No, it doesn’t sell Iron ore

Can you please confirm where do you see 1000 crore cash balance by mid-term results? I couldn’t find it in screener or in the presentation

1 Like

Very good results from the company considering the big negative development due to export duty.

The most commendable thing is the volume growth they have been able to deliver despite the big negative development due to export duty.

Concerns that I could think of:

- Realisation was about 11,500 for this qtr. Export duty came in around end of may and hence the fall in realisations would be visible in Q2. Given the scenario today, fall would be steep of 20-25% and perhaps net profit will fallen even more.

- Given the export duty, I think GPIL will now go for integrated steel plant so the large capex outlay will start.

- The export duty was very steep - personally I feel govt has made it clear that they don’t want to export natural resource - iron ore to promote steel making in India. I don’t think the export duty will be rolled back fully…it will be probably reduced to 20-25%. If so, it’s a long term negative.

I have been a huge fan of GPIL however the govt move to impose such a steep duty was like a black swan event to my mind and I sold quite a bit of my position ![]()

Disc: invested with a small allocation, sold over last few weeks.

8 Likes

Not really, the duty was imposed only in last month of Q1, and still pellet sales was down by around 20% because they knowingly used pellets more for internal consumption.

My guess is pellet sales from Q2 onwards will be 30-40% less vs normal quarter- as pellets will be used for internal consumption to make higher value added products.

The prices of value added products like billets, wire rod haven’t fallen at all. The fall is nominal at best.

5 Likes

Duty was imposed on 22 May.

Sadly GPIL can’t increase forward integration to use pellets more inhouse for steel making as they have been running at full capacity for sometime and don’t have EC clearance for further expansion

3 Likes

I think you are missing the fact that only 28% of total sales in Q1 was pellet sales despite the fact that 60% of Q1 did not have any export duty.

in Q2, only 24 or 25% will be pellet sales.

If only 25% of total revenue is pellet sales, and pellet prices are down by 25%, iron ore cost is also down by 25% (royalty will come down), how will net profit fall 20%?

Can you please throw some light here?

Value added products were 72% of sales in Q1. I would rather focus on prices and cost of those 72% (majority of sales), than the price of minority sales (pellets).

Once they get EC approval for sponge iron capacity expansion (can come any day now), sales of value added products will increase to 80% of total sales.

2 Likes

I’m going to ask this question in the conf-call if I get the opportunity. In Q1 billets production was 93,470 tons out of rated capacity of 1L tons/Q (~93+% utilization). Probably another 7% billet capacity is available as they’ve paused billet expansion too. As far as my understanding goes wire/TMT rods which is the next value-added product is produced from billets.

Sponge iron expansion may give them more profitability (sponge iron realization better than pellets), but won’t solve the next stage billet bottle-neck for value-added products.

1 Like

GPIL cannot get any further EC approval for additional Sponge Iron Capacity as advised by Management because the present unit is located very near to Raipur.

1 Like

that is after the current approval. Sponge iron capacity has already been expanded from 0.5 to 0.6, but EC approval is pending.

Even without this approval, Pellet sales is only 28% of Q1 sales.

I am not sure why is everyone so focused on 25-28% of total sales.

Should we not pay more attention to 72-75% of total sales?

3 Likes

I got the opportunity to ask if current billet capacity is a bottle-neck for downstream products. Couldn’t hear well fully but understood that the company can expand billet capacity in 3 months if needed. And they’re going to concentrate on wire rods which is a more profitable value added product. So, my understanding is no bottle-neck on going with more downstream products for more profitability at current capacity itself

1 Like

Whether the annual EPS is 85 or 95, it really doesn’t matter as of now.

It hardly changes the PE ratio from 3.05 to 3.4.

No stock in Indian market stays at 3-4 PE for a long time (unless it has high debt with corporate gov issues).

Even stocks with corp gov issue and high debt trade at 8-10 PE in Indian markets.

Stocks trade at 3-4 PE only when market is very bearish on their near term earnings (like steel duty), and once that event/earnings impact passes away, the low PE ratio doesn’t remain at 3-4 range for a long time.

4 Likes

Got a very important clarification from today’s concall-

The current price of pellet of 8800 per tonne is without the premium of high grade pellet.

For high grade pellet, the price is around 9900-10000 per tonne today.

The Q1 pellet price was 11500 per tonne.

10K per tonne today’s price is only 13% fall from Q1 price.

The iron ore royalty will also come down substantially due to fall in IBM price (with a lag of 2-3 months).

One can easily calculate the net profit based on this information.

Meanwhile, the prices continue to surge today too-

Based on the surging prices, I am expecting a Buyback with the next results.

3 Likes

Very long term positive for steel industry-

Earlier Indian prices were set at export parity price = International price - Freight cost

Gradually, Indian prices will be set at import parity price = International price + Freight cost

No wonder Indian steel prices are very resilient! This is how free markets work, despite the steel duty.

JSW steel stock price before steel duty = Rs. 630 on 20 May 2022.

Today’s stock price of Rs. 640 is higher than that.

4 Likes

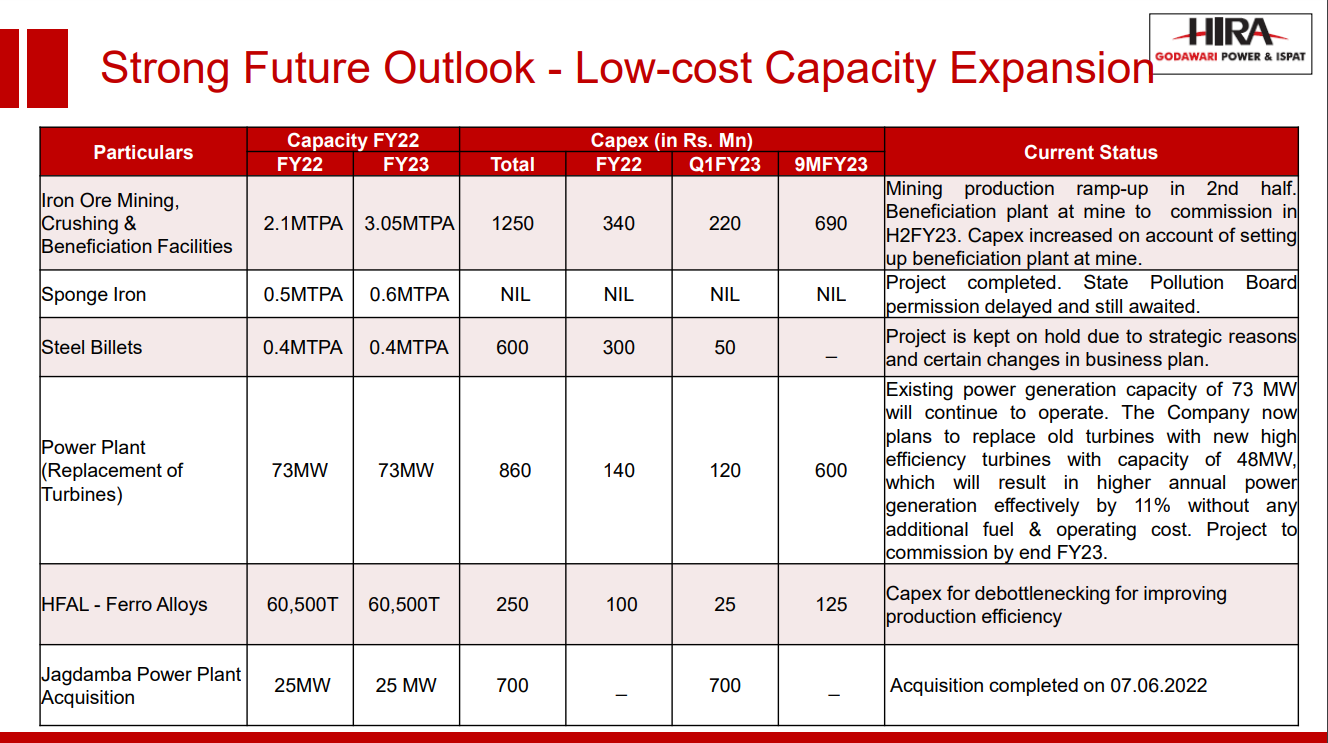

@Kumar_manas, the management team said that the new beneficiation plant near the mines is being set up to eliminate around 20% loss of output during transit from mines to the incumbent plant. So, does that mean the existing plant will be underutilized?

1 Like

Company continues to impress on all fronts. As discussed by some investors above, we will start seeing the impact of export duties and resultant lower realisations from Q2FY23 because of the lag effect. Good to see they are focusing on sponge iron and other products to try and maintain good margins. Kudos to @Kumar_manas for being right about this all along. Seems fair to assume this will cushion the margin hit a lot of people were expecting next quarter to a significant extent as even though prices of pellets have corrected quite a bit, prices of sponge iron and billets are actually trading higher than they were before the export duties.

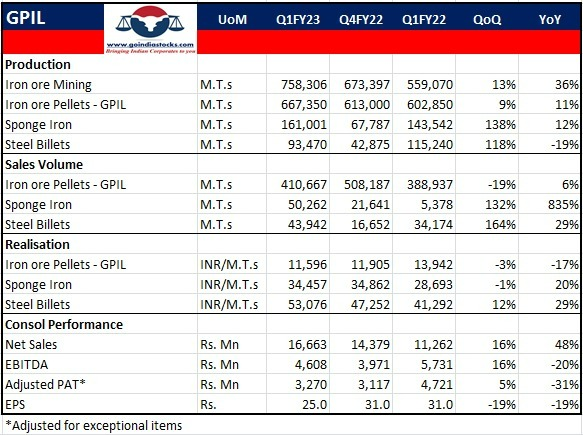

Credits to Go India Stocks for the following image that summaries the performance.

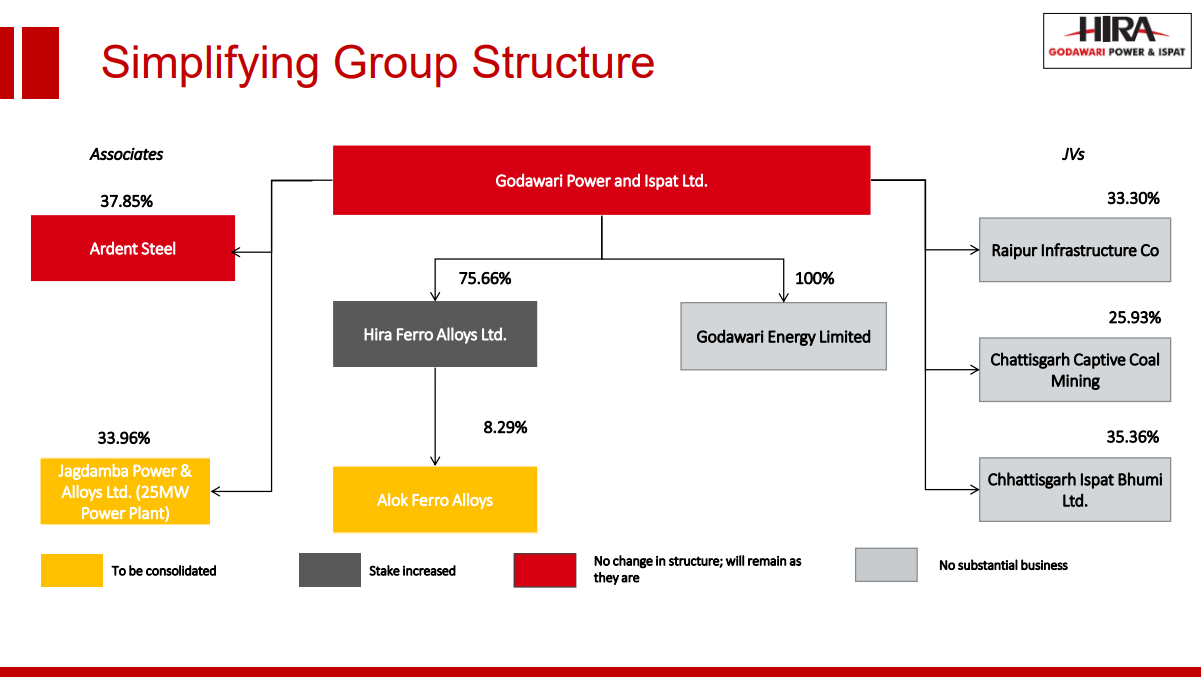

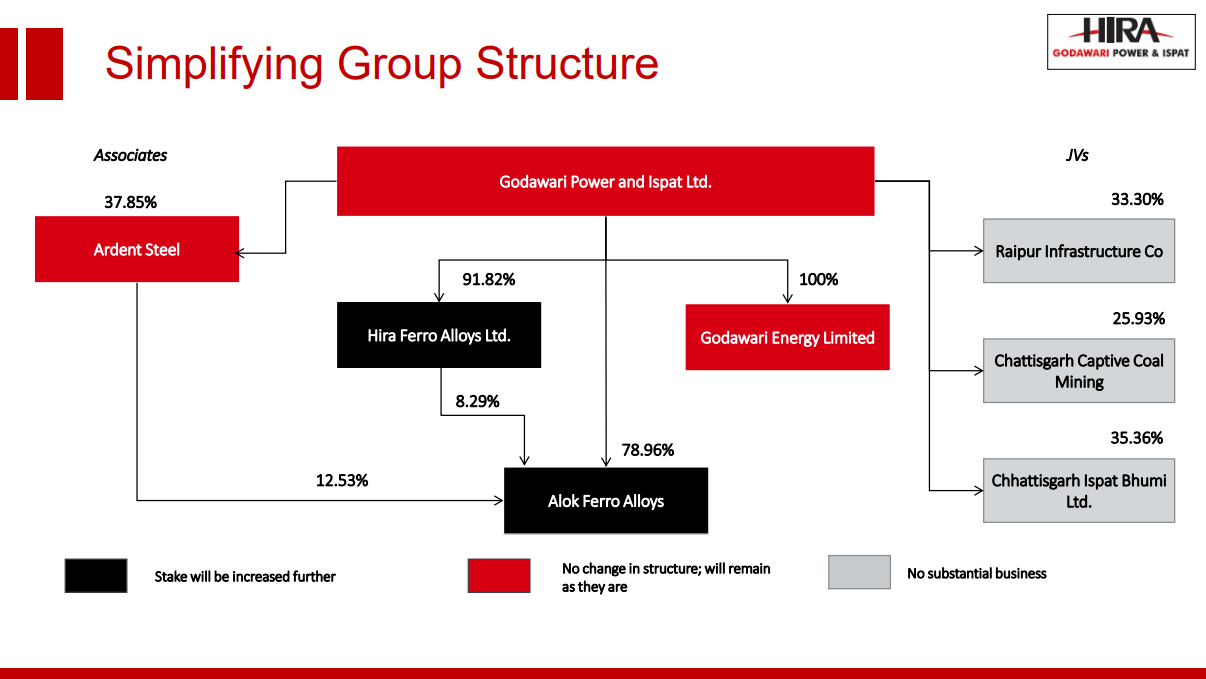

Group structure being simplified:

- Management have guided they will eventually make both HFAL and AFAL wholly owned subsidiaries.

- Acquired the 25MW Jagdamba Power Plant on slump sale basis and surrendered shares in buyback launchd by the company so that they qualify as captive producers.

Q4FY22:

Q1F23:

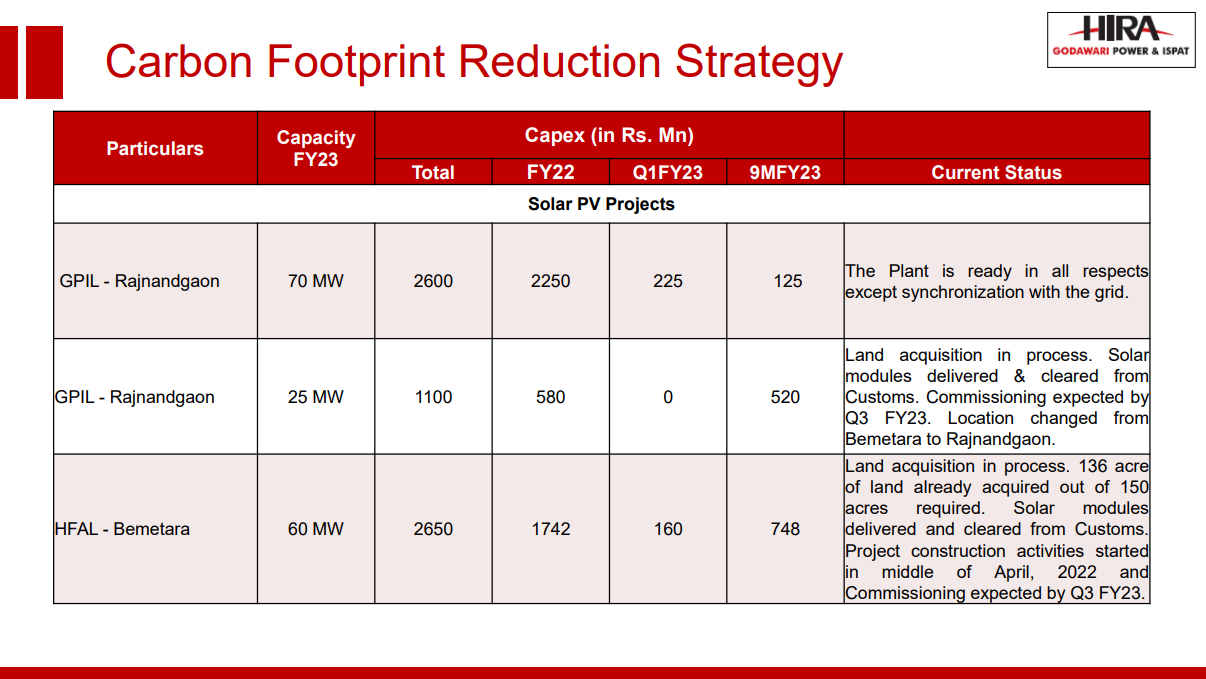

Solar Plants + Carbon Footprint Reduction + Power Cost Savings:

- Confident they will commission all solar plants - total of 155MW - within FY23.

- Once solar plants go live, existing capacities will have achieved carbon neutrality -

155MW solar + 42MW waste heat recovery + 8.5 MW biomass (HFAL) + 1.5MW windmill - Once solar plants go live, prices inclusive of interest and depreciation won’t exceed 2.25 rs/unit. Currently they are paying grid prices which amount to 6rs/unit. And the rates at the mine are 14 rs/unit.

- In an interview with CNBC TV18, Abhishek quantified these savings to around 100 cr on an annual basis.

Capex + Greenfield Project Updates:

- Maintain guidance of 500 cr capex in FY23, of which 150 cr undertaken in 1QFY23.

- Greenfield capex still in planning stages. Finalising of design, size, capacity and technology yet to be done. Processes of environmental approval, land acquisition ongoing. Investments will be announced based on market conditions and cashflow of the company.

- Ore is currently transported from the mine to the complex where it is beneficiated. 20% of the ore becomes waste after this process. So beneficiating at the mine pre transit will save 20% in freight costs. Cost of beneficiation - 150rs/t.

- Beneficiation at the mine will also help them accurately pay royalties under a recent IBM rate which is based on concentrate level.

Coal:

- Had to buy thermal coal for the sponge iron plant which lead to higher expenses this quarter.

- Moved from higher grade RB1 coal to RB3 for cost reasons. Might lead to 2-5% dop in production but will be made up by lower costs.

- Trying to bid for a captive coal mine under auction in order to fulfill the long-term requirements of GPIL, HFAL and AFAL which are now dependent on linkages from Coal India. Have been unsuccessful so far because of the cost structure but should be able to acquire one once the premium is within their range band.

Iron ore costs:

- IBM royalty rates are lagging by 3 months and they are currently paying royalties as per iron ore prices in May. This should reduce by 200-300rs going ahead based on where iron ore prices are now.

- Fuel costs also contributed in the way of diesel prices. Both these factors combined have led to a 450 rs in landed cost of iron ore.

Overall, management has guided that the focus for the next few years will be bottomline as significant topline expansion can only come after the greenfield project is live. Was hoping for them to share some idea of what they have planned for growth ahead but I guess the delay is understandable given the situation post export duties. I find the company to be trading very cheap even on sustainable earnings at current capacity.

Some upside risks I see are significant cost savings (power, freight), increase of share of high-grade pellets in mix, reduction/removal of export duties, China infrastructure + realty stimulus.

Downside risks are significant fall in commodity prices globally due to recession fears, China debt contagion.

Disclosure: Invested

10 Likes

There is another upside which you missed in my view.

That’s inflation and fall in purchasing power of INR.

I mentioned it earlier and in India, everything nearly doubles in price every 7-8 years irrespective of what happens in China or Russia.

Meanwhile average pellet prices have increased today to 9100-9200 per tonne.

High grade pellet is at 10200-10300 per tonne.

https://www.steelmint.com/insights/SteelMint-PELLEX-inches-up-by-INR-200-t-on-increase-in-offers-345501

3 Likes

India is much more tightly integrated with rest of the world than before, so won’t at least a portion of the steel that Chinese mills keep churning out find its way to the rest of the world, esp India ? With China having world’s 50% capacity, the same steel mills who are complaining against export duty today will have no problem asking for a steep import duty.

It is important to take note when Godawari management says:

- Any revenue growth for the next 2-3 years will come from realizations

- Greenfield plant will be purely based on evolving market conditions and future cash flow of the company.

It is funny that article you have linked says that 1/3 of China steel will be bankrupt- this is very good news for Indian steel industry.

Competition going Bankrupt is the best news ever!

1 Like

Yeah, but only over 5 years ! I wish it was immediate.

https://www.nasdaq.com/articles/iron-ore-rally-loses-momentum-as-china-steel-curbs-weigh

While the first order thinking is that with Ukraine/Russian exports out of the market, there should be more demand for others to fill the gap it is interesting to see international iron ore exporters like Vale, Rio Tinto etc also reducing iron ore output.

Looks like India may be the only growth market now and for foreseeable future, but how much the growth and hence steel price stability will be is anybody’s guess.

1 Like

I plan to hold GPIL for 5 yrs, so am happy with 5 yr view. Haven’t bought this for short term trading.

1 Like