Which means in a quarter when the current supply has been absorbed, we are looking at reduced supply against decent domestic demand i.e. domestic pellet prices will go back up to an extent, unless the govt rolls back the export duty?

1 Like

@kumar_manas sir, do you expect Q1’s results to improve is the EC is approved?

EC will come in a few mths.

However, Q1 should be better or same as Q4 because that limit is not a constraint in Q1.

By Q4, EC shd come.

20% increase in sponge iron capacity should lead to 5-8% improvement in net profit I guess.

Plus add 100 cr or so additional EBITDA once all the solar power plants become operational.

plus add additional margins from 100% high grade pellets.

This year profits should not be very different from last year despite the export duty is my guess.

They can be 10-20% lower though.

6 Likes

The government will be happy with its decision as steel prices have drastically come down. Further every body knows that steel Companies including pellet units have made windfall profits during last 2 years and hence government would not mind even if there profit is reduced for next 1 year. This Companies have made sufficent profits and deleveraged their balance sheet to face any such adverse impact. Government present focus is on inflation and they would mind steel companies making low profits or even loss provided steel prices are in control.

Pellet units were working in cartel and were keeping the domestic prices high as there was good export opportunity but now the tide have turned agaisnt them.

1 Like

Very few companies own captive iron ore mines.

Infact, many small scale steel mills have done very poorly because they had to buy pellet/ore at high prices.

You can google articles in 2020/21- which mention the same.

Infact, one of my banker friend told lot of small scale steel plants in Raipur had closed down.

GPIL made big profits because it had the mines- and it will still continue to make very good profits- bcz it also earns money from ferro-alloys (no export duty), new solar power plants, billets (no export duty), sponge iron (no export duty).

Out of 1400-1500 cr quarterly revenue, only 500-600 cr revenue is from pellets.

Companies that did not own the mines like KIOCL did not make any windfall profits, and have already closed down their pellet plants.

The closure of many pellet plants will result in unemployment, reduction in state and central govt revenue, no capex in this sector, and low GDP as well.

Less forex earnings too. Eventually, shortage of pellets in the country!

How does this help the govt??

10-15% fall in steel price- is it more important than so many negative factors?

Infact, profits of GPIL will increase exponentially over the decade.

6 yrs from now, GPIL will be mining 7 mn tonnes of iron ore per year ( from 2.1 mn tonnes today), plus price of pellets/sponge-iron/billets should be at least 50% higher.

Cost remains the same.

Please calculate the profits if you can!

8 Likes

Management is eyeing to expand its mining capacity to over 9MTPA over the long term right? Expanded capacity X median margins (assumption) would mean an inevitable rise in EPS by 2030. Is it reasonable? @Kumar_manas

Why would you take median margins as an assumption? This is not JSW steel, where margin = market price of steel - market price of raw materials.

In GPIL, margins = market price of steel intermediates - fixed low price of own iron ore

So, the cost will not increase over coming years.

But, the market price will keep increasing - due to inflation, falling INR, and increasing steel prices over the years.

So, the margins will keep increasing forever (with some volatility in between, when steel prices cool off for a few months, but if you look over years, they will keep increasing)

3 Likes

The point I was trying to get across was that even with conservative assumption, given the current price, the investment makes sense. It doesn’t matter what the reasonable/most probable outcome would be. The expanding capacity itself protects the downside over the long run. That is what my reply supposed to mean to the question you had posed.

Disclosure: I have a position in GPIL.

1 Like

No, it doesn’t protect the downside. Currently, the EV is around 3000 cr, and EBITDA is 1200 cr. (after the import duty and fall in prices, otherwise the EBITDA is 1800-1900 cr)

It can go to 2x EV/EBITDA or even 1x EV/EBITDA! means, it can fall 60% from here too.

5 Likes

Can anyone calculate FY 23 estimated EBITDA based on current sponge iron, billet, wire rod, pellet prices + taking in account 20% higher sponge iron capacity, high grade pellet, ferro alloys business, and new solar plants.

It would be an interesting and easy exercise in excel sheet.

1 Like

Sir, if you do these calculations, may you please upload the excel sheet here as well so we can learn?

1 Like

I never said it would in the short term (it dropped 20% the other day - gyrations in the prices don’t concern me as long as the business fundamentals are good), I was alluding to the 9MTPA expansion plan which will take, god knows how long and this hike in duty is to curb the inflation and the management also believes it is a short term measure. Yeah, it can drop 60% and you may consider it as a risk but I don’t because I have no plan of selling GPIL.

GPIL still has not received EC for sponge iron capacity expansion right? When do you reckon they will get it? Will the coal prices fall any time soon and if it does what do you think the sustainable premium for HG pellets will be?

Hi @Kumar_manas,

Based on today’s prices with some assumptions and 50% effect of additional EBITDA from solar power (150/2 = 75 cr). According to recent steelmint article, Godawari’s pellet quoted price was Rs.8800 I think.

Steel.xlsx (42.0 KB)

4 Likes

Nice job, however, do note that April and May were almost over by the time the duty was announced.

My broad guess is 1600 cr annual EBITDA.

If you add additional interest income from surplus cash balance, the net profit will be more or less similar (10% lower) to FY 22. So, the EPS may be Rs. 100 for FY 23 as well, and it continues to trade at a measly PE of 2.6 with 1000 cr cash balance as of date. Likely dividend of Rs. 15 in FY 23 translating to a yield of nearly 6.5%. If dividend is higher at 20% of profits, it will be 8% dividend yield itself.

When will PE come in 12-15 range so that it becomes a consensus buy is what I wonder! (cyclicals should be bought at high PE is the consensus I guess)

Also, note that depreciation in GPIL P&L is very low compared to other steel cos, as it is an asset light business.

6 Likes

Right ! but I was thinking it may kind of average out over the subsequent 10 months in FY23.

Material cost for FY22 is ~2455 crores, calculating landed cost of iron ore for each q and the quantity mined - from the PPT, iron ore cost is “just” ~675 crores, just ~27% of total raw material cost.

But we never know how the business case for lower value-add products will change. I really wish Godawari would move to higher value products with duty-free export potential.

I hope that happens too, but likely only if earnings deteriorate drastically.

The trick is to find a high debt, high or negative PE company at the bottom of the cycle and ride out the deleverage story with the cycle for outsized gains - Godawari ticked all the boxes. I’m trying to figure out if this is good for the next cycle too.

Additional capex may get some depreciation, but with the company not going ahead with the steel plant depreciation will be very little. As it stands today, management seems to be ultra cautious with any high capex or trying anything outside of what has worked for them last few years - stung by the BIFR experience I guess.

6 Likes

The last 11 years data shows that operating profit of GPIL has never gone down drastically.

Last few yrs growth is without the increase in mining capacity.

Coming 5 yrs, mining capacity is going 4x.

I wonder the growth ahead, plus add the inflation and falling INR leading to higher steel prices over the years.

2 Likes

There’s 89% correlation between market/landed price of iron ore ratio with EBITDA% for that quarter.

I’d be happy if they can do the 2nd stage expansion to 5Mill Ton over next 2-3 years (by FY26 ?).

Can we somehow figure out what a sustainable minimum EBITDA could be from now on. It will be highly determined by the market price of iron ore (a floor has been set from recent 2020 auctions).

Is it a coincidence that the ratio peak 3.83 was when Godawari stock price also hit a high, discounting the recent high which I think was because of the Russia-Ukraine war disruption

2 Likes

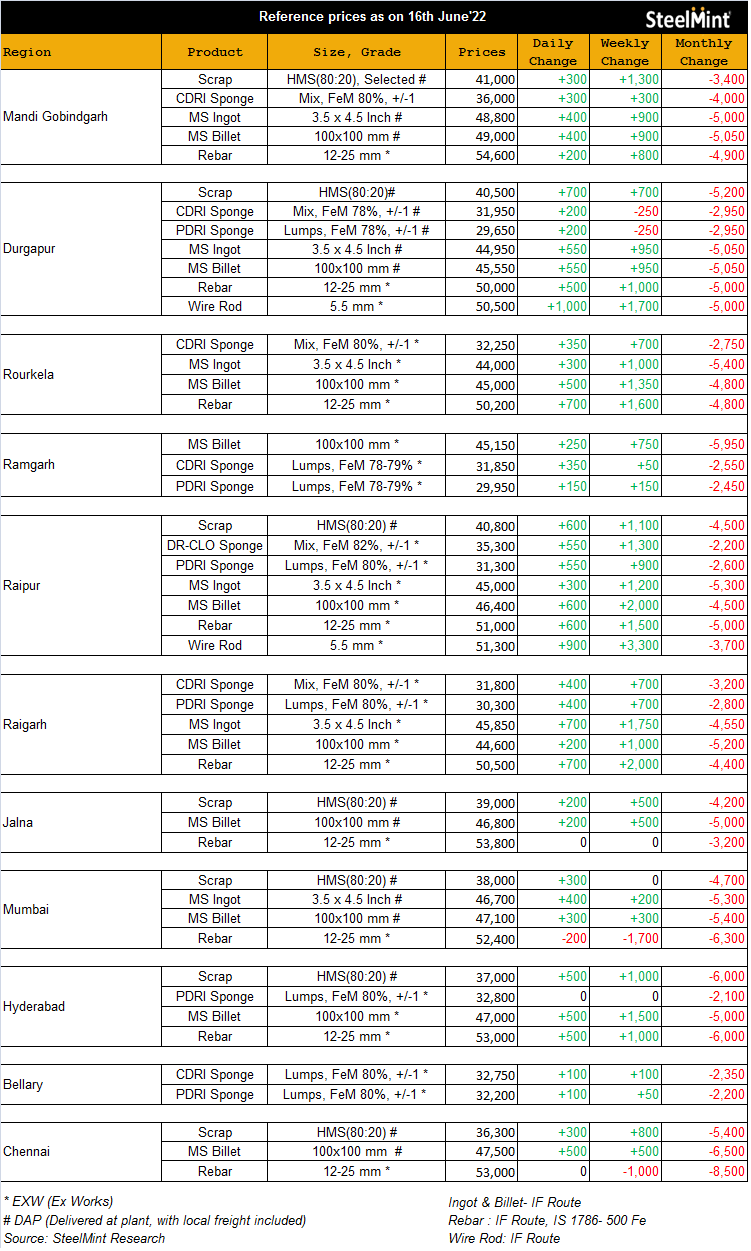

The whole thesis of bearishness is reduction in steel prices due to export duty.

BUT, these are today’s prices.

Do note the weekly and monthly change. It isn’t that bad!

If one can control inflation by putting export duties, then inflation would not have been high during Nehru (pre-1990 times), or USA can easily put export duty on their petroleum exports and bring down inflation.

This will backfire big time.

The whole cyclicality theory is based on dumping of steel by China in 2015-16 which was once in 20-30 years event. It happened due to excess chinese capacity created due to stimulus in 2008-09 financial crash. This isn’t happening again I guess!

It will take sometime for markets to realise the same.

5 Likes

@Kumar_manas Prices are just one variable - do we have a way of monitoring volumes? No point to pointing to prices if there are very few trades happening.

Going forward this will be something to monitor:

If they somehow actually manage to execute this, that may put a cap on iron ore prices.

Another interesting thing happening in China is this:

If coking coal falls off more and the same happens in India, that would negate our higher-grade premium thesis.

Personally I feel it’s clear to see we are watching the downcycle play out in metals globally with interest rate hike environment, talks of recession and dollar index at 104. China opening optimism also faded out with further cases showing up and also doubts on the rebound of the realty sector and economy at large.

Disc: Only partially invested and being very cautious here

3 Likes