Yes that’s a good view, I think GPIL is under-priced even absolutely, leave alone any comparison with Sarda/Shyam Metalics, though both have their own advantages too in some fashion.

I’m absolutely surprised how Shyam was able to complete major expansion recently (from IPO proceeds without major debt) and looking to raise Rs.5000 cr for even further expansion right from pellets to steel mill, without captive iron ore.

They were probably lucky to not be saddled with debt payments like GPIL and rode the wave last 2 years making surplus money.

My only thinking is if GPIL may be too conservative to have more capacity in time for the next growth wave after this phase of maturity/stability.

Biggest trigger which no one is paying attention is 4x increase in mining reserves.

That’s huge as their biggest asset is their mine.

And, it is totally asset light.

Imagine a real estate company- whose land bank increases 4x overnight at no extra cost.

You cannot sell the Iron Ore in open market and present capacities are fully utilised. You need to incur CAPEX to fully utilise these Iron Ore mines. For utilising additional 1 MT Iron ore you need CAPEX for 1 MTPA.

@Kumar_manas In your real estate example you can sell the land however here you cannot sell the Iron ore …

Flip side of Chinese Steel companies going bankrupt will be surplus supply of Iron Ore which will further bring down the prices to Iron ore and negatively impact Godawari. Also slow down in China will force Chinese steel companies to glut the global steel market thereby impacting all steel producers including Indians.

Stock price is a function of future earnings, not of today’s earnings.

The future earnings of GPIL went up 4x (7-8 yrs from now) because of 4x increase in mining reserves.

Even, real estate developers don’t sell vacant land, they also develop land and sell projects- and it takes many years for them to develop projects on vacant land.

And, btw, captive miners can sell iron ore in open market if they want to. But they don’t sell because selling value added products gives much higher margin. That restriction to not sell has been removed.

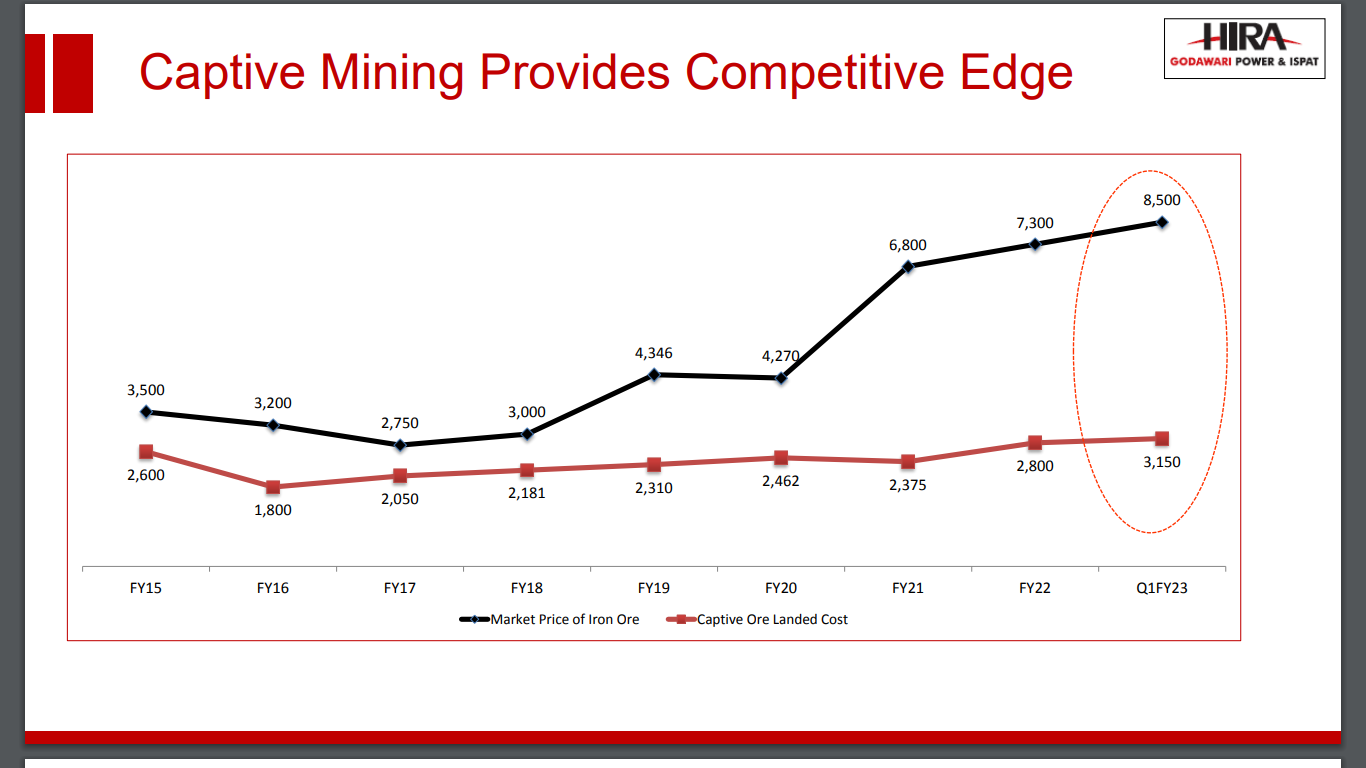

GPIL makes Rs. 3000 per tonne of iron ore (market price of iron ore lumps = Rs. 6000, captive iron ore = Rs. 3000 per tonne)

Total mine reserve = 160 million tonne.

Value of mine = 160 million tonne X Rs. 3000 = Rs. 480 Billions = 6 billion USD

If market price of iron ore goes to Rs. 10000 per tonne, 5 years from now,

The value of iron ore mine = 15 billion USD

This valuation excludes the pellet/billet/wire rod plant and solar power plants.

This I had mentioned earlier too. Export duty has increased domestic price vs International price.

Before export duty,

Domestic price = export parity price = International price - freight cost

After export duty.

Domestic price = import parity price = International price + freight cost

Also, note JSW steel stock price just before export duty = Rs. 630

Today, JSW stock price = Rs. 652

Not sure, how export duty is negative for steel industry. Even stock prices don’t agree with opinion of the analysts.

@Kumar_manas

Hi sir thankyou for sharing your views on this stock regularly. I have investments here from lower levels and your research really adds lot of conviction of mine into this stock. Thankyou once again.

Kindly note tha t the prices of Iron Ore w.e.f. 11-08-2022 has been fixed as under:

i) Lump Ore (65.53, 6-40mm)@ Rs. 4, 100/- per ton

ii) Fines ( 643, -1 Omm) @ Rs. 2, 910/- per ton

The irone ore price set by NMDC is below market price as of now. Does this affect GPIL in any way or the overall price of irone ore. Please share your thoughts.

Aurangabad. Large scale black money has been recovered in Income Tax raids at two places in Aurangabad and Jalna of Maharashtra. Income tax teams raided a builder in Aurangabad and the owner of a steel making company in Jalna. Black money of 390 crores has been unearthed in the raids. Income tax officers recovered Rs 58 crore cash and 32 kg gold from both the places. It took the officers close to 13 hours to count the cash. The raids were conducted in Jalna on 3 August. The owners of SRJ PT Steels Pvt Ltd and Kalika Steel Alloys Pvt Ltd came under the scanner of these raids. Teams of 260 Income Tax officers conducted raids in Jalna.

KSAPL, incorporated in October 2002, is engaged in the production of TMT bars with an

installed capacity of 2, 50,000 metric tonnes per annum (MTPA). It is backward integrated with

an installed capacity to manufacture 2,50,000 MTPA of billets.

Its unrelated news to GPIL post, but this raid will strengthen the perception of the government about the windfall profit that has been made by steel companies during last 2 to 3 years.

I see your posts in Yes Bank thread, you know and post a lot. You are like a lone warrior in Yes Bank, opposite to IDFC First Bank thread, where there are many.

But here you are saying that his research is adding conviction to yours, what you think about the business is what matters. I don’t think you follow Godawari Power as much as Yes Bank.

There are some threads where only one or two members post, only those one or two members are invested and follow the business, because they have their own view, thesis and conviction. It does not matter to them if anyone else is invested or not. What they think about the business matters to them. Sometimes they win, sometimes they may lose, but it is their conviction that drives them forward.

Sometimes some members read the whole thread and come to a decision, I do that too when a business is new to me. But a member having great conviction should not have any effect on our conviction, because their investment is not like their home which they will not sell, they can sell their holding without any notice to us for any reason. They may even disappear from the forum. I had this experience.

A lot is posted in this thread, as you are a full time investor, you can very well read the whole thread, and as you become more knowledgeable, you can even differ with the regular members of the thread, find fault in their thesis.

As you are young, I felt like saying this, don’t take it the wrong way, I only wish you good.

Performance: Operating performance

-Highest annual iron ore mining in FY22 of 2.3 MillionT (YoY increase of 36 Per cent) (previous best in FY21 of 1.6MnT)

-Record annual iron ore pellets production of 2399 KT (up 6 Per cent YoY) (previous best in FY21 of

2256 KT)

-Highest annual ferro-alloy production in FY22 of 16KT (up 14 Per cent YoY) (previous best in FY21 of 14KT) Financial performance

(standalone)

-Record turnover of Rs. 50,746 Million, up 39 Per cent YoY

-Highest EBITDA of Rs. 17,993 Million, up 78 Per cent YoY

-Record PAT of Rs. 13,510 Million, up 116 Per cent YoY Balance Sheet performance

Your Company became long-term net debt-free on a standalone basis in Q1FY22 and net debt-free on a consolidated basis in Q4 FY22.

@Kumar_manas : Sorry I have not done that calculation but would certainly like to have insight from you.

However, CFR Iron ore prices in China was trading below $100 in China 2 days back when compared to peak of $225 last year during same time. With the possible recessionary trend in Europe and lower growth rate in China the demand for Iron ore over its supply is thing to be monitored.

What impact would it have if Iron ore prices go around USD 75.