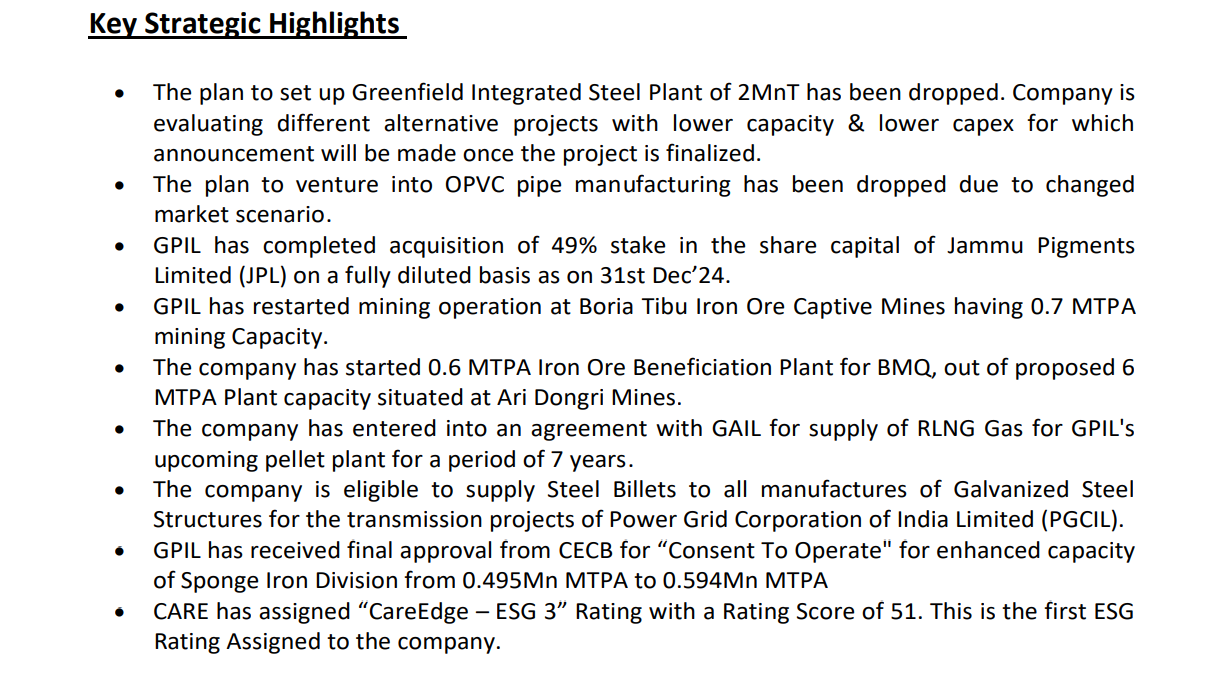

In a recent filing to the stock exchanges, Godawari Power communicated about 2 new line of businesses which are non-core to mining, iron and steel industry

-

Setting up a separate unit to manufacture oPVC pipes. This is a commodity business with cut throat competition from established players like Supreme, Astral, Prince, Hindware with a good brand recognition.

-

The proposal to acquire up to 60% equity stake in R. G. Pigments Private Limited (RGP) for a consideration of Rs.56.75 Crores. Again this is recycling of non-ferrous materials which is non-core to them

Godawarai is not known as a brand outside their current business and how this diversification can help or impact the growth of the company? Any insights from experience boarders who track this company closely is appreciated.

Link to the notification is provided below:

5 Likes

More than growth, I see these as attempts to diversify business profile from ‘iron dependent’. Management has alluded to Steel as hedge to iron ore bet as well, when inquired about steel investment being RoCE dilutive in nature. Though at very good RoCEs.

Large capex is being done across the industry to increase Iron Ore mining. Lloyds, NMDC and Captive iron ore mines from large steel players. And it is (and likely to remain) a commodity.

Investment in these 2 business line is not substantial. Approximately cashflow generation from 1 quarter.

Option value can be provided. If management sees opportunity to scale and generate value, they will do it. And, they are likely to have cash generation for that.

Disclosure: Invested.

10 Likes

Godawari Power & Ispat Limited (GPIL) has entered into a definitive agreement to acquire upto 51% Stake in Jammu Pigments Limited at a post money valuation Rs. 500 Crores (approx.).

5 Likes

It will be a good move if the said synergies are realized by GPIL through this acquisition. There is not much clarity on the foray into oPVC manufacturing which is already a crowded space.

2 Likes

Just Look at the peer comparison shared on twitter by someone. It does look like a great acquisition. Listed players in this space are really expensive.

10 Likes

Source for this is presentation shared by gpil management. To communicate acquisition rationale.

3 Likes

The stock appears to be at interesting levels again after the recent correction. I think certainty of earnings here is quite high given the upcoming triggers over the next few quarters.

The company should be able to do around 2000cr EBITDA in FY26 but I think the rerating will start as soon as the mining expansion approval is in. Only large risks I see would be a state mineral tax a la Karnataka and a significant downturn in the iron ore market globally. Currently prices are hovering around 100$ but long-term consensus is around 70-75$ due to large supply going live.

Disc: Currently invested. May sell at any point without informing. Do your own due diligence.

8 Likes

It’s a rational move. I have earlier raised my concern why they are venturing into a non core business. Better sense prevailed.

4 Likes

for diversification and to remove the tag of commodity

1 Like

But steel is not noncore. Surprised they dropped it after talking about it for how long? Two years?

Yes, I agree. I was referring to the OPVC business. However, they have clearly stated that they will explore alternative options with minimal capital expenditure. Adopting a cautious approach to new spending is a wise decision. GPIL benefits from owning captive mines, while large-scale steel manufacturers are struggling due to China’s dumping practices. Additionally, the 25% tariff imposed by the US further impacts steel companies. It is prudent for GPIL to proceed slowly with capacity expansion until market conditions become more favorable.

6 Likes

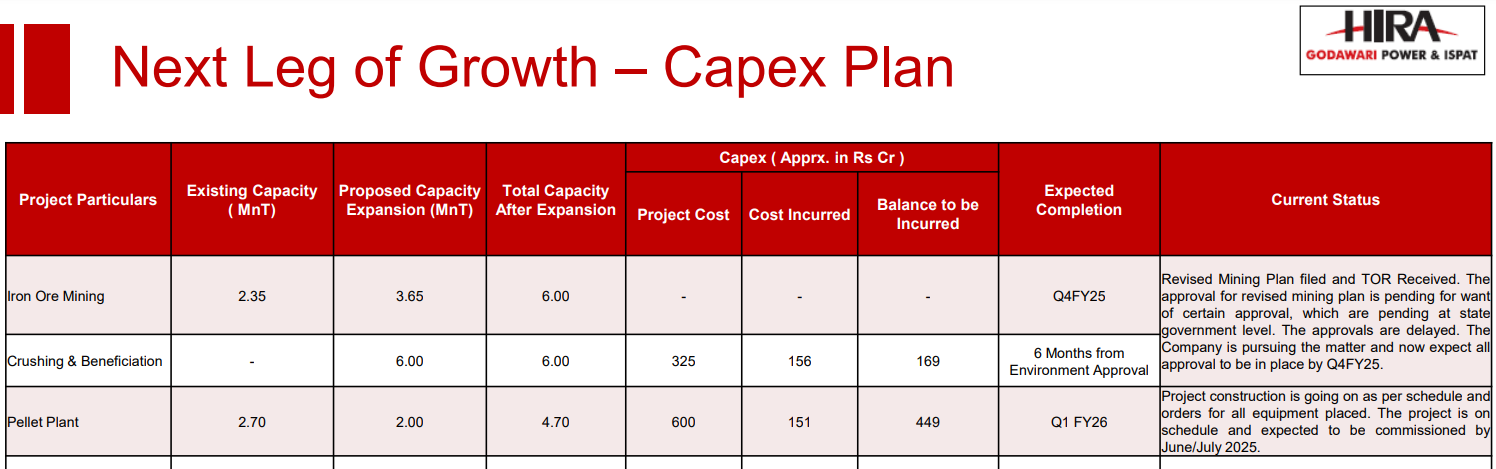

Only large 2mnt plant dropped will be substituted with smaller capacity. Steel remains a core activity but avoiding getting into flat products which is dominated by large players and have lower return as it is more influenced by global trade. GPIL will do value added long steel products which is linked to domestic trade.

8 Likes

Recent rally in iron ore prices have taken it to above 110 level, which is quite surprising. Domain experts are requested to give their observations on positive implications on pellet price in general and GPIL in particular.

4 Likes

The company has loaned 50 crores to deccan gold mines @ 12% pa.

This comes under related party transactions. While they are transparent, hope it is not a way to transfer money.

2 Likes

Godawari is sitting on Rs700cr of cash balance. And with internal accruals currently exceeding capex as there is a timing difference. They have to do treasury management in the interim. Company is trying to maximise it’s returns above the 7% they get in FD, at the same time lending where they are comfortable to recover the money.

13 Likes

12% safeguard duty on steel

https://x.com/hd_kumaraswamy/status/1914331513627529409

4 Likes