Hello everyone hoping it helps,

Its March news… already discounted for if you are looking at a price POV

Hi Manas, Thanks for the brilliant insights. Stupid question here, can’t Tata Steel renew their lease?

It will go in open auction. Anybody can bid and anyone can win.

JSW can take Tata steel mines if the bid of JSW is higher.

This is what happened in Odisha mine auctions.

1 Like

Could you please explain how GPIL would benefit, considering that their lease is scheduled to expire in 2055 while Tata’s lease ends in 2030? Especially given Tata’s ability to renew their lease.

It will be helpful, if you can do SWOT analysis of steel and mining industry and share it with us.

Thanks

1 Like

2 Likes

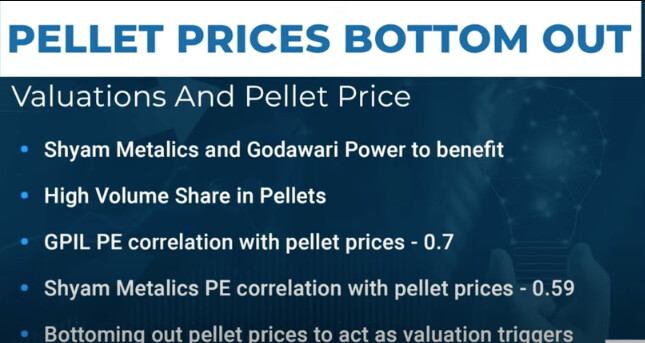

This is ideally the fundamental trigger ex the High/Low PE for GPIL

Godawari Power and Ispat Ltd (GPIL) has launched a new grade of pellets comprising iron (min 66%), alumina (max 1.1%), silica (max 3.25%), phosphorous (0.02-0.025%), and sulphur (max 0.01%) at a price of INR 11,200/t exw-Raipur. Currently, the company is holding back sales of Fe63% pellets while other players are offering at INR 8,900-9,200/t exw. GPIL’s pellet production stood at 2.62 mnt in FY23, up 9% y-o-y.

2 Likes

So, will margin become higher in coming years?

That means, it will no longer be a commodity company?

Should we give specialty valuations like 30-35 PE for debt free specialty cos?

2 Likes

Investor Presentation for the Q1-FY24

Result for Q1-FY24

1 Like

Basically, GPIL’s first meaningful capex is at least 15 months away (assuming they get env. clearance today). The performance will be largely driven by realization dynamics. In domestic market the demand scenario appears decent given the growth outlook for India. For international market, it will hinge on growth pick up in China which most of the analyst are betting on. Good to see that even in challenging environment GPIL came up with decent improvement compared to the last quarter. But it seems that the stock price will be driven by prices for its products in international market.

4 Likes

Demand for Iron ore may slow down due to cooling of real estate market in China

8 Likes

GPIL NOTES.pdf (2.7 MB)

Gpil Notes

22 Likes

Sandur Manganese, another iron ore mining company has been on a tear ever since it announced getting the approval for capacity enhancement, something that was already on the cards & it was more a matter of “when” & not 'if". Todays announcement of a liberal bonus issue of 5:1 has further added fuel to the stock rally. I am decently invested in Sandur as well & am delighted with the way the stock has behaved in the last month or so. Also, I continue to hold my full quantity.

The purpose of this particular post however is to put forward the view that the valuation differential between Godawari & Sandur has become glaring & there does not seem to be any justification for this. In fact, Sandur aspires to be in five years where Godawari Power is today! Sandur is still in the process of forward integrating from ore into value added products where as Godawari has already done so & is not selling any iron ore. Godawari is much bigger in terms of scale & is in the process of more than doubling its capacity from 2.35 MnT to 6 MnT. As per the mgt commentary, this permission is expected by March '24 & the increased capacity should go on stream in about 15 months. Despite more than doubling its mining capacity, Godawari is not planning to sell any iron ore & is confident of simultaneously increasing its palletization capacity.

To me the Company seems to be an mis-priced bet, more so, admittedly, after the recent run up in Sandur. I repeat, that Sandur is a wonderful mining Co. with a history of great corporate governance & its valuations are well earned. My limited point is that both Co.'s own iron ore mines, which clearly is their biggest strength & being a bigger Co. & a more efficient user of capital, Godawari’s valuations leave a lot of scope for improvement.

A comparison of the two companies is given below:

Peer comparison

| Godawari Power & Ispat Ltd | Sandur Manganese & Iron Ores Ltd | |

|---|---|---|

| Market Cap | 9,669 | 6,871 |

| Current Price | 710 | 2,545 |

| High / Low | ₹ 726 / 307 | ₹ 2,546 / 695 |

| Stock P/E | 12.4 | 24.4 |

| Book Value | 297 | 735 |

| Dividend Yield | 0.56 | 0.20 |

| ROCE | 27.5 | 18.4 |

| ROE | 22.3 | 14.7 |

| Face Value | 5.00 | 10.0 |

| Debt to equity | 0.02 | 0.07 |

Disc: Invested decently in Godawari Power!!

43 Likes

I too am invested in both GPIL and Sandur manganese. However, I have cut down my portfolio sizing in Sanduma yesterday ![]()

I am not able to comprehend the valuation gap between the two.

Infact by my limited understanding, GPIL management seems better than Sandur. Rights issue of Sandur was not in the right spirit in my opinion.

Yet the market is very buoyant about Sandur. The valuation of Sandur are out of my comfort zone.

Any insights as to why we have this valuation gap?

Any reason we should doubt the integrity of GPIL’s management?

Discl. - Increased my portfolio in GPIL in recent days and months.

10 Likes

@Rakesh_Arora Sir can you provide your expert comparison between Shyam Metallics and GPIL at current valuation ?

2 Likes

Can any one guide on what would be the Revenue per tonne and EBITDA per tonne for Billets, Sponge Iron and cast iron?

1 Like

Company shares Realsiation per ton for all products. For EBITDA per ton, you will need to make lots of assumptions

5 Likes

Amit both Shyam Metallics and GPIL have very different business model and profit drivers. GPIL profits are largely driven by iron ore prices while Shyam Metallics is driven by conversion margin and value addition. Will post more details once we have done more detailed comparison.

22 Likes

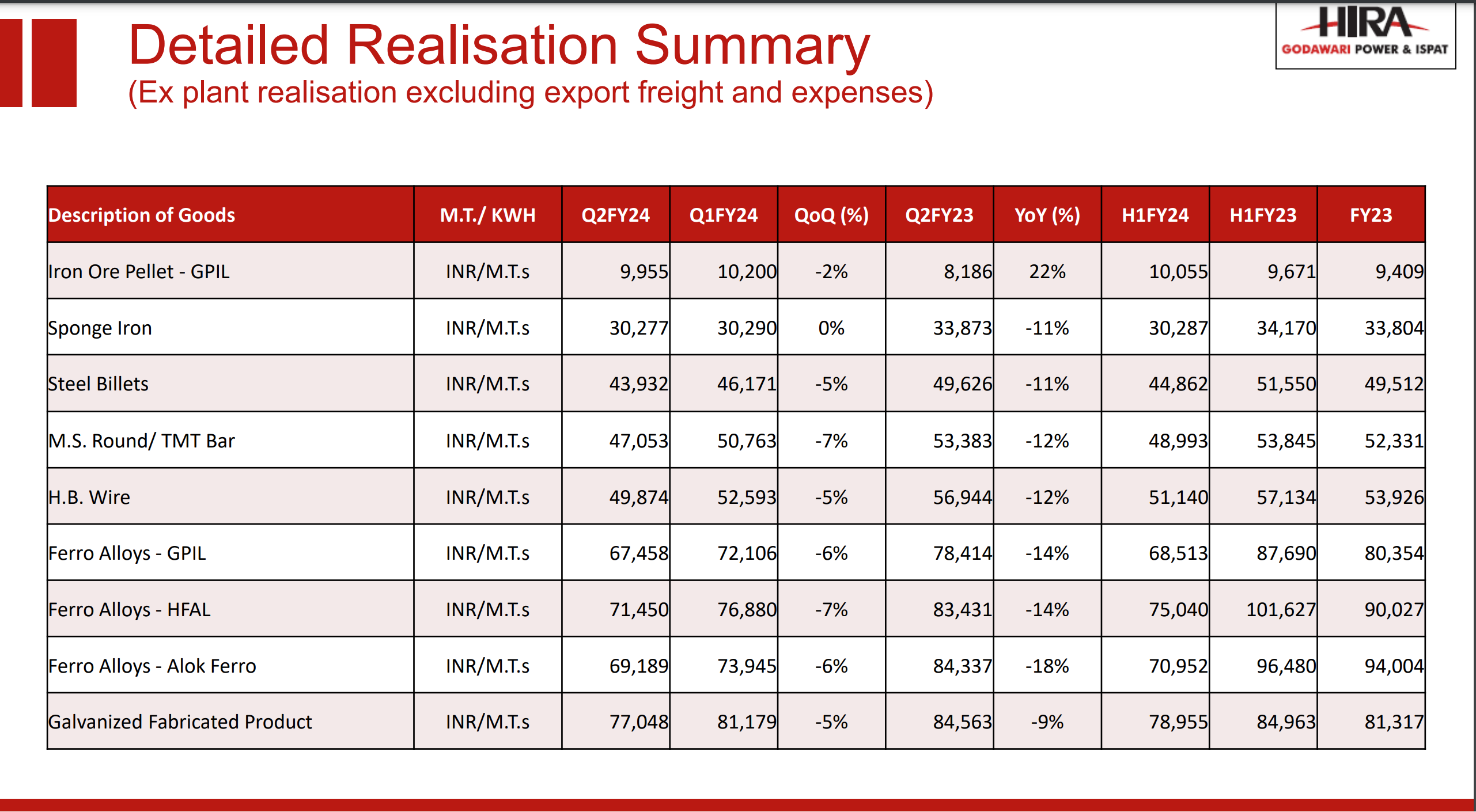

Decent set of numbers from GPIL. Investor presentation below

2 Likes