Yes, pellet prices have been soft. And if they fall further the earnings can get materially hit. And this is the reason why market is giving such a low multiple.

What I was talking about in the above post was that there is a good premium to higher grade of pellets if the co is successful…so we need to keep a tab on the same.

3 Likes

While the pellets prices have softened, the international prices are still in the territory of 110-105$, which is not too bad. Further, the tax cuts can enhance the cash flows by about 35-40 cr, which can be used to repay debt.

Regards

SJ

1 Like

power related debt will continue to be overhang no !!

Borrowings have decreased by 10% in 2019 compared to 2018.

Interest pay out has decreased therefore.

By 2021, Reserves will equal borrowings, at the current rates.

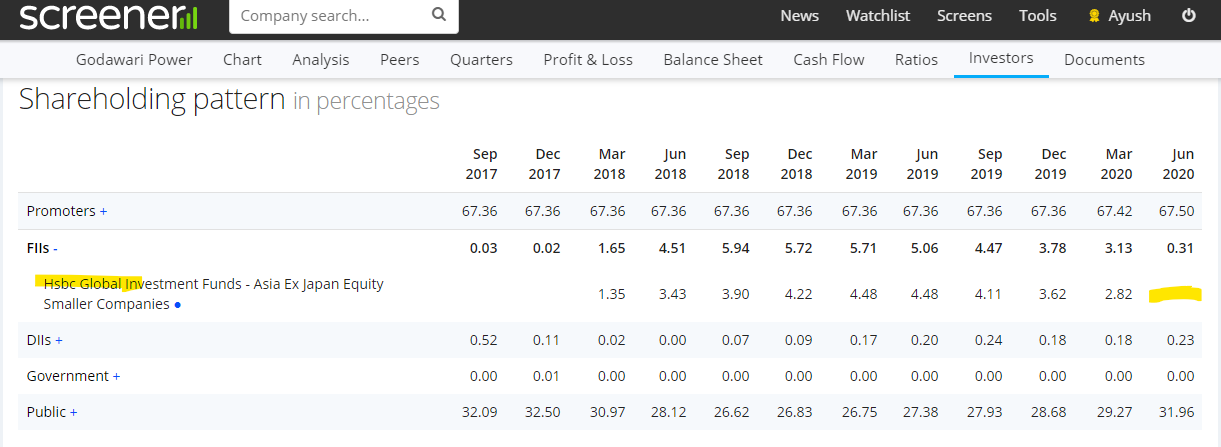

FIIs have made entry in March 2018, bought upto 6% by Sept 2018 but have decreased now to 4.5%.

Sources:

https://www.screener.in/company/GPIL/consolidated/

https://trendlyne.com/equity/share-holding/486/GPIL/latest/godawari-power-ispat-ltd/

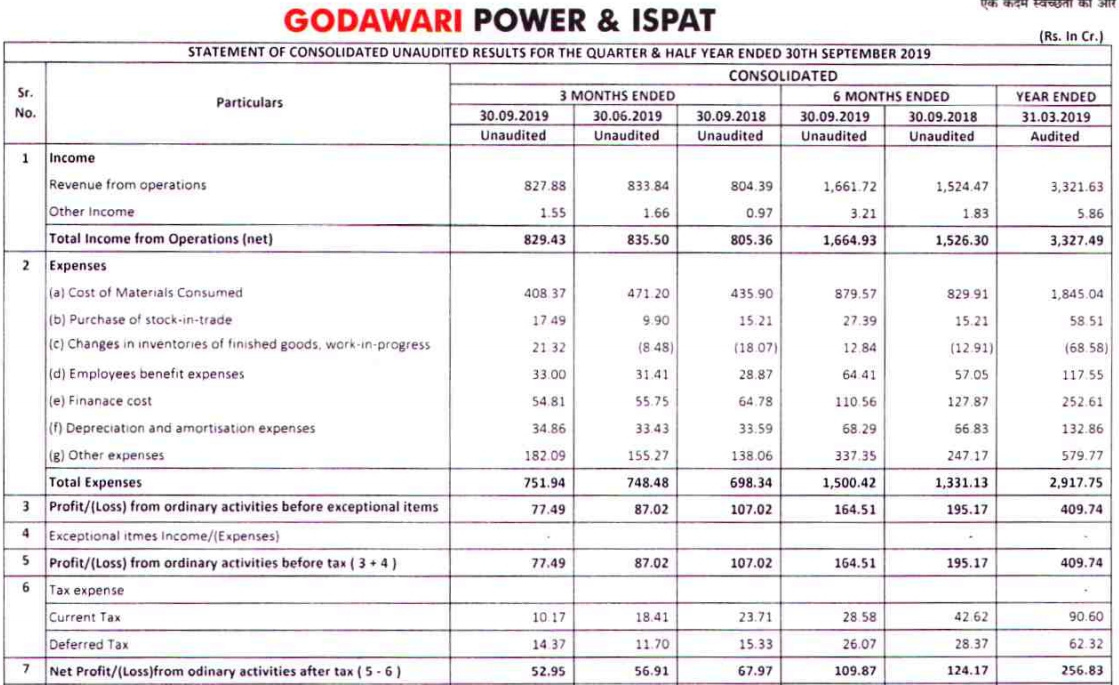

The realizations from pallets have remained stable, while billets and other products have been impacted a little. However, overall consolidated EBITDA margin has fallen to 20.2% for the quarter, which is still decent. FCF for 6M-FY20 is Rs. 211.7 cr The entire debt scheduled in FY20 of ~Rs. 100 cr has been repaid in 6M. With the current trajectory, they should be able generate FCF to repay debt maturing in FY21, which is another Rs. 100 cr. Overall things look stable. Here is the link to the investor presentation.

Regards

SJ

Yes, importantly, they have maintained they will continue to pay off debt (they have been paying off debt in last two years). Overleveraging has been a common mistake by these small steel players.

Few catalysts hereon: 1) Iron ore auction to push up iron and pellet price - Godavari has iron ore mine for 50% of its 1.8 mtpa pellet capacity and hence will benefit if this event plays out well.

2) With deleveraging, interest cost likely to come down to 11% from 12% in the near term.

3) Contracts with Japanese companies for export of high grade pellets could improve their margins.

4) Overall, it trades at cheap valuations on depressed earnings (EBITDA of 500 cr) and when cycle turns EBITDA could be 800-900cr. Market cap of 850 cr and intention to pay off debt of 1700 cr currently looks good from a 3-5 year perspective.

1 Like

Iron ore pellet prices have remained steady at about 100$ and Vale closure may push the prices higher atleast in the short term. GPIL has made a disclosure on COVID-19, which is painting a bright picture for the rest of the year. While we all should take it with a pinch of salt, the progress on debt repayment during the COVID period and decision of not opting for moratorium is encouraging. Views invited

Disc: Invested in Godawari Power

2 Likes

Interestingly the international iron ore prices continue to remain strong and are making fresh highs :

This bodes well for GPIL. As per the recent concall, they have ramped up pellet exports to China.

It has been good to read the recent concall transcripts and it seems management has been walking the talk and repaying debt consistently. Despite uncertain times like Covid, the management remains committed on debt repayments if things don’t change materially going forward.

The investor presentations of the company are good and informative. They have been emphasizing that their sustainable EBIDTA is 500Cr+ as they have scaled up production on their mines substantially over last 5 years, yet the stock is at 600 Cr MCap (right way to look at is EV which is 2200 Cr but I wanted to highlight the low market cap as they have been repaying debt)

Another interesting thing to observe in shareholding patter is that HSBC (they had bought during good times and were holding close to 5% stake) seems to have exited in recent quarters and the same seems to have been absorbed by market

Any other insights/strong negatives on this? One negative is that they have a solar plant in their subsidiary which has a long term contract with government at a high price. The company is making money but there might be some risk.

Disc: Invested in family accounts and PMS

6 Likes

I do not have insights, only some stray thoughts:

-

Ore prices have been elevated since Feb 2019, and GPIL has done worse in past 1.5 years throughout the period prices have been quite elevated. (and Vale incident combined)

-

Ore prices have climbed recently since mid-April 2020, this could just be China starting up before the ore producers have supplies in place. So, a temp bump likely. Overall, demand may be on the lower end for this year perhaps.

Quality company definitely, worth the wait, depends a bit of course on luck of course.

Disc: not invested, interested.

Very good Q1FY21 results - margin maintained despite lower volumes as pellet prices were strong.

Now, assuming this company pays off Rs300 cr in FY21 and another Rs400 cr in FY22, its market cap will nearly double. Further, lower interest cost and deleveraging will re-rate the stock. Lastly, steel cycle is currently weak, if it picks up and GPIL does 900 cr of EBTIDA stock could be Rs700-1000 in two years. Lets see

Disc: Invested

5 Likes

I am impressed with the disclosure level of the Company and the details which they give in Investor presentation. The management routinely interacts with its investors through concall. The Company has impressively reduced its debt and is continuously following that path and utilising all its available cash flows for reducing its debt.

What an impressive performance, the Company was earlier A rated by rating agencies then it defaulted in its payment and was down graded to Default rating D, now again at BBB+ and steadily moving towards A again. Truly a turn around story. This proves the reliability and Corporate Governance of the management. Very few companies in Small cap which have shown such an exemplary turn around performance.

The management due to there loan default and restructuring in the past seems so wary of debt that they want to get rid of this necessary evil at all cost and therefore if we go through the investor presentation the Core idea seems to be debt and the entire focus is to only reduce the debt. It is to the extent that in some case they have prepaid the due for entire year in advance in the month of August itself.

I would rate the management 10/10 on a small cap parameter.

One may loose money in this counter due to genuine business failure and cyclical nature of the business, but not because of siphoning of Money by the promoters’

Disclosure: 5% of my portfolio added around 8 months backGPIL INVESTOR PRESENTATION Q121.pdf (1.4 MB)

6 Likes

Interesting management interview

8 Likes

The latest concall transcript is a very good read - https://www.bseindia.com/xml-data/corpfiling/AttachLive/7d9fd452-a868-4e88-8111-35999d545327.pdf. Good example of combination of financial de-leverage in play.

As mentioned earlier, good to see strong emphasis from management on remaining disciplined and making strong debt reduction. They have been walking the talk till now and if the current tailwind broadly sustains, I feel, the company may surprise and create value.

Ayush

Disc: same as before

11 Likes

From the transcript, I understand that China is an important market for GPIL. Is there a risk of their business with China due to ongoing tension between the two countries, sentiments of avoid Chinese companies, what if GPIL customers from China start buying from elsewhere. Is that really a possibility and risk, if yes how big can be the impact.

Second, their debt reduction plan seems to depend on prevailing higher pallet prices. What if pallet prices cool down earlier than expected? Will they still be able to reduce debat by 300 crores

Some of your concerns are valid. Firstly on China, trades are smooth as i understand from my channel checks. But GPIL is trying to de-risk itself by trying to tie up with Japanese and middle East companies for high grade pellets (Fe conent of 65%).

On debt repayment dependent on pellet prices- its quite true that 50-70% EBITDA comes from pellets. So in case pellet prices fall, that debt repayment can come down to Rs200-250 cr. In good cycles, they can pay off Rs400 cr. But its is noteworthy that their interest rate is high at 12% and interest cost of Rs200 cr could easily be down by Rs50-80 cr over two year period as their ratings improve with lower and lower debt. Not much capex they aim to do.

1 Like

Prices of Pellets have increased to Rs. 8,500 in domestic markets and GPIL has increased its exposure to domestic markets. Due to increased prices in normal grade iron ore pellet they have delayed the export of high grade pellet as the premium not lucrative at this point. Also seems like they repay above 100 crores o debt this quarter.

Looks like that Q2FY21 might be one of best quarters in the history of the company.

Disclosure : Invested.

5 Likes

Hi Raj,

Thanks for the info. What is the source of this info? “Also seems like they repay above 100 crores o debt this quarter” (assuming you mean fy21Q2)? In concall, if i remember correctly they said they paid around 70 crore last quarter.