Ok thanks sir will put forward this

No company specific news but generally market is worried about

- Fall in steel prices in China and now in India

- Possibility of some export tax on iron ore pellets in the budget

Whole sector is seeing correction btw.

1 Like

@Rakesh_Arora, Shouldn’t the point - 2 be indeed positive for JSPL as they don’t have captive iron ore?

Not for current year. They have captive mines of 3-4mnt and also sitting on pre-paid inventory of 8-9mnt. Next year they can benefit but remember their costs will rise sharply in any case as this cheap iron ore inventory gets consumed.

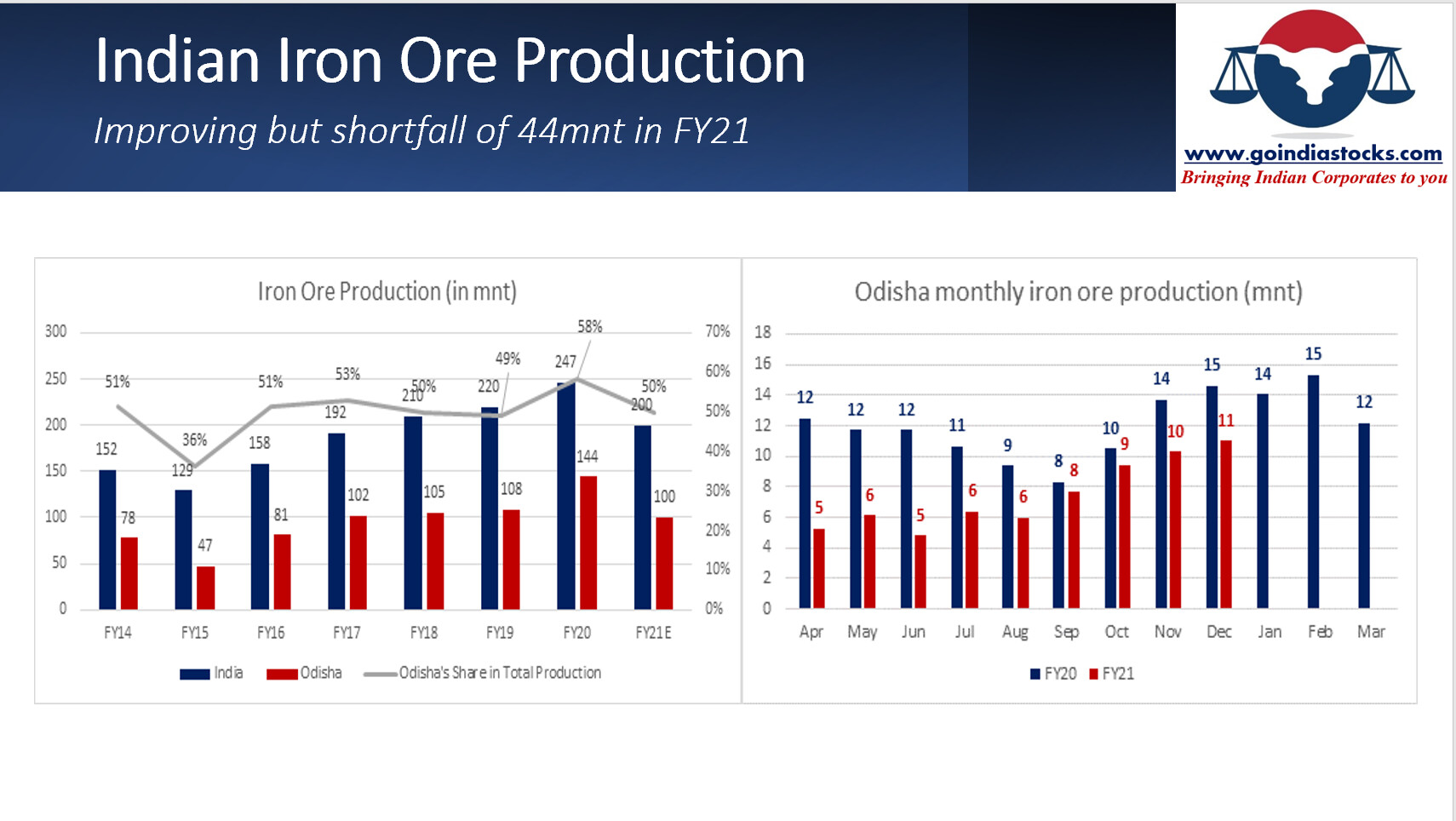

Iron ore production shortfall to be 44Mnt in FY21. Shortages should last well into FY22 too unless government takes some drastic steps

6 Likes

A few months back govt had clearly ruled out tax on pellet exports, although a possibility , i think its low on probability.

3 Likes

Result out:

Rs 5 dividend.

EPS (consolidated): 45.64.

Growth of 54% from 30/09/2020

Growth of 400% from 31/12/2019

6 Likes

Consolidated numbers masks the actual performance of steel sector. They made 30% EBITDA this quarter which will rise in Q4.

Any idea why the taxation is so high?

2 Likes

Q3 PRESENTATION.pdf (1.6 MB)

Very impressive figures:

Long term debt reduced by 667 Cr during current FY 20-21. We can expect further debt reduction in this quarter.

Outstanding Long term debt only Rs 873 Cr. If the current pricing of pellet continues for another 9 to 12 months then the Company will certainly become debt free.

50% dividend Rs 5 per share…

Financial cost reduced substantially.

Financial cost during previous years

2014-15 Rs 224 Cr

2015-16 Rs 252 Cr

2016-17 Rs 259 Cr

2017-18 263 Cr

2018-19 253 Cr

2019-20 212 Cr.

For 9 months 126 Cr and it will be around 160 Cr for the full year…

Even at the current debt level 873@9% Financial cost will be less then Rs 100 Cr for FY 21-22.

Cash accruals will substantially increase once it becomes debt free and will help the Company to fund its expansion without raising debt.

I am really impressed with the granular details they provide in their presentation…

Commendable…

Disclosure … Invested and recently increased my stake.

6 Likes

Also, interesting that Ardent has turned around with strong volume growth due to higher availability or iron ore due to strategic partner. It would be great if Godawari can get sustainable dividends from Ardent hereon.

Interesting to see if they announce a dividend policy in a quarter or two. They will have sustainable Free cash flows of Rs500-700 cr annually (ofcourse today the FCF run-rate of Rs900-1000cr due to strong prices).

I guess the company is a re-rating candidate. Interest coverage, leverage ratios are vey well under control.

4 Likes

No export tax on pellets. Positive for Godawari. Conf call tomorrow at 12PM

DOMESTIC ACCESS NUMBERS:

Access Number 1 - 91767 96600

Access Number 2 - 044 4563 4951

Earnings Call Invite - https://goindiastocks.com/GIA/NewsDetailStock?Id=84

4 Likes

Major takeaways from the call:

- Mining capacity to rise by 0.8 mn tonnes in FY22- this means additional sustainable EBITDA of Rs160 cr (0.8* Rs2000/tonne) atleast.

- Improving product mix in favour of billets, wire rods…no sponge iron sales…more price stability

- Debt free (excluding solar power plant) during FY22

- Dividend policy to be finalized soon.

This means sustainable EBITDA could be Rs7-800 cr per year. Free cash flows could be Rs500 cr after paying tax and maintenance capex. So FCF yield as it stands today is over 25%. Valuation at 2.3x EV/EBITDA for a debt free (soon to be) company and for a company with a moat (captive iron ore mine) looks very cheap.

Next catalysts could be 1) sustainable dividends payouts from Ardent to the parent, 2) GPIL starts paying out 30% of PAT as dividends, 3) Higher mine production (very strong catalyst) and 4) selling off Godawari Green (very remote possibility).

7 Likes

Concall takeaways

1.Deleveraging continous strongly.

Long term Debt @ 500 crores on a standalone basis expected to be completely paid back by the end of calendar year

2.Average pellet realization at 11500 per tonnne from around 9000 in the last quarter

3. Company expects to be out of debt restructuring soon.

4. Company expects to receive ec for increasing mining capacity by the end of FY 21.

5. 375 crores of long term debt for godawari green

Invested

3 Likes

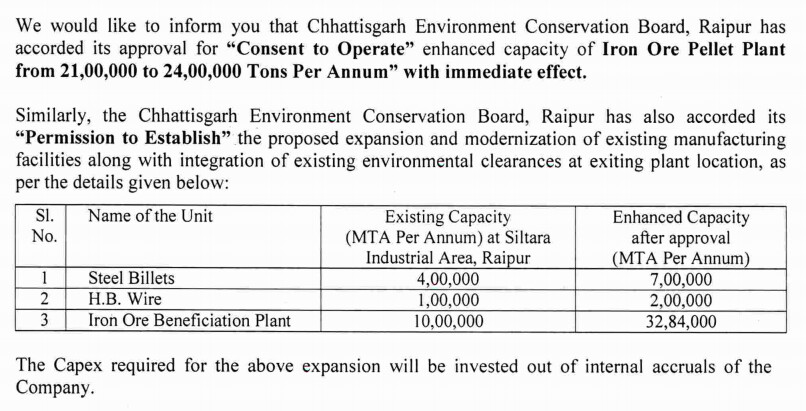

Delivery of High Grade Iron Ore Pellets (65.5% Fe) to China and Other Countries started by company

ef28ca68-77a5-45be-a154-b89329ed6dca.pdf (113.7 KB)

2 Likes

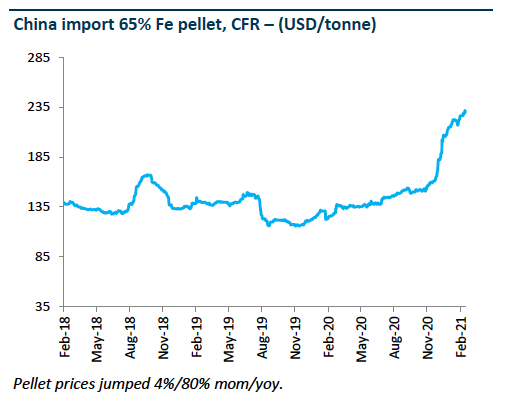

Research Report from Philip Capital

Here is the full report.

1627105523PC_-Metals_Monthly-_February_2021_20210227190038 (1).pdf|attachment (1.1 MB)

4 Likes

Hi All, Very informative details in this article about current situation in China steel plants crackdown. Please share your views.

https://www.metalbulletin.com/Article/3977670/Latest-news/FOCUS-Key-effects-of-Chinas-latest-industrial-crackdown-in-Tangshan-on-steel-sector.html

Good article. The key takeaway is that China closes down smaller blast furnaces which are inefficient and polluting and replaces it with much larger efficient furnaces. The effect is that both steel capacity is going up and at the same time it is becoming low cost. So, contrary to the popular perception that this is positive steel prices, this is in fact negative steel prices longer term.

15 Likes

Can someone share the con call transcripts of 26 Mar