Going through this thread I have to take my hat off to @Kumar_manas for understanding the company and the sector that it operates in perfectly. Well done sir. Also in hindsight its so obvious how cheap the company was but few will put their money where their mouth is. Another thing to note is how long the market takes to recognize the fact and the rerating to occur. It’s almost as if the market fails to recognize that a turnaround in the balance sheet has occurred and still remembers the misdeeds of the past. True test of patience but reward is sweet at the end.

7 Likes

Please continue to post. At your discretion of course. The forum is richer for it.

1 Like

@royatirek @Administrator @adminph2 @RajeevJ @ChaitanyaC

ok …so a newbie is trying to wade into. ![]()

I’ve had read last post of @Kumar_manas, where he stated that “Comparisons of GPIL Vs Sandur were repeatedly getting bumped off and claimed the reason for such posts getting deleted because certain VP administrators might have interests in sandur hence they would delete such comparisons”

Although i have not studied GPIL or Sandur but i would like to know from @Kumar_manas.How someone holding Sandur may benefit if GPIL is better placed in terms of valuation? as a newbie I am unable to understad the same.In case you may like to shed some light on this matter for the benefit of others as well.Also there are still many of your posts available on this thread. ![]()

I’ve also read @royatirek’s response, which highlighted various potential reasons for the removal of your posts. These may include automated removal mechanisms and inadvertent flagging by members.

Unfortunately, I couldn’t retrieve screenshots of those original posts.

Though i’d like to think that VP is democratic/diverse/greatly beneficial forum and its free.I thought @kumar_manas’s original post would survive but i think founders/admins would certainly have rights, only they may know the reasons (i know some of the reasons which would get post bumped off are arrogance/narrow vision/personal comments). ![]()

But i would still like @kumar_manas to continue to post.Your conviction and knowledge certainly helps. Also there are members who reads your posts before they get deleted…yes ? ![]()

5 Likes

Sandur manganese clearly cheated the minority shareholders in its rights issue- and many people on VP don’t want to get this mentioned anywhere.

I mentioned this in my previous post- and that was deleted for same purpose.

9 Likes

ok…so it was not the GPIL vs Sandur valuation comparison for which your post getting bumped off.

Because i see such comparison already present on this thread.

.

D- Not invested in either of them.Studying GPIL.

2 Likes

Your contribution to the Godawari thread is invaluable & helped many of us build conviction! Thanks a ton!!

On the rights issue… I normally apply for Five times the quantity that I’m entitled to, more so in these times of ASBA, but in any worthwhile issue, I seldom get any meaningful extra allotment. A pity that I was not a shareholder in Sandur at the time of the Rights issue or I too would have made a killing!!

But is it fair to say that Sandur cheated minority shareholders when they (minority shareholders) themselves did not apply for their rights? Ofcourse, like all of us, you too are entitled to your opinion.

8 Likes

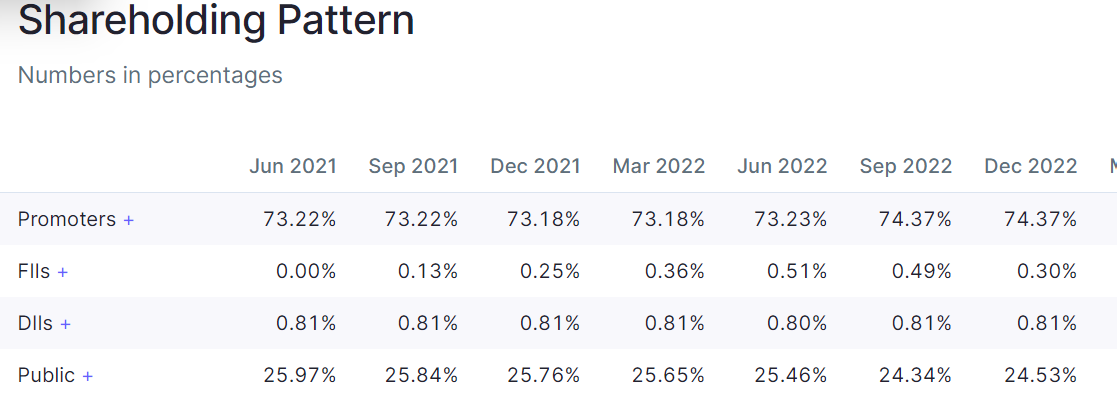

they (promoter) of course applied to rights- otherwise their shareholding would have reduced by huge margin.

rights issue was nominal at Rs. 10 or something, when share price was in thousands.

Post rights issue-

the shareholding of promoters increased from 73.23% to 74.37%

1.2% were free of cost shares- snatched from sleeping/inactive retail shareholders- who didn’t apply to rights shares.

they got these shares for FREE. as rights issue was at Rs. 10 only, while actual share was at Rs. 2000 or something near it.

The sleeping shareholders- who didn’t apply for rights issue- saw huge wealth erosion.

It is understandable not 100% of retail shareholders are active in markets.

Many are senior citizens and check their portfolio once in a year.

The purpose of rights issue was only to snatch their shareholding- and increase promoter shareholding.

Please check price of rights issue, price of sandur stock (before split/bonus), amount raised from rights issue.

19 Likes

No one stopped retail from applying to rights issue. Unless the company mis-represented info, this could be opportunistic thinking, but not illegal. so, repeatedly calling this cheating in a public forum, on THIS basis - may be the reason those posts were flagged/removed. your posts are valuable, so i’d suggest to continue posting, and if you want to compare, please focus on qualitative and quantitative comparison. without calling this rights issue a cheating. would benefit everyone.

2 Likes

I agree here. had the right issue been close to market price, it would not be called cheating but right issue was at 10rs. The purpose was not to raise fund. they could have given bonus shares or even could have done stock split.

In my opinion, the practice was not ethical as promoters gained from inactive shareholders who did not apply. Cheating would be a strong word but for sure it was an unfair mean used by promoter to increase their shareholding.

Also I feel that the stock price is manipulated for Sandur though I dont have any means to confirm that but the huge fluctuations in share price doesnt give me comfort.

P.S - I am a shareholder with small capital in both GPIL and Sandur. However, I have reduced my stake in Sandur and have increased stake in GPIL in recent months.

13 Likes

Any posts regarding Sandur should be posted on relevant thread.

10 Likes

Good results considering that there was considerable industry chatter about weak pricing in some segments.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/74f0e253-9c0d-4d56-8e09-d2b171824677.pdf

Link to presentation -

6 Likes

Q4 Concall highlights

| Products | FY’24 Production | Fy’25 Guidance | % Change |

|---|---|---|---|

| Iron Ore | 2.3 | 3 | 30% |

| Pellets | 2.6 | 2.44 | -6% |

| Sponge Iron | 0.59 | 0.594 | 1% |

| Billets | 0.475 | 0.5 | 5% |

| Ferro Alloys | 0.08 | 0.08 | 0% |

| Rolled Products | 0.2 | 0.325 | 63% |

-

Shareholder Payout

Buy Back worth 200crs

Dividend of 125crs -

Total Capex in FY’25 700crs & FY’26 1000crs:

Power 63crs (this will help reduce the power cost)

Beneficiation 176crs (this will save transportation cost for the company)

Pellets 568crs (should be done by Q1’26)

Steel Plant 6000crs (this should start after getting Environmental clearance (EC) will happen over 3 years time) -

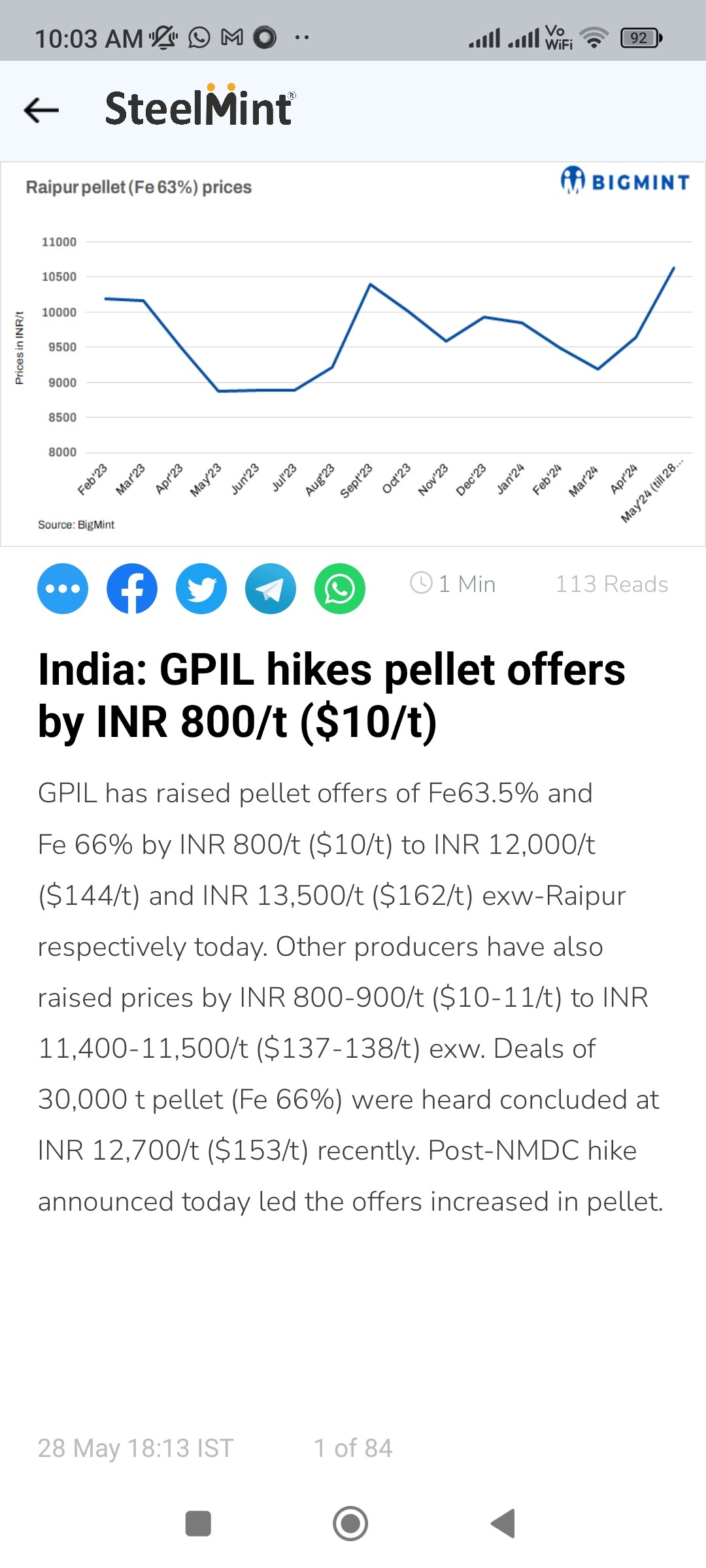

Product prices have gone up 10% since Holi on an average. Pellet Prices have gone up from 10.5k/t to 11.3k/t for industrial grade pellets & higher grade is selling at 12.5k/t. Company presently has a 50:50 product split.

-

Post the capex in mines & pellets the product mix will change in favour of high grade pellets (75:25). Company expects mining output to increase from Q4’25. Higher grade pellets are at a prem of Rs 1000-1500/T to Industrial grade pellets.

-

Cost price advantage due to older royalty is Rs 3400/tonne.

-

Demand for pellets will remain strong due to DRI capacity coming on stream in a few months time.

-

Ferro Prices have gone up and are likely to sustain at higher levels due to disruption in Australia’s South32’s mining operation. It will take 18 months for the supply to flow back to the market.

-

Currently only one mine is operational and all the capex will is happening at that mine. The company has stopped production at the second mine due to inferior output. Company is planning to set up a beneficiation plant at the second mine site. They have already started the EC process. The production from the second mine should start in FY’28.

My Two bits:

- For GPIL iron prices are the most important factor that we should track. FY’26 will be a great year for the company as it will be able to double its pellet plant.

- Biggest advantage that this company has is the mines under the old scheme. This leads to a cost advantage of ~Rs 3000/T and if the price of Iron Ore goes up the advantage will only increase.

- Company should post a EBITDA margin>25% (company has guided for 24-25%).

- Revenue for FY’25: 6000-6200crs & EBITDA ~1600crs.

- FY’26 should be a breakout year for the company.

- Capex can be easily funded through internal accruals.

- Company is looking to move up the value chain by setting up a HRC plant (Steel Plant) of 2MT.

- Mines auctioned under the new royalty regime will also start coming on stream in a couple of years time.

- Company is likely to keep rewarding its shareholders through BuyBacks & Dividends in the future despite higher capex.

Disc: Invested

13 Likes

Q4 EBITDA margin was 22%. Prices are up from that base line.

Sponge Iron has still not recovered.

Its prudent to be conservative and build your investment case, isnt it?

3 Likes

Dear Members if possible please share your feedback.

I think the best way to track GPIL is keeping a tab on the iron ore prices. All the other forward integrations measures (Integrated Steel Plant) will take time to fructify. Till then we need to just focus of Iron Ore prices and capacity additions.

Ive also tried to draw a comparison between the two other iron ore miners under the old royalty scheme based on FY’24 numbers. PFA the comparative table below:

| GPIL | Lloyd Metals | Sandur | |

|---|---|---|---|

| M.Cap | 11994 | 34863 | 8761 |

| CMP | 882 | 690 | 541 |

| Sales | 5455 | 6522 | 1252 |

| EBITDA | 1328 | 1728 | 320 |

| EBITDA % | 24.34% | 26.49% | 25.56% |

| PAT | 936 | 1243 | 238 |

| PAT% | 17.16% | 19.06% | 19.01% |

| Net Cash | 1056 | 265 | -74 |

| EV | 10938 | 34598 | 8835 |

| EV/EBITDA | 8.24 | 20.02 | 27.61 |

| P/E | 12.81 | 28.05 | 36.81 |

| Net Blcok | 2364 | 1235 | 886 |

| CWIP | 430 | 1268 | 116 |

| AssetTurn | 2.31 | 5.28 | 1.41 |

| RoA | 40% | 101% | 27% |

| Equity+ Reserve | 4496 | 2811 | 2157 |

| RoE | 21% | 44% | 11% |

| IronOre Capacity (in MMT) | 3 | 10 | 3.81 |

| IronOre Prod (in MMT) | 2.3 | 9.7 | 1.97 |

| Production Guidance | 6 | 55 | NA |

| Lease Expiry | 2057 | 2057 | 2033 |

Sandur also has manganese ore which is on a high these days.

Lloyd has crazy expansion plans.

GPIL is the cheapest company out of the three.

16 Likes

Somehow the no’s of LLoyds seems not comfortable, the CFO/EBITDA seems very high and atlease from screener, they are not paying any direct taxes. not sure why

1 Like

Pursuant to Regulation 29(1 )(b) of Securities and Exchange Board of India (Listing Obligations and

Disclosure Requirements) Regulations, 2015, as ainended, it is hereby infomed that, a meeting of the

Board of Directors of the Company is scheduled to be held on Saturday, June 15, 2024, inter alia, to

consider a proposal for buyback of fully paid up equity shares of the Company of face value of €5

each as well as matters related/incidental thereto, in accordance with the applicable provisions under

the Companies Act, 2013 (including the rules and regulations framed thereunder), the Securities and

Exchange Board of India (Buy-back of Securities) Regulations, 20189 as amended, and other

applicable laws.

Godawari Power Buyback.pdf (417.6 KB)

It will be pertinent to note at what price management value GPIL.

8 Likes

GPIL has announced a buyback price of Rs.1400 with record date as June 28, 2024 and amount not exceeding Rs.301 crores.

Godwari Power Buyback.pdf (1.8 MB)

12 Likes

Since the announcement of Board meeting for buyback, this stock has ran up quite a bit, despite softening of pellet / iron ore prices. May be it was due to the fact that it was discounted cheaper compared to peer group shared. But after the announcement of details, there is no further trigger in the short term. Also only 1.6% of paid up shares will be bought back. So acceptance ratio for retail shareholders in a optimistic calculation can’t be more than 3 %. So in my opinion, if it opens gap up on Tuesday, one should sell. I am sure we will get lot of opportunities to buy it at lower level.

NB- This is my opinion and I may be wrong.

9 Likes