4 Likes

These are ESOP exercised by employees

4 Likes

Two big investment company has announced

- 0.7 mtpa cold rolling mill in Jharkhand for cost of 900 cr.

- 700 cr BESS Project.

2 Likes

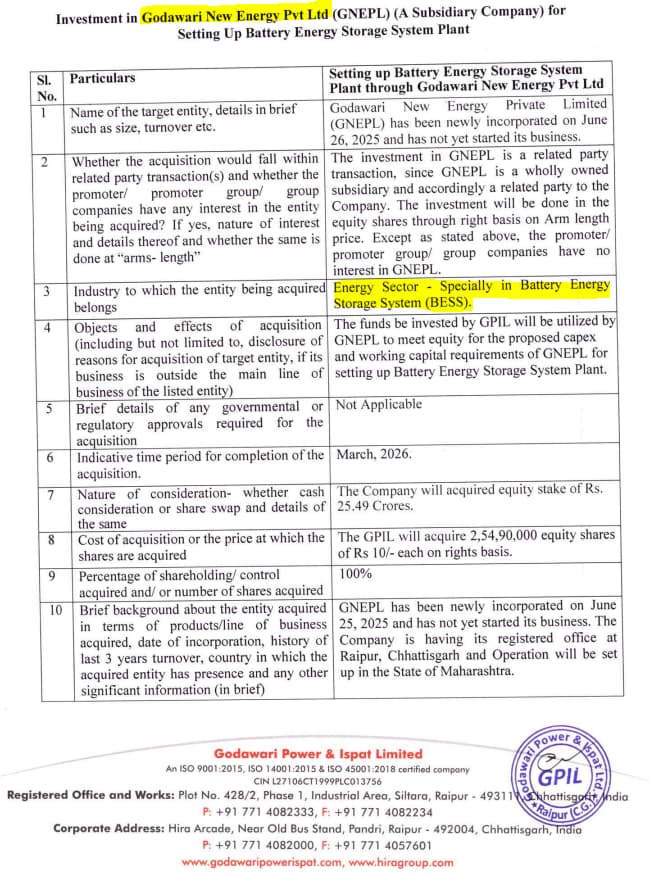

Entry into Battery Energy Storage Systems (BESS) via GNEPL

Key Details:

GPIL has incorporated a 100% subsidiary, Godawari New Energy Pvt Ltd (GNEPL), on June 26, 2025, to enter the Battery Energy Storage System (BESS) segment.

Total investment: ₹25.49 crore via rights issue (2.54 crore shares @ ₹10).

GNEPL will set up a BESS plant in Maharashtra, with expected operations to begin by March 2026.

This is a related party transaction, but conducted at arm’s length.

Thesis View:

India is pushing aggressively towards renewables + grid stability, and BESS is central to solving intermittency of solar and wind power.

Entry into BESS reflects management foresight in diversifying into future-ready adjacencies.

While small in size (₹25 Cr vs. GPIL’s scale), it offers an optionality in a high-potential sunrise sector.

Early-mover advantage + group’s engineering pedigree can be monetized over time if scale is built.

Long-term strategic bet, near-term impact on earnings negligible, but directionally very positive.

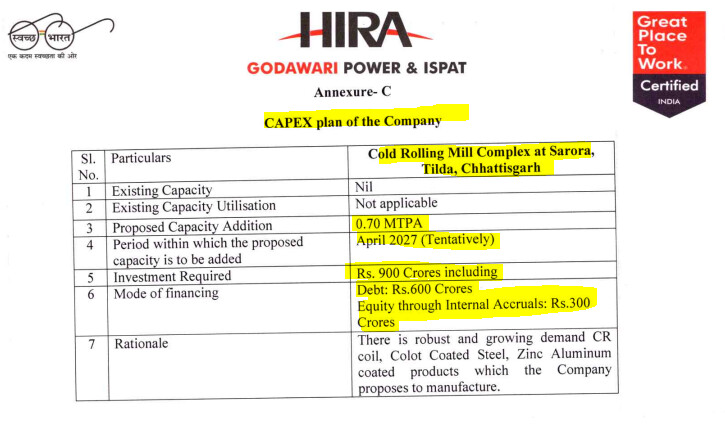

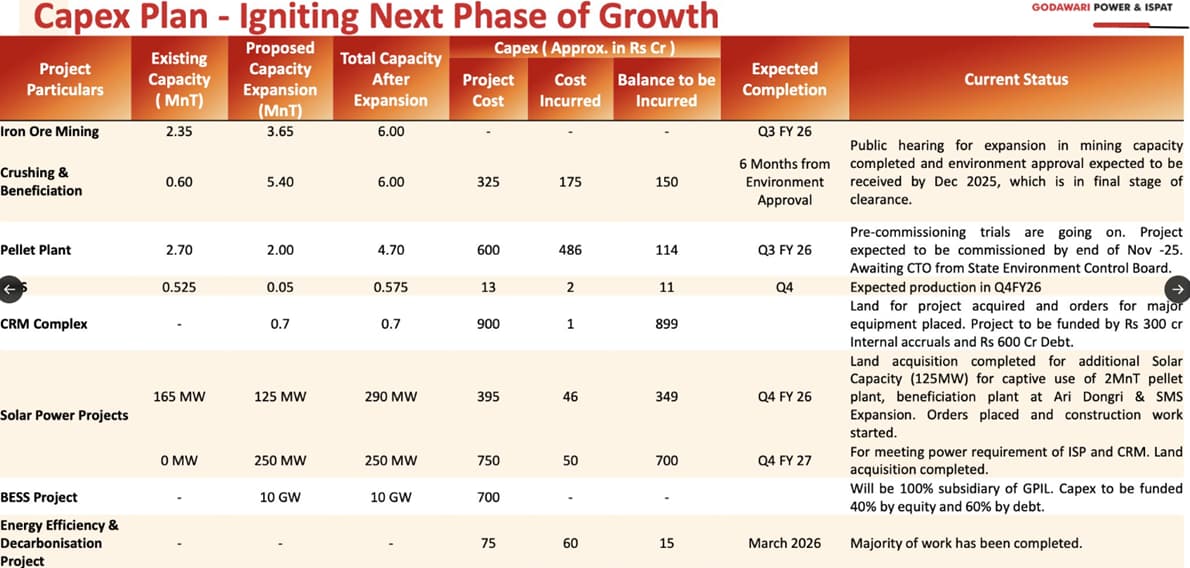

₹900 Crore Capex for Cold Rolling Mill Complex (CRMC) in Chhattisgarh

Key Details:

GPIL will invest ₹900 Cr to set up a 0.7 MTPA Cold Rolling Mill at Sarora, Tilda, Chhattisgarh.

Timeline: Completion by April 2027

Funding:

₹600 Cr via debt

₹300 Cr through internal accruals

Strategic Rationale:

Rising demand for Cold Rolled (CR) coils, Color Coated Steel, and Zinc-Aluminum coated products in sectors like construction, white goods, automotive.

Currently, GPIL is focused on iron ore, pellets, sponge iron, and TMT bars. This is a forward integration move to tap into value-added flat steel segment.

CR coils command better margins and pricing power vs. long products.

Helps de-risk cyclical dependence on raw material prices by entering higher-margin downstream products.

Thesis View:

Capex is large (~₹900 Cr), but manageable considering GPIL’s balance sheet strength and operating cash flows.

Adds product diversification and strengthens presence across steel value chain.

Could improve blended EBITDA margins and RoCE over time.

Execution and timely commissioning will be key monitorables.

Sources: Latest filings to exchanges

12 Likes

Refractory collapse on 26 Sep 2025 killed 6, injured 6; pellet plant closed pending inquiry.

Siltara plant accident on 26 Sep 2025: six killed, six injured; ₹46 lakh aid and long-term support.

2 Likes

Godawari Power & Ispat (GPIL) appears well positioned for a strong rerating in FY26. The company reported mixed Q2 FY26 results, but margins remained exceptionally strong despite lower realizations. GPIL posted revenue of ₹1,142.57 crore, up 4.2% year-on-year, EBITDA of ₹349.43 crore with a 27.8% margin, and PAT of ₹248.40 crore, marking a 60.7% year-on-year jump. EPS also rose 60.7% to ₹3.84. The balance sheet continues to be one of the strongest in the sector with very low debt (D/E of 0.03) and robust cash generation. Operational efficiency remains high and the company is advancing a strategic expansion plan, including ₹1,050 crore of capex in renewable energy. While the stock has already appreciated recently, the long-term outlook continues to be positive. GPIL is entering an aggressive expansion phase with approximately ₹3,200 crore of planned capex over the next 18 months focused on premium iron ore and green technology. The company has applied for environmental clearance to more than double iron ore mining capacity and its ore already commands a premium in the market. Land acquisition has been completed for its integrated steel plant, CRM complex, BESS project, and the new 250 MW solar plant. A major milestone has also been achieved with the completion of the public hearing to expand the Ari Dongri mine from 2.35 MTPA to 6 MTPA — a critical step before final environmental clearance. This expansion would significantly increase captive ore supply, enhance cost competitiveness, and support the next phase of steel and pellet capacity expansion, reducing regulatory risk and strengthening GPIL’s growth visibility.

11 Likes

The promoters of the company made a personal investment in Deccan Gold Mines (Financials attached below) in Aug '23. Since then 120 cr loan has been given by GPIL to DGML. In addition company is now subscribing to DGML’s right’s issue. Doesn’t look like a very prudent capital allocation to me. Also how come a company with 5 cr Annual sale end up having a Market Capitalisation of 1800 cr. If anyone has more info on the company, please share.

Status : Invested

1 Like

Deccan Gold Mines is India’s 1st private Gold Miner after independence

GPIL is trying to diversify from its core business into another adjacency of Gold mining apart from BESS plans

Deccan Gold Mines is operational but not yet profitable , with pre-commercial production trials underway at its Jonnagiri gold mine in Andhra Pradesh and its Altyn Tor gold project in Kyrgyzstan. The company is also starting drilling for critical minerals like nickel and copper in Chhattisgarh this December, but its Q2 FY26 results show significant operating losses and cost control challenges

Deccan Gold Mines can generate sort of 400 kgs Gold in 1st year with ebidta of around 60% as per Google search i did to understand high level view

Details are in this section

To myself it looks like a good move(may be forced too) to diversify and increase stake when they have good balance sheet, how it pans out needs to be tracked closely

6 Likes

Three updates worth noticing:

GPIL (Godawari power and Ispat) ramps up capacity again - The company has started commercial operations of its additional 2 MTPA iron ore pellet plant at Raipur effective 08 Dec 2025. Pellet capacity jumps from 2.7 MTPA → 4.7 MTPA Boosts value-added mix and earnings

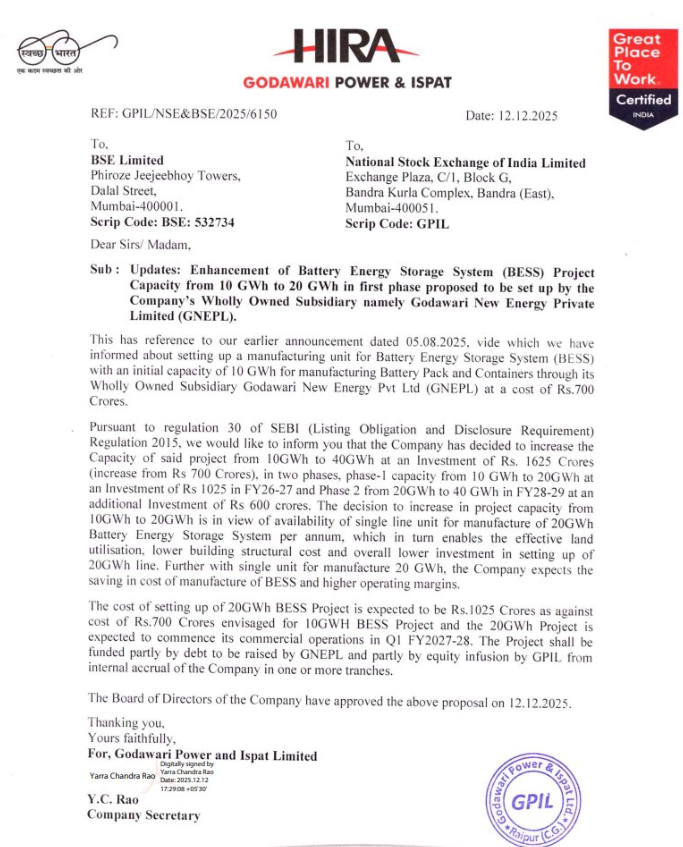

Godawari Power & Ispat’s subsidiary scales its BESS project from 10 Gwh to 40 Gwh. Total investment rises to Rs. 1625 Cr from Rs. 700 Cr. The 20 Gwh phase-1, costing Rs. 1025 Cr, targets efficiency, lower costs, and higher operating margins.

Unit Economics of A BESS project given by GPIL in their concall Insightful to understand this evolving sector

Godawari Power & Ispat (GPIL) The primary trigger at play for the near term for the company stands the Ari Dongri mine approval which it is expecting the approval by dec 2025 and is in final stages of clearance Mining Target: 6.7 MnT by FY26. + Pellet Target: 4.7 MnT by FY26. This will largely double their current mining capacity + also expanded its pellet capacity Now company is also putting up a CRM complex for production of specialised steel + also a BESS project GPIL is changing its DNA and is not just a integrated steel play

12 Likes

Godawari Power & Ispat Ltd (GPIL)

Business Model

Godawari Power & Ispat Ltd (GPIL) is a vertically integrated steel and iron producer based in Chhattisgarh. The company operates across the value chain—from captive iron ore mining to the production of pellets, sponge iron, billets, rolled products, and ferro alloys. It also generates power through captive thermal and renewable sources. GPIL benefits from strong backward integration, cost efficiency, and is expanding its capacity across key segments including a ramp-up of iron ore mining and renewable energy.

Financial Snapshot

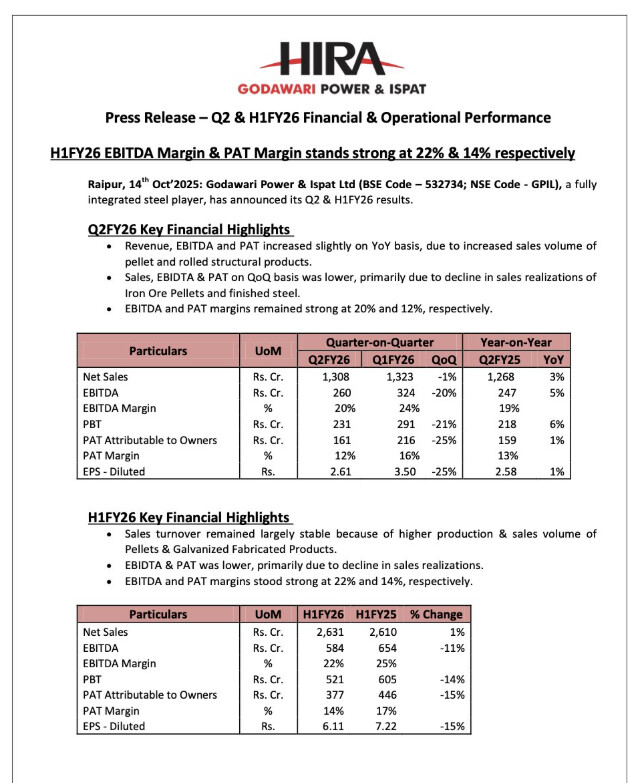

Q2FY26 Revenue : ₹1,308 Cr, up 3.16% YoY

Operating Profit : ₹260 Cr with 20% OPM.

Net Profit : ₹162 Cr, slight improvement from Q1FY26.

EPS for Q2FY26 : ₹2.41.

H1FY26 EPS Total : ₹5.64 (Q1 ₹3.23 + Q2 ₹2.41).

Steady Profitability : OPM ranged between 20–24% in FY26 so far.

Moderate Revenue Recovery : Sequential uptick seen post Q1FY26 dip.

Margins stable despite modest topline growth.

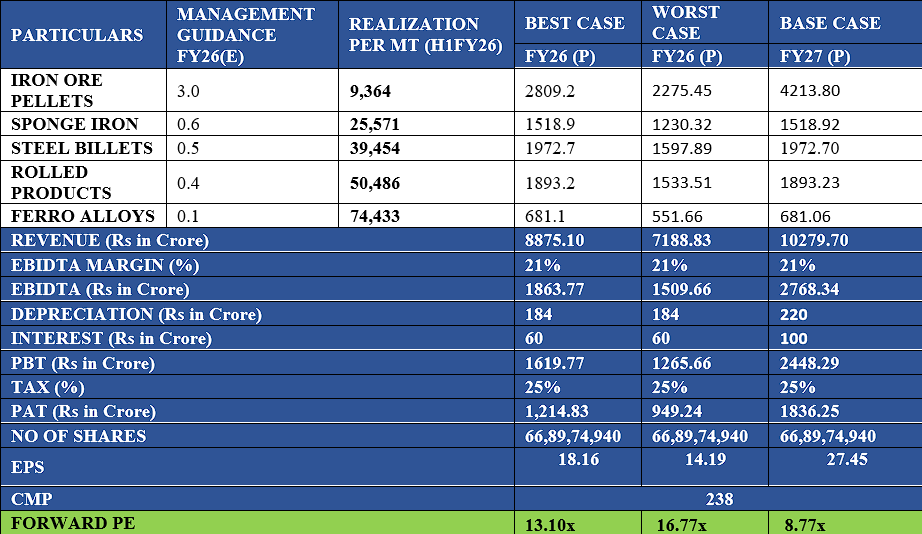

Realization Per MT/Rs mentioned below:

| Product | Q1 FY26 | Q2 FY26 | QoQ | Q1 FY25 | (Q1 FY26 vs Q1 FY25) | FY25 Avg |

|---|---|---|---|---|---|---|

| Iron Ore Pellets | 9,828 | 9,364 | -5% | 10,503 | -6% | 10,060 |

| Sponge Iron | 24,756 | 25,571 | +3% | 30,986 | -20% | 29,123 |

| Steel Billets | 41,682 | 39,454 | -5% | 45,342 | -8% | 42,971 |

| M.S. Rounds | 44,408 | 42,167 | -5% | 48,019 | -8% | 45,455 |

| H.B. Wires | 48,075 | 44,875 | -7% | 50,039 | -4% | 47,241 |

| Ferro Alloys (Cons.) | 75,399 | 74,433 | -1% | 72,218 | +4% | 72,011 |

| Galvanized Fabricated | 78,767 | 79,035 | 0% | 76,408 | +3% | 72,277 |

| Rolled Structural | 49,047 | 50,486 | +3% | N/A | N/A | 49,502 |

Positives

-

B2B, diversified (~120 dealers; no customer >10%)

-

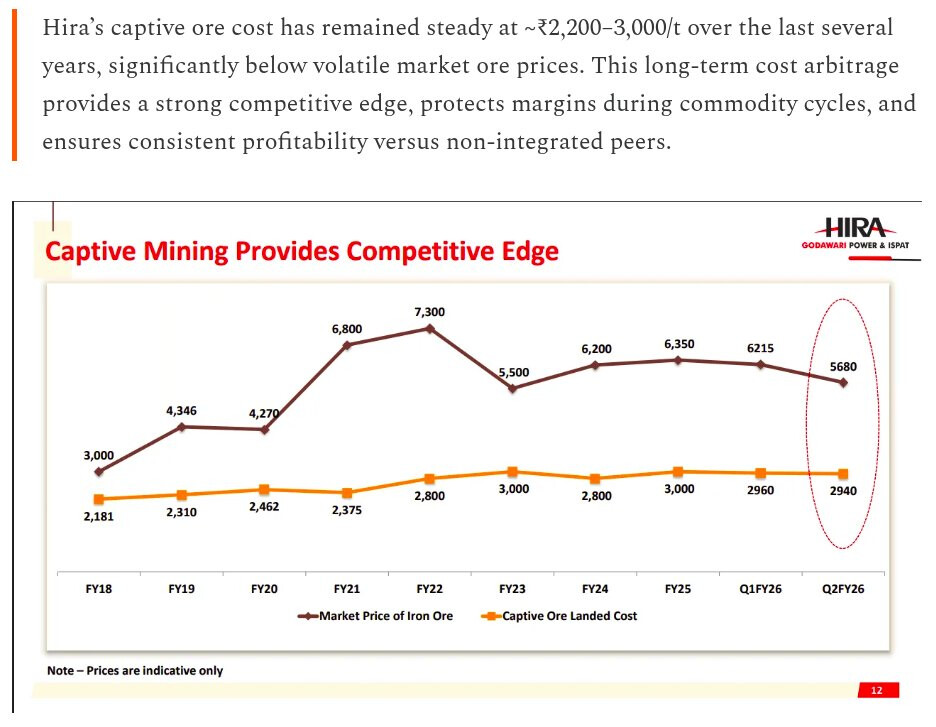

Captive Resources : Mines (165 MT reserves, 35+ yr life; cost edge Rs 3,000+/MT savings); power (164 MW solar + expansions).

-

Premium Products : High-grade pellets (+Rs 1,000-1,500/MT); PGCIL-approved billets/structures (improved margins).

-

Financial Strength : Net cash Rs 863 Cr; 36% PAT CAGR FY20-25; funds growth internally.

-

Sustainability : Net-zero 2050; 2.37 tCO2/ton steel (WSA assured); ISO 50001/27001; decarbonization (WHR, CCU pilot).

-

Expansions : Mining/pellets FY26; CRM/BESS FY27; integrated steel (1 MTPA post-mining EC).

-

Group Synergies : Ferro alloys/power subs; JPL recycling (zinc synergy from galvanizing)

-

Mine Expansion Headroom: Increasing Ari-Dongri mine capacity ensures raw material security for future growth, supports downstream expansion, and offers flexibility for surplus monetization.

-

Pellet Capacity Expansion : Pellet capacity to reach 4.7 MTPA by end of FY26, up from current levels.

-

Value-Added Focus : Strong push toward HB wires and fabricated steel to improve margins and retail presence.

Ferro Alloys Export Boost : Exports now form over 70% of ferro alloy sales, driven by strong global demand.

Integrated Operations : Pellet plant operates on 100% captive iron ore , ensuring secure and cost-efficient input supply.

Beneficiation Plant Upgrade : Ongoing magnetite beneficiation capacity expansion to support higher pellet output.

Power Cost Optimization (Future) : 250 MW solar plant expected to reduce power cost significantly post commissioning (first phase by June 2026).

Targeted Pellet Margins : Company aims for ₹5,000–₹6,000/tonne EBITDA in pellet business with scale and efficiency.

Key Concerns & Negatives

- Solar Plant Delay : Only 100 MW of the 250 MW solar plant expected by June 2026; cost benefits deferred.

- Falling Pellet EBITDA : Pellet EBITDA/t fell to ₹2,675 in H1FY26 vs ₹3,127 in FY25 due to lower realizations.

- DRI Feed Rigidity : Sponge iron plant fully depends on pellet feed; no flexibility to use direct iron ore.

- Beneficiation Ramp-Up Risk : Delay in magnetite beneficiation expansion could impact pellet scaling.

- High Power Costs : Power cost remains elevated at ₹8.5/unit, pressuring margins until solar savings kick in.

- Capex Execution Risk : Simultaneous projects increase chances of delays and cost overruns.

- Battery Storage & Deccan Gold Bets : Early-stage capex in battery storage and Deccan Gold should be monitored for cash drain.

- Capital Allocation Monitor : Investment in Jammu Pigment and other ventures must prove efficient over time.

Future Outlook

*Assuming Captive Beneficiation benefit to be at Rs.400 per Ton adding 255 Cr to EBIDTA & Iron ore captive benefit to be at around 345 Cr on the conservative side.

CONCLUSION

GPIL is positioned to benefit from operating leverage as its key capacity bottlenecks ease by Q3FY26 and fully by Q2FY27. The upcoming 6 MTPA magnetite beneficiation plant will significantly reduce the landed cost of pellet feed, enhancing margin resilience. Additionally, the phased commissioning of its 250 MW solar plant is expected to lower power cost to ₹5.5-6/unit, unlocking further profitability in energy-intensive operations. These structural improvements could drive strong earnings momentum over the next 18–24 months. The stock currently trades at a forward P/E of 16.8x FY26E EPS of ₹14.19 and 8.7x FY27E EPS of ₹27.45, indicating a favorable risk-reward profile. With key triggers such as the beneficiation plant, pellet capacity expansion to 4.7 MTPA, and 250 MW solar plant expected to come online over the next 12–18 months, structural cost efficiencies and volume growth could drive meaningful earnings upside.

11 Likes

Is this mine related to Godawari or different? Experienced boarders please clarify

Seems not related to GPIL.. this is that I got through AI

In the Tamnar block of Raigarh district, Chhattisgarh, several major coal mining projects are underway or proposed, primarily centered in the Gare Palma (also spelled Pelma) sector. As of late 2025, these projects have become focal points of intense local opposition and civil unrest.

Major Coal Mining Projects in Tamnar Block

Gare Palma Sector-I: Currently allotted to Jindal Power Limited. It is the site of recent violent protests as villagers from 14 affected areas demand the cancellation of the project and its public hearings.

Gare Palma Sector-II: Operated by the Adani Group for the Maharashtra State Power Generation Company Limited (MAHAGENCO). It is one of the largest proposed mines in the region, with an estimated yield of 655 million metric tonnes of coal.

Gare Palma Sector-III: Allotted to the Chhattisgarh State Power Generation Company Limited (CSPGCL). Baseline studies and land use classifications were being conducted as recently as 2024–2025.

Gare Palma IV/2 & IV/3: Integrated opencast and underground mines previously operated by Jindal Power Limited. Recent efforts include expanding capacity to 6.25 MTPA and setting up an 800 TPH coal washery.

Other Blocks: The block also includes the Gare Palma IV/5 underground mine (currently mothballed) and the Purunga coal mine.

Recent Developments and Conflicts (December 2025)

Violent Protests: On December 27, 2025, a protest against the Gare Palma Sector-I project turned violent. Protesters allegedly torched police vehicles (buses, jeeps, and an ambulance) and stormed the Jindal Power Limited coal handling plant, vandalizing equipment like conveyor belts.

Casualties: At least 8–10 police personnel, including senior officers, were injured during stone-pelting and clashes.

Core Issues: Villagers and tribal communities cite “fake” public hearings, lack of proper Gram Sabha consent, and forced displacement from forest lands as primary reasons for their resistance.

Government Response: Chhattisgarh Chief Minister Vishnu Deo Sai ordered an official inquiry into the violence, and the local administration has initiated the process to cancel the controversial public hearing for the Jindal project.

2 Likes

AI articulated

The rights allotment process for DGML is now complete.

Because GPIL had previously committed to subscribing to its full entitlement plus any unsubscribed portion of the rights issue, it will be interesting to monitor the disclosures over the coming weeks to see the exact increase in their stake (specifically acquiring rights entitlements from the existing promoters, Rama Mines and Australian Indian Resources + unsubscribed portion if any)

GPIL is essentially acting as a “backstop” for DGML. By providing the debt to build the mines and the equity to shore up the balance sheet, are they positioning themselves to be the dominant stakeholder if DGML’s gold projects (like Altyn Tor) successfully move into production ?

4 Likes