@Kumar_manas sir, it is evident that the steel and iron ore demand will increase due to the upcoming Capex cycle. You said that the supply will most probably decrease due to the export duty and margin pressure.

Will this in turn cause Margins to expand of companies like GPIL?

Why dont these brokerages cover GPIL?

It is a decent sized company now, with 1500 cr+ annual EBITDA (Not many companies in India make this much money)

in 6 yrs, GPIL mining capacity will reach 9mnt/annum, which will put it just next to Jindal steel.

It will be a fairly big company in few years.

Yet, no big broker covers them.

Sir, the cancellation of shares is not mandatory hence, contingent upon the management’s discretion because subsidiary companies need not cancel shares of holding company if those were being held even before the company became a subsidiary.

So GPIL shareholders will only see accounting benefits if

a) the management indeed decides to cancel those shares

b) GPIL declares dividends (divided portion of the income will be piggybacked in the consolidated FS)

c) in the remote change of HFAL and AFAl being merged with GPIL

Do you @Kumar_manas think that the shares will be cancelled? One should ask this in the next earnings call.

You are so much worried abt accounting benefits but real cash is what is more important.

5% of Dividend will go in HFAL and AFA which are now 90% held by GPIL- so effectively, this 5% is with the company only.

Actual Share cancellation may happen after 1 year. How does it matter- as long as effectively, the shares are as good as cancelled.

I am worried because if the shares do not get cancelled then GPIL shareholders will be at the mercy of AFAL and HFAL’s ability to allocate capital effectively. 5% of the dividends in cash will go to those two companies and will only come back to us in the form of income generated from reinvestment of that cash which is riskier than if simply those shares were cancelled. Of course, those two companies may end up investing that cash effectively and create more wealth for GPIL shareholders.

I asked the question considering the possible risk of misallocation of dividends by those two companies. Yes, effectively that money belongs to GPIL shareholders.

This is what happens when one doesn’t own the raw materials.

Sales price fell 15% but raw material inventory which has been bought at high market prices is at high cost, plus depreciation and interest cost is super high- so, your EBITDA falls 50% and net profit falls 80%- none of this is applicable for GPIL.

Hi GPIL uses thermal coal for part of its power requirement (part by solar, which within a year will meet 100% of the requirement) and also in its process to make DRI sponge iron. Any thoughts on impact of the current very high coal prices on its cost of operations?

I am still learning about this Industry so, anyone please address my questions.

How are sales generated? What is the industry average (Company specific is fine too) of repeat orders? Do suppliers reach out or the customers? Is there an online aggregator/market place platform?

Result is here.

Pretty decent with 25 EPS.

My guess is 15-18 EPS for Q2 (Q2 is weakest quarter due to Monsoons, though 20 EPS can also come, 50 for H2, Total EPS around 90-95 for the year.

At same prices, with double the capacity in 3 years, the EPS should be 200 in FY 26. (and 400 in FY 29, with 4x the capacity)

(Future EPS can further increase if prices of mid-steel products increase over long term- which is a certainty in a high inflation country with depreciating currency)

I would leave price targets and valuations to the market, something which we don’t have any control on.

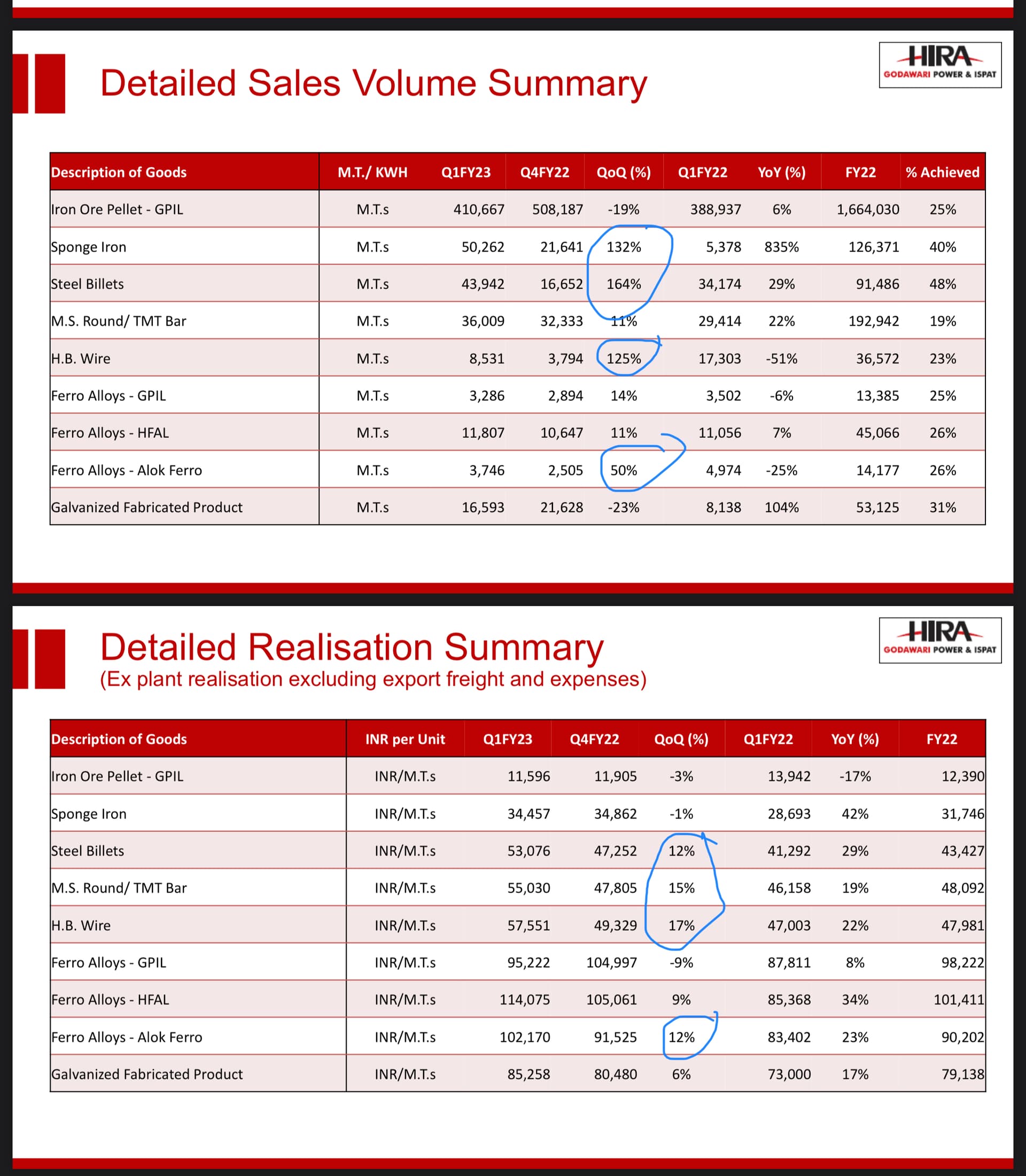

The pellet realization (3% down QoQ) and sales volume (19% down QoQ) both DOWN QoQ.

But, net sales is UP 16% QoQ, and EBITDA is also UP 16% QoQ.

Implies, majority of sales and profits is right now NOT coming from Pellets.

Prices of other products are pretty stable and strong.

No sharp fall in earnings expected unlike other steel companies.

Company should have 1000 crore cash balance by mid-term results.

From the investor presentation, one can make out the quality of management and their thought process of managing the company.

I find management quality and thought process far better than most other companies.

Verdict in favour of GGEL (a former subsidiary of GPIL) wrt to appeal made for compensation for insufficient Direct Normal Irradiance. The majority of the compensation (along with liquidation damages of 14 cr reimbursement) will accrue to GPIL.

@Kumar_manas Trying to under stand about GPIL, from the presentation is it fair to say that GPIL produce iron ore and converts to value added products pellets/billets and other products. It does not sell iron ore directly in the market like NMDC, is it fair understanding or it sells iron ore also.

From the presentation it’s Management is moving in clear path and direction for the future, it become debt free, removed pledge last year, giving dividends, increasing stake in subsidiaries, sold non core assets, setting up solar plants, increasing existing capacities with clear goals for next 3/7 years.

The below shows the profit contribution for the quarter: