Good Summary Ayush. Just one point the repayment mentioned for current year probably just for stand alone entity and doesn’t include repayments for it’s subsidiaries Ardent steel and Godawari Green. Watch out for results today for clear picture on debt repayments.

4 Likes

Yeah. Very strong results.

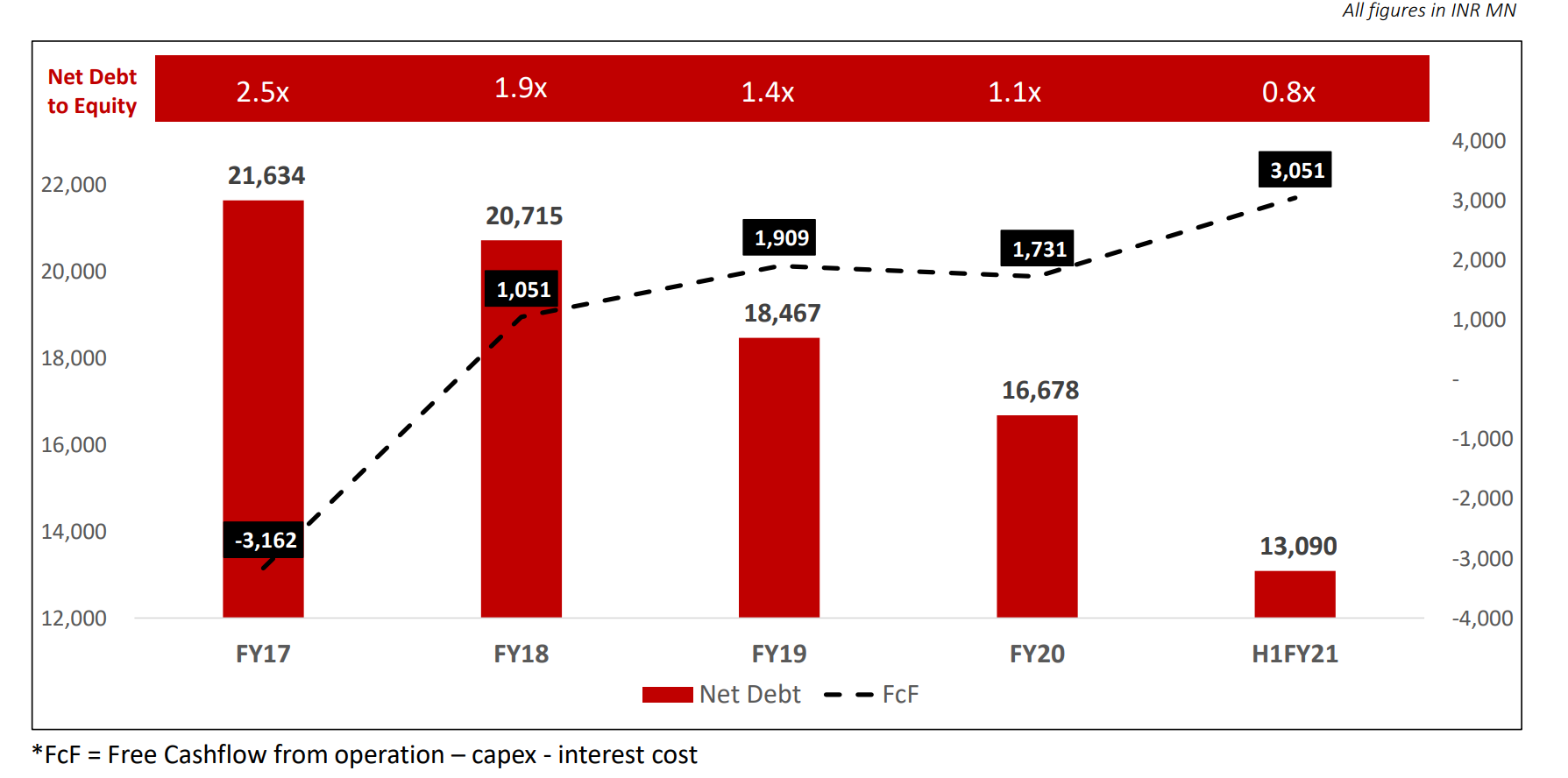

EBITDA at Rs235cr and Pellet realizations were only Rs7000/t . Today pellet prices are far higher and likely to sustain in the near term which could mean debt could be down another 300 cr in H2FY21 to Rs1000 cr. With Crisil upgrading their ratings, interest rate could fall to 9% from 11% for FY22.

Very likely that by FY23 end, very little debt will be there on balance sheet.

Valuation today - EV of 2600 cr with 1300 cr market cap + net debt of 1300 cr. Very high probability of debt being swapped in favour of market cap- thus doubling the stock in 2-3 years. I am not even counting any re-rating possible. Maithan Alloys - 0% growth, no moat, but debt free and only one line of business (ferro alloys) trades at 6x EV/EBITDA. Godawari at 3.5x EV/ EBITDA today.

6 Likes

Godawari Q2FY21 conf call details

Hi Rohit, banks don’t release pledge till last penny is paid. So it should take another 2years to repay the full debt. The rating doesn’t matter and pledge is not linked to stock price.

They want to exit all businesses outside of Chattisgarh and Ardent falls in the same non-core for them. The replacement cost is around Rs175cr and non one is willing to pay anything more than replacement cost and 1-2years of profits. With the auction of iron ore mines in Orissa, the merchant availability of iron ore has gone down dramatically. Transtek Coal and Minerals is a trading company with long term contracts for iron ore and will ensure sufficient supply of iron ore to keep Ardent’s pellet plant running. Eventually, Godawari will fully exit Ardent at appropriate time. And Transtek is no way related to promoters.

6 Likes

Listen to the conf call recording here. Mr B L Agarwal has handled this issue at the fag end of the call.

2 Likes

I have gone through the concall what I understood is they are practical about steel cycle. Everyone of us sceptical about stake sale.

Reason 1: Mr. Agarwal (MD) explains that when good times is there someone will come and purchase stake.

Reason 2: Any one can come up with this type of plant in a period of 1nd1/2 yr to 2 yrs. No one will pay more than replacement cost.

Reason 3: It’s a single product plant and there is no iron ore sourcing advantage. If we add stratergic partner he can source iron ore at reasonable prices.

Reason 4 : To reduce debt and focus more on Chattisgad facility.

@ayushmit can add more because he is in the call.

4 Likes

Iron ore prices in India hit 10year high. Pellet prices latest deals heard at Rs11500/t. This compared to Q2FY21 avg price of Rs7000/t. I tried to calculate who benefits, how much as compared to market cap.

Source: Diwali Continues here...

7 Likes

Any particular reason that stock is in the circuit band of 5% for last around four months? There is no heavy movement in stock price for last three four months…still it is been kept in 5% band for so long…

stock under ASM framework of exchange. Not exactly sure how it works, but review due now in Dec.

Now it is not part of ASM framework, I think It was out of ASM around one month back,

Yesterday also Circuit filter has been revised and ASM list has been issued by NSE and BSE, GPIL is not in the ASM list. But GPIL Circuit filter has not been revised and remain to 5% only.

2 Likes

3 Likes

Tried to calculate the market cap of Godawari on various combinations of EBITDA and EV/EBITDA. Still plenty of upside left

Source:Godawari 2.0 - Debt Free Growth

7 Likes

Hi @Rakesh_Arora ji,

It was good to see your educational video on the steel sector - https://www.youtube.com/watch?v=aXD20h5Z-1Y

You explained everything very easily! Kudos.

I have also been tracking this space closely for last 3-5 years and like you mentioned, It seems the cos with long term mines (which are not coming up for renewal) are big beneficiaries. Due to high premiums, the cost should remain very high for new miners so the old miners seem to have a big cost advantage rather arbitrage going ahead. I also feel GPIL has not got its due ( maybe biased as invested) given the “walking the talk” done by the management and strong de-leveraging done. Market cap has not increased even equal to the debt reduction done till now over last 3 years.

If they can sell/get off from the solar power business or maybe demerge the same, that will be really good.

Another co which seems to be a beneficiary with growth ahead is Sandur - would be good to get your thoughts/insight on the same (there is another thread for the same).

Thanks & Regards,

Ayush

11 Likes

Thanks Ayush. Couldn’t agree more on Godawari. While divestment of power plant would have been ideal and remove unnecessary diversification, but now has become non-critical due to low debt. Also maybe Godawari can one day claim to be carbon neutral and attract ESG investors. I think as market cap improves, funds will find it difficult to ignore. Btw in Dec, Godawari is one of the most added small cap by MFs. I will have a look at Sandur. Lots of people asking.

7 Likes

One thing that I wanted to clarify was the stake sale in Ardent steel. The management commentary regarding the sale definitely made sense considering ore availability in odisha. Recent MOU with Chattisgarh govt makes it clear that they want to grow their capacity around their captive mines. But how do you see the valuations of the deal?

Disc: Invested

Hi Jose, the replacement cost of the plant similar size is Rs150cr and none of the other potential buyers like Tata Steel, JSW Steel etc were willing to pay any more than this. So Rs300cr is reasonable from replacement cost basis. Now the partner which Godawari has got with very high capabilities in iron ore sourcing, will make sure very strong profitability for Ardent. We should get some clues on how this partnership is going in the upcoming results.

2 Likes

@Rakesh_Arora Sir as you said in video , main thing is iron ore prices and China steel export import .

Also they have direct effect on stock price without a lag

Sir how can we track this data on real time basis or fortnightly as possible

Deepakji most of this data is behind paywalls and subscriptions to industry sites like Mysteel.in, SteelMint, Platts etc. Best as I have recommended to others is to put google alert for news on “China Steel Exports” you will get news articles which should be enough to guide you.

2 Likes