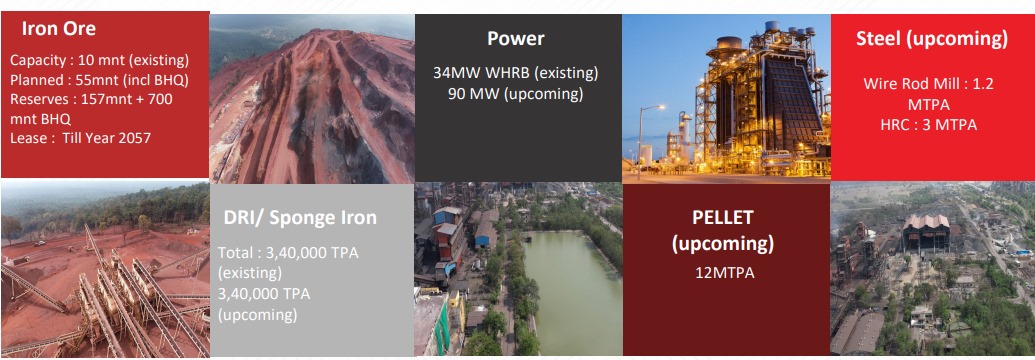

Company got enviornment clearance for expansion of Iron Ore pelletization plant from 2.7 MTPA to 4.7 MTPA

The entire project cost of expansion shall be met out of internal accruals of the company and the commercial operation of the expansion program is expected to be commissioned in Q1 FY26.

the part of using internal accruals to fund their expansion is what makes me happy, as steel cyclicals tend to warp the earnings a lot. This should be able to keep their PAT numbers up in a downturn as their interest outgo wouldnt be that much

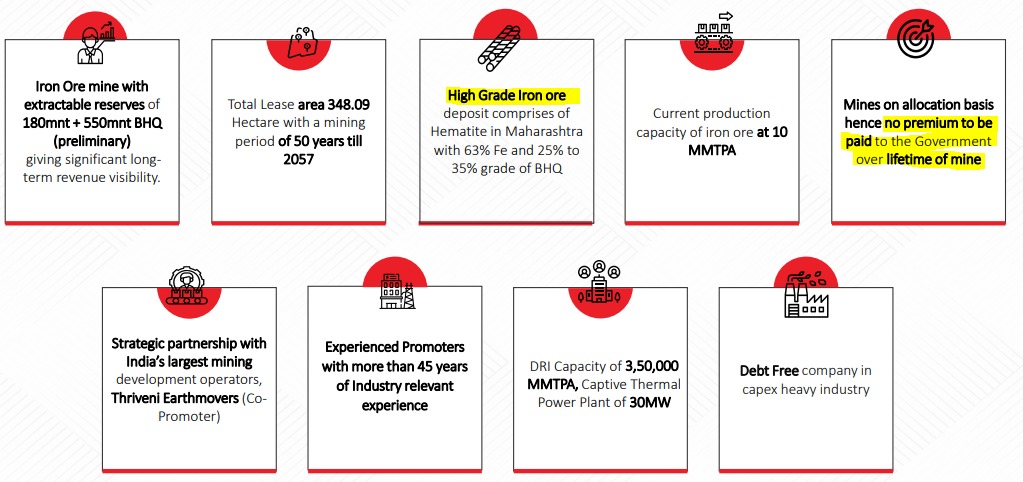

GPIL has 0 royalties premium to be paid on Iron ore mines. As it is in the old mining regime. Likes of Jsl and JSPL have to pay through the nose at these auctions, and continue royalties which are at 100% Premium. Which gives a natural advantage in being a low cost producer.

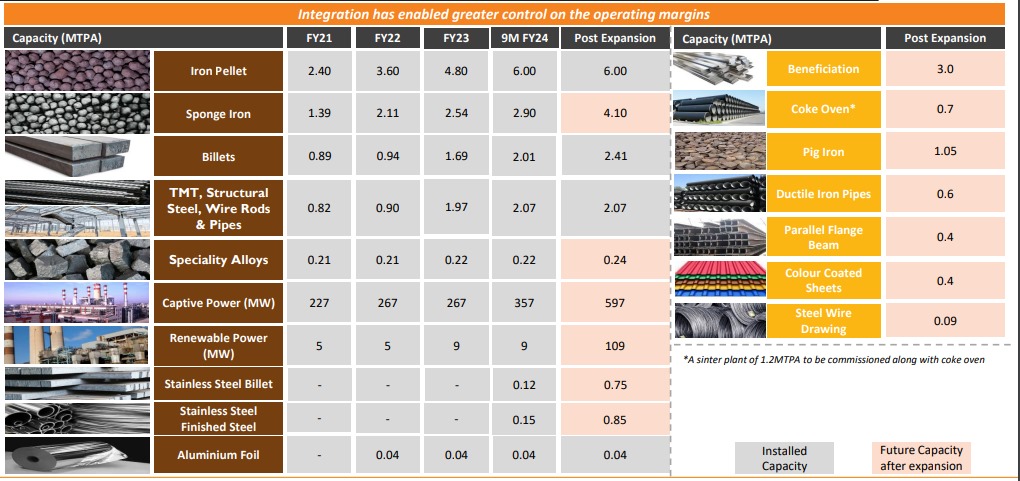

Ebitda per tonne will likely be close to 10,000 rs and at peak this capex can add 1800 crores of Ebitda assuming 90% Utilisation of the steel plant.

The biggest risk for this company is iron ore prices…which are at very elevated levels. A 20-50 dollar fall in price will have very adverse effect on its profitability and cash flows.

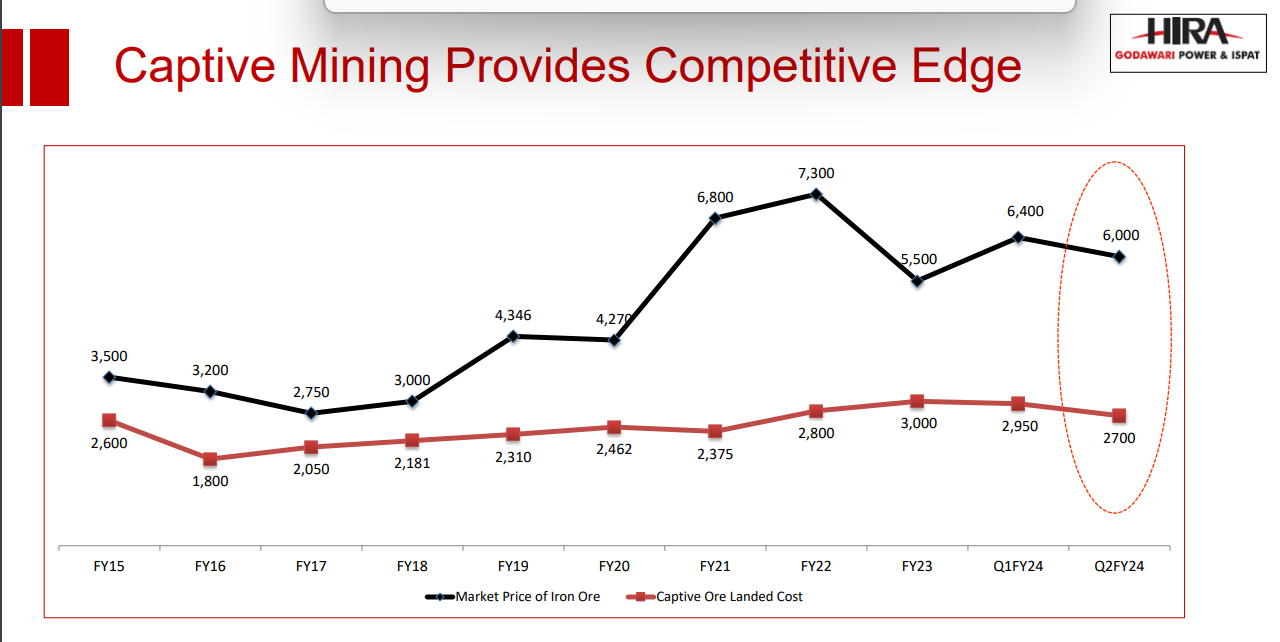

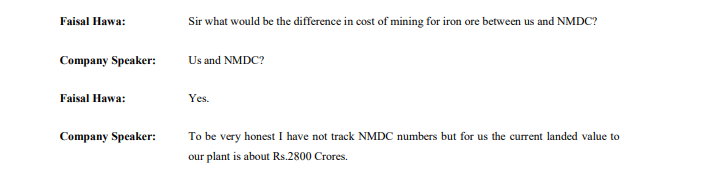

Any fall in the prices of iron ore will have an impact, but for mine owning companies like Godawari, the impact is that much less as its landed cost is much lower than companies that don’t have captive mines.

On the contrary, economic impact is very high. If iron ore cost decrease, RM cost for other players will decrease disproportionately to GPIL. Where as, higher iron ore prices and lower landed costs of iron ore boosts (gross) margins for GPIL.

Perhaps I did not put my point across properly. The price differential between the landed cost of captive iron ore & its market price amounts to the extraordinary profits that mining Co.'s like Godawari are assured of. Over the last several years starting 2018, which include the Covid years, the average operating profits of Godawari has been around 24%. Unless there is a drastic/ unprecedented fall, by & large mining Co.'s have enough margins to absorb the shock. Further, if there is indeed such a fall, then iron & steel prices too are likely to fall drastically, thereby wiping out profits for the steel companies. My limited point is that captive mining Co.'s in India with long mining leases still to go are better equipped to handle volatility.

Yes sir. and in that case, in 2nd order effect, companies like GPIL can benefit. Other companies may start facing solvency issues. Bankruptcies may get triggered. Capacities may get destroyed, temporarily.

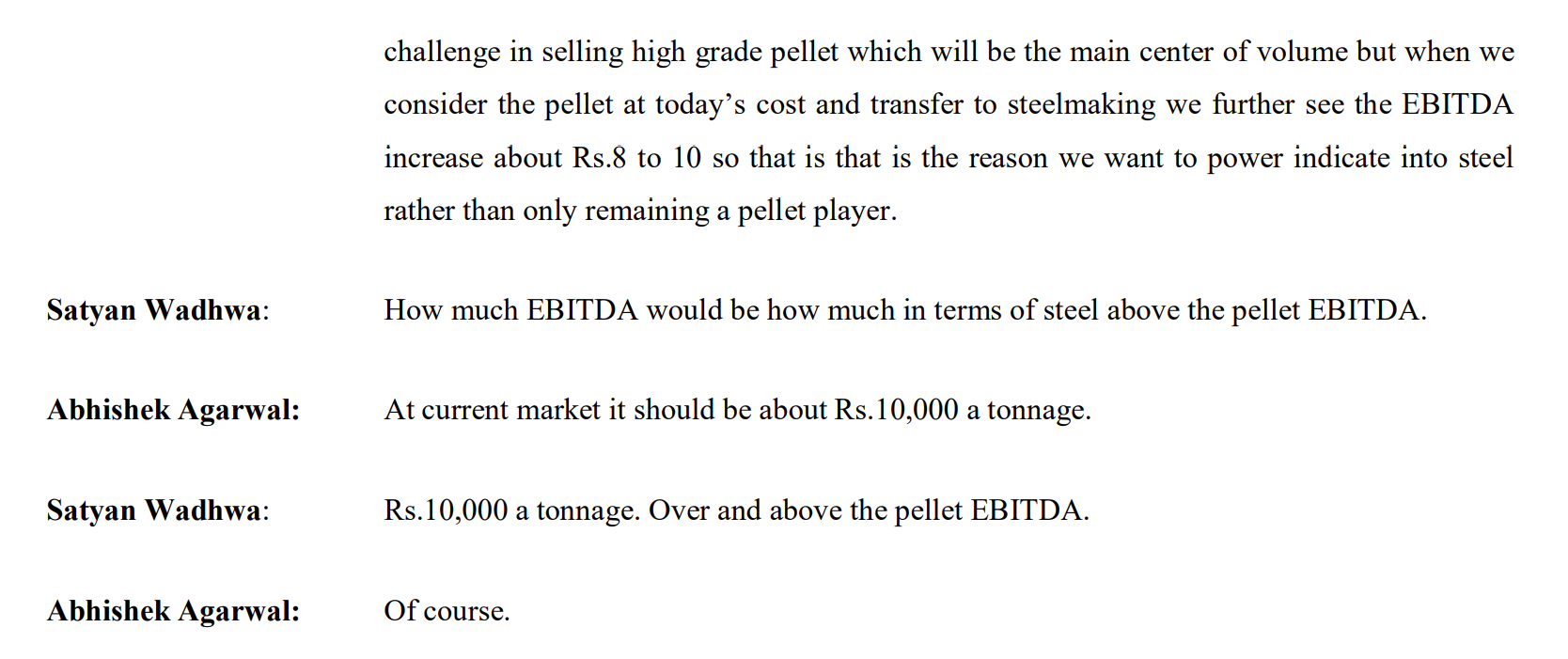

I guess Peak EBITDA could be more higher, as per concall they would be having EBITDA of 10,000 rs over and obove pellet EBITDA, Pellets EBITDA is nearly 4,000 rs

So EBITDA from steel could be nearly14,000 Rs

Assuming peak utilisation of 90% capex can add near to 2500 crores

@Worldlywiseinvestors any idea on how much time they will take to reach peak utilisation for this integrated steel plant?

Wanted to understand views of all who are tracking this story in terms of oversupply that may come because of the capex that many other companies are doing?

Llyods doing capex for pellets and HR coils (long products) and GPIL is also doing similar capex. Moreover the quantum of capex for Lloyds is quite high as compared to GPIL. Also if we look in terms of the quality of iron ore, premium to be paid to gov. etc Llyods is pretty similar to GPIL (I know it trades at twice EV/EBITDA multiple as that of GPIL).

Shyam metalics is also expanding (though they are getting into low value products like pig iron, DI pipes, colour coated sheets, Steel wires). Some of these products like Steel wires are something GPIL is currently producing so there could be some competition in existing products.

Last but not the least, all these players be it Lloyds, Shyam or Sarda , everyone is talking about integrated nature of business and everyone is also setting up power plants for captive consumption.

So the question is, if everyone is expanding their capacities, is there enough demand to absorb this new supply coming? Exports could be additional avenue but Gov. policies could spoil the game here.

Dear Manas, @Kumar_manas

Its been long since you posted here. Hope you are doing great.

You are the person who has the highest conviction and with highest allocation (I think close to 60% of your postfolio) in this business. We all now can see that you were spot on… Some of us gained from your continuous post on this thread. Unfortunately, for me I could not hold on to it at a time where I though that it would come down for some time. So I sold and waited for correction, which eventually did happen, but I wanted more correction… you know, the ‘greed’ and it started the upward journey. I could not catch it again. Which again was a great mistake as even if I could bought it 50% more than my selling price, I would have been still a winner… anyway this happens I guess.

So, thank you. It would be really great if you could share some of your current thoughts on GPIL.

It doesn’t matter much in overall scheme of things. India needs close to 200mnt of iron ore and that demand is growing at 7-8% so around 15-16mnt per year. Despite all these expansions, iron ore supply won’t over run the demand. Secondly, most of these companies are integrating into steel and steel can be exported in worst case. Here too the key driver of steel price is China’s exports. The key differentiation will come from cost of production.

Growth prospects are still very much attached. Opportunity is not lost in my view. Company can do fairly well from here given the capex from internal accruals and premium product (iron ore FE content 66%) versus others producing lesser FE content iron ore.