Some calculations can be based on this.

4 Likes

Interesting read shared by fellow boarder @Chandragupta in “Commodity and cyclical plays”. Some snippets as below:-

Request members with knowledge in this area to share insights on the impact of this on GPIL and the Indian mining sector

6 Likes

I think below statement from the article will required to be closely watched;

The slowdown in China comes, crucially, as a new generation of large, low-cost mines in Australia and Africa start production. That mix is the problem because it means the iron ore market, already oversupplied in the first half of this year, would remain in surplus in 2025, 2026, 2027 and probably 2028, too. Macquarie Bank Ltd., an Australian lender, says that the current surplus is “one of the worst” ever.

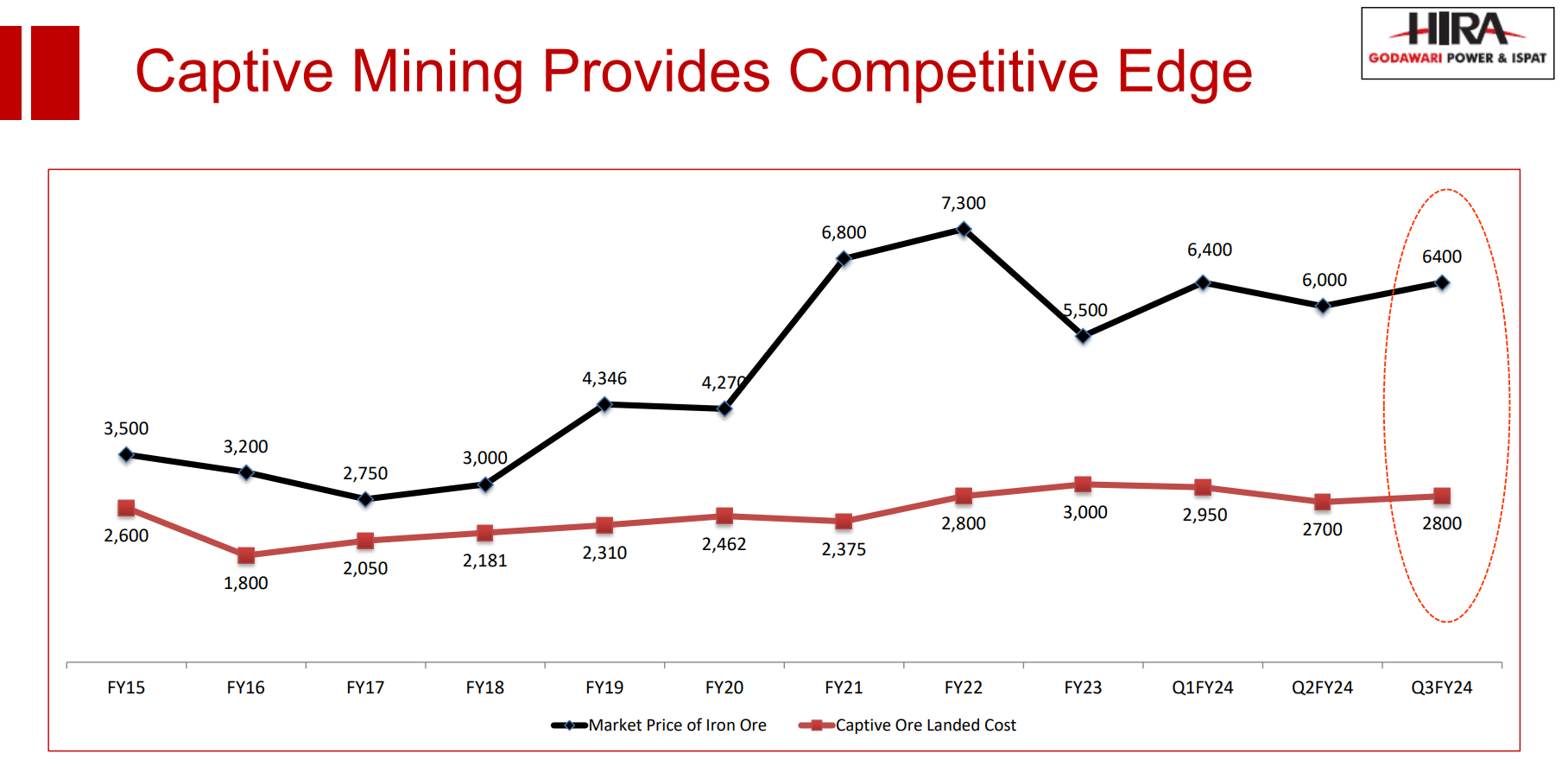

For GPIL the landed cost of captive iron ore is around 2800rs ($40).

Currently the iron ore price is around $98.

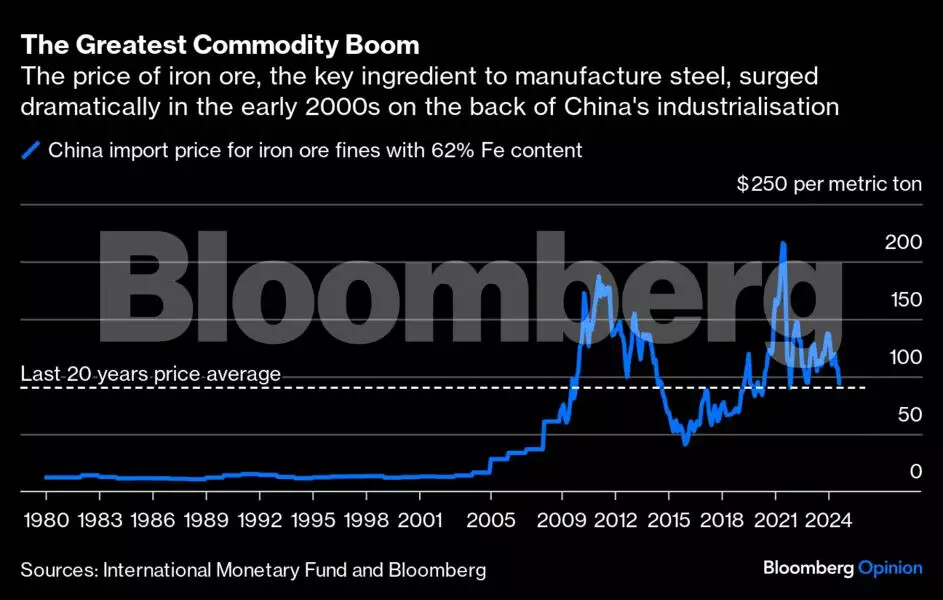

Iron Ore - Price - Chart - Historical Data - News (tradingeconomics.com)

The article also pointed out that;

Over the medium-term, iron ore prices must drop to rebalance the market, pushing out high-cost miners. How low? It would depend a lot on whether the new mines come on stream on time, and whether the Chinese real estate sector recovers a bit.

In 2015-16, the prices dropped to $50 due to oversupply. Rio Tinto Plc., the world’s largest iron ore miner, digs the mineral out of the Pilbara region of Western Australia at a cost of about $21 a ton.

I think there is medium term risk to iron ore prices as pointed out in the article. There is higher probability of capital cycle playing out in this sector going forward.

However, GPIL is one of the low-cost producer having high grade Fe iron ore mines.

Disc: Invested & Biased. Not a mining expert or related to mining industry. Views are personal.

22 Likes

Monarch Networth - GPIL - Initiating Coverage.pdf (2.0 MB)

Very detailed report, Worth reading

13 Likes

STEEL INDUSTRY WEBINAR

1 Like

As it appears to me it is not at all a concern. It is just tracking fall in iron ore prices. If you see prices of all iron ore companies, you will observe similar trend. And it has nothing to do with book value. Iron ore prices in international market is at 52 week low due to Chinese concern and it may go down further as per experts. And it is not going up until Chinese demand comes back. And to compound the matter further there is the concern of rising state royalties on the back of recent SC judgment.

6 Likes

If you are posting lines from analyst documents or from websites, do say so. You are confusing members who have invested. Also, it is better to add your own view, in addition to what you post, even if you are not invested.

3 Likes

What kind of book value multiple are you expecting for this cyclical stock in a regulated mining industry?

2 Likes

A book value multiple of 1 to 1.5x is generally reasonable.

1 Like

These are my own views to provide a balanced perspective.

2 Likes

India’s mining royalty rates are among the highest globally. Lowering these rates could boost investment and foster growth in the mining sector.

1 Like

-

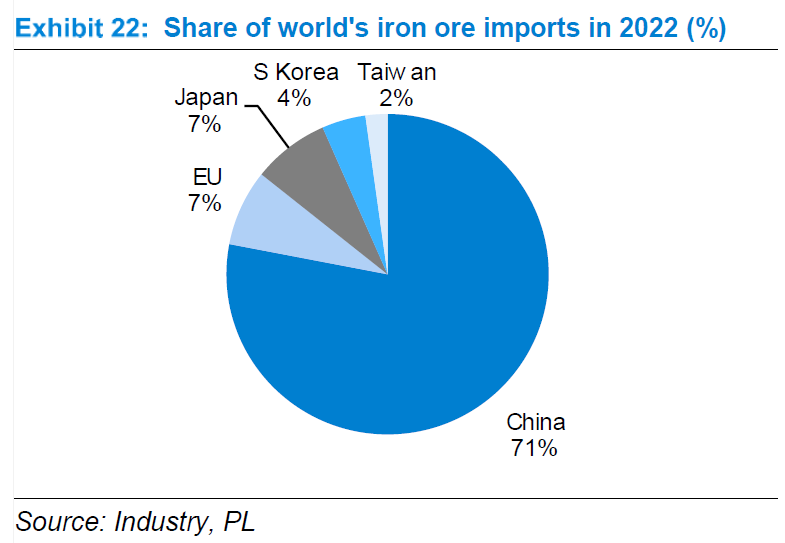

On average, the cost of producing iron-ore in Australia is $30/t, compared with $40/t to $50/t in West Africa and $90/t in China. According to Bloomberg, around 70% of Chinese iron-ore output is uneconomical at prices below $96/t.

-

According to the World Steel Association (WSA), global steel production was down by 4.7% in July this year and 0.7% during the January-July period of the current year compared with a year ago. However, this is not just a Chinese phenomenon. Steel production fell in four of the five top steel-producing nations—China, Japan, the US, and Russia – during the January-July period of the current year. India was the lone exception, recording a 7.2% positive growth in steel production during the same period over a year ago.

Iron ore is a very structured industry. The big four – BHP, Rio Tinto, Vale and Fortescue – control the market. Experts believe the way Opec does not flood the market, big four iron ore miners also won’t flood the market with excess production if there is insufficient appetite. -

Iron ore (62% Fe content) prices at Qingdao Port are currently hovering below $100/tonne, around $88/tonne as of August 16, marking the lowest level since November 2022, with the year-to-date average in 2024 thus far being $109/tonne, as per BMI data. Weaker iron ore prices have also cumulatively wiped out $100B in market cap from the world’s big four iron ore producers - BHP but analysts say the top global miners probably will be disciplined to prevent iron ore prices from collapsing too far.

Over the long term, however, the brokerage expects iron ore prices to follow a multi-year downtrend, with prices forecast to decline to $78/tonne by 2033.

Source:

11 Likes

I fail to understand what we are discussing here. This is not the thread for mining sector but GPIL. And we are not discussing personal views but ground reality. I do not agree that reducing royalties will lead to mining growth. But that is beside the point. Fact is SC has already approved right of State Govts to tax mineral mining. Moreover, it is retrospective. Some analyst say that the amount in case of Odisha only may reach 30000 cr. And majority of it on Iron ore. We can safely assume that other states will also join the bandwagon. It is apparent to any casual observer to see the squeeze in margin for iron ore companies, particularly when there is demand slump due to Chinese concern.

4 Likes

Is that reasonable for mining companies ? Or for steel companies ? Or is it for all companies ?

2 Likes

The general consensus is that mining or steel companies also operate similarly to others in the industry.

2 Likes

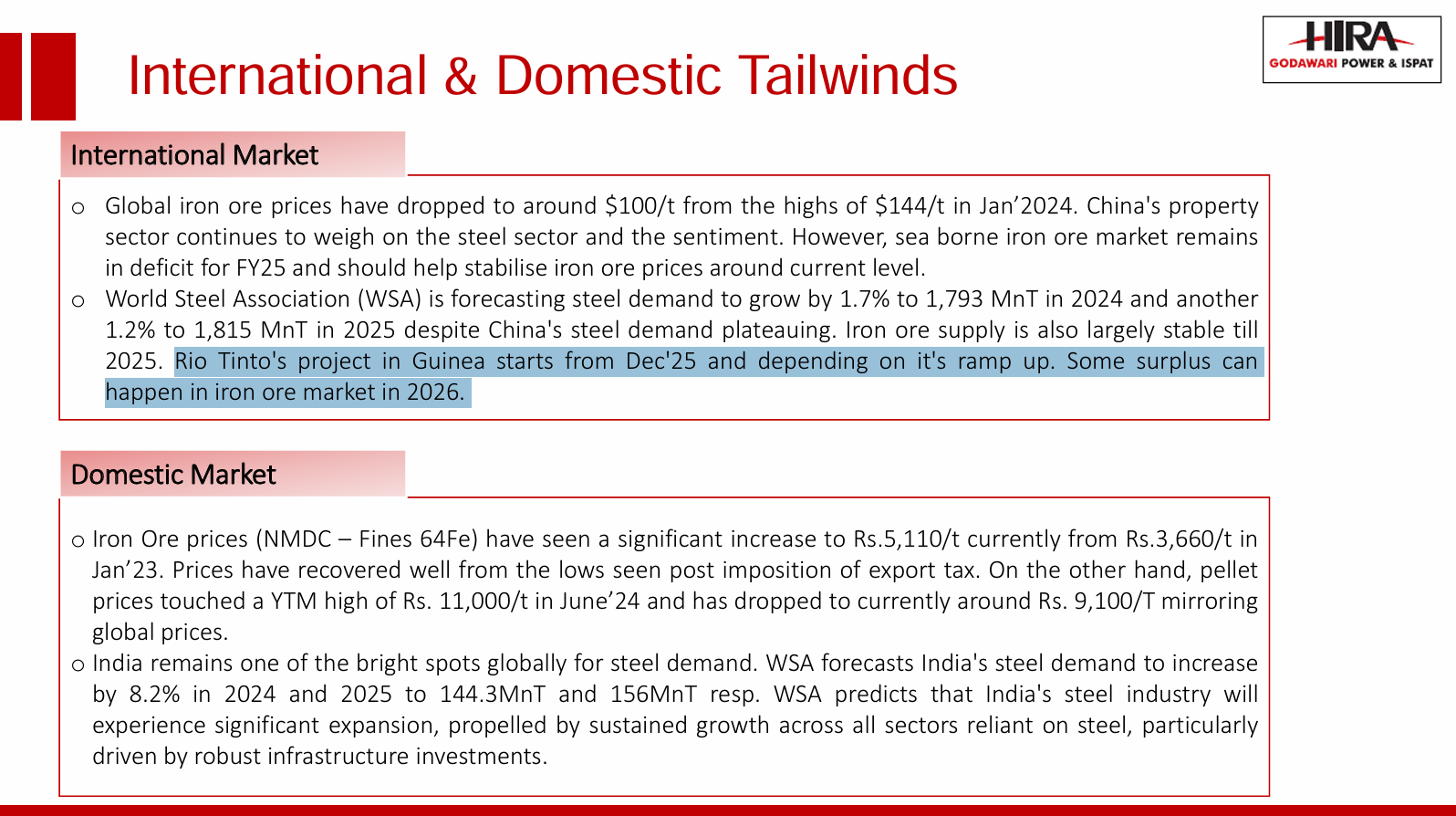

China Slowdown Concerns and Iron Ore Prices:

The ongoing slowdown in China’s economy and the drop in global iron ore prices are valid concerns. However, it’s crucial to note that GPIL is less exposed to these fluctuations than many other players in the market. One of the primary reasons is its fully backward-integrated operations. GPIL sources 100% of its iron ore from captive mines, which means it’s insulated from the volatile pricing that typically affects companies reliant on external sources.

Moreover, while the global slowdown is contributing to the correction in commodity prices, domestic demand for iron ore and steel in India remains strong. India’s steel production continues to grow at around 7% CAGR, and the government’s ongoing infrastructure projects are expected to provide steady demand for iron ore. In fact, GPIL’s premium pellets, which fetch Rs1000-1500 more per tonne due to their high Fe content, cater specifically to this domestic demand, especially from DRI plants in Chhattisgarh. This makes GPIL better positioned to weather the current global headwinds.

Strong Margins and Operational Efficiency:

GPIL has significantly expanded its pellet capacity, which will drive its revenue and profitability over the next few years. By FY27E, pellets will contribute 57% of GPIL’s revenues, up from 39% in FY24. The expanded capacity ensures that GPIL will continue to benefit from economies of scale, further lowering production costs while increasing margins.

Additionally, GPIL’s access to captive iron ore means it doesn’t have to pay premiums on royalty, which enhances its profitability compared to other steel producers who rely on externally sourced ore. The company’s integrated solar power plant also helps to reduce energy costs, providing additional margin stability.

Strategic Expansion and Long-Term Growth:

GPIL’s growth story is not just about the present—it’s about its strategic long-term investments. The company is planning to double its pellet capacity and set up a 2 million tonne steel plant, entirely funded through internal accruals, without incurring any debt. This steel plant will not only double GPIL’s EBITDA but also make the company even more resilient to commodity price fluctuations by fully backward-integrating its iron ore and energy requirements with green power sources like solar.

This positions GPIL as a net cash company, able to fund its growth internally, a rare feat in the capital-intensive steel industry. Even in the face of fluctuating global commodity prices, GPIL’s balance sheet will remain strong, and the company will be able to capture the next phase of growth without taking on additional financial risk.

29 Likes

What explains the rise in stock in last few trading sessions?

Prices of iron ore futures gained, as prospects of fresh Chinese monetary stimulus and lower inventories overshadowed concerns of the top consumer’s weakening domestic demand.

China’s central bank unveiled a broad package of monetary stimulus measures to revive the world’s second-largest economy, underscoring mounting alarm within Xi Jinping’s government over slowing growth and depressed investor confidence.

People’s Bank of China (PBOC) to cut Reserve Requirement Ratio (RRR) by -50 bps and to provide 1 trillion yuan in fresh new liquidity.

China to lower rates on existing home mortgages by around -50 bps.

11 Likes