Hi Deepender,

I track the prices of Iron Ore pellets on steelmint and cross checked it with the CFO of the company. Also, they paid 90 crores in Q1 and not 70 crores.

3 Likes

Thanks, 100 crore will be in Q2?

That’s my assumption, it should be between 90 to 100 crores as the cash generation this quarter is very high and management seems focused about repaying debt.

1 Like

NMDC increased the prices of lump ore by 10% effective from 5th of September 2020. Hopefully this should increase the spread of iron ore pellets for GPIL.

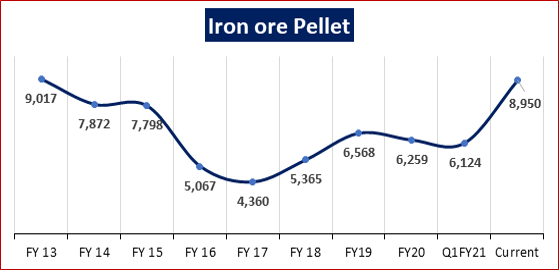

Current prices of Iron Ore pellets at Rs. 9,000 ex raipur (Source: SteelMint)

Disclosure: Invested.

6 Likes

Below is the price trend for Iron Ore Pellets

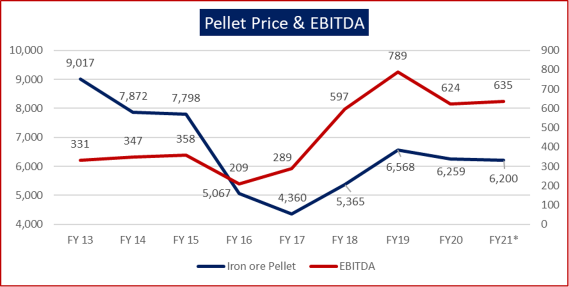

However, Godawari’s EBITDA has been going up despite stable pellet prices due to increasing value addition and access to low cost captive iron ore. Even in a weak quarter like Q1FY21, company has done annualised EBITDA of Rs635cr. So unlikely it’s EBITDA will drop below this level in future.

8 Likes

Is there any reliability in news that as main marekt of gpil is China , and in China there is some reduction in pellet prices as we’ll as demand which can affect negatively to gpil ???

1 Like

Not really, as of now GPIL supplies iron ore pellets to the domestic markets as they are able to get fairly high realisations. To my knowledge prices are stable between 8800 - 9000 per tonne and my reckoning is that it will be above the 8000 mark till december.

3 Likes

Godawri rating update:

Debt has come down to 1230 crore. From April 2020 to August 2020, the group has already repaid ~Rs. 214 crore as against scheduled repayment of Rs. 71.85 crore for FY21.

4 Likes

I think by this peace, the company’s debt will be below 1000 crore mark by the end of FY21 and debt free by FY23 - FY24.

1 Like

This is really good work by them- paying off as much debt as possible, especially when they are earning abnormally high margins in Pellets currently. Now the interesting thing to watch will be how much lower the interest rate comes off for them. Over the coming year or so, I think interest rates should come off by 150 bps from 12.5% currently. The savings on interest will surely be used to repay more debt in FY22.

1 Like

Current interest cost is 11.5, it will come down to 9.5 in three to six months time.

While we have seen strong price performance in iron ore and iron ore pellet prices. Pellet prices are till around Rs8800/t, up from Rs6200 seen in Q1. Now it appears that steel prices are all set to add to margins of Godawari. Chinese steel mills margins are touching zero and steel prices have to go up from here on.

Source: Cycle among Cycles...

2 Likes

Current pellet prices are around Rs8400/t ex works. This is reduction from recent peak of Rs9000/t.

Interesting insights in the recent update - https://www.indiaratings.co.in/PressRelease?pressReleaseID=52600&title=india-ratings-assigns-godawari-power-%26-ispat-‘ind-a-’%2Fstable

Financial deleveraging is a powerful thing. We don’t usually see cos making pre-payments continously.

Risk - there are articles of export ban/duty on pellets. If that happens, it could be a serious negative.

Disc: same as before

1 Like

Yea, it is astonishing that the markets are rallying and still GPIL tardes at 3 times EV/EBITDA with such an astonishing performance especially on the balance sheet side of things

2 Likes

No export duty on pellet exports - A big relief for Godawari, Sarda, JSPL

2 Likes

People who are tracking I think this article will help on the acquisition of the power division of Jagdamba Power and Alloys Ltd. adding the power business too alongwith its steel business as they are closely related.

Disclosure: Not invested anymore.

2 Likes

Iron ore prices in India have doubled in last 4months, still the prices are at a historical discount to global prices. Looks like still more scope to go up. Btw pellet prices ex Raipur are back above Rs9000/t.

Source: Shortages - Can be Structural...

3 Likes

CRISIL Ratings has assigned A Stable/A1 credit rating to GPILs Credit Rating. Interesting development is repayment of Rs 263 crores of term debt on standalone basis in the current FY. https://www.crisil.com/mnt/winshare/Ratings/RatingList/RatingDocs/Godawari_Power_and_Ispat_Limited_November_04_2020_RR.html

3 Likes

Few key points in the above update:

- GPIL has cumulatively repaid Rs 311 crore of term debt in fiscals 2019 and 2020 against scheduled repayment of Rs 159 crore. Company has further repaid Rs 263 crore till October 28, 2020 against scheduled repayment of Rs 55 crore for entire fiscal 2021.

- On account of accelerated deleveraging, gearing is expected to reach below 0.7 time by the end of fiscal 2021

- Management has indicated limited capex requirement of Rs 70-75 crore per annum to be funded entirely from internal accrual. These capex would largely be towards regular maintenance, debottlenecking/efficiency improvement resulting in increased capacity of long steel intermediate products along with increase in mining capacity to 3.0 MTPA from 2.1 MTPA

Source: https://www.crisil.com/mnt/winshare/Ratings/RatingList/RatingDocs/Godawari_Power_and_Ispat_Limited_November_04_2020_RR.html

13 Likes