Results are out and would not like to dwell much on them. The clarity of the management, on the impact of goverments recently announced policy ,will be keenly watched by investors in the conference call , scheduled on 30 May . This call will be more important than the just declared results.

2 Likes

GPIL seems peeked fundamentally for a temporary phase. may see a significant drawdown in stock price. as commodity stocks teacher says sell when you get the best of the best profit and margin results. this may be a temporary correction. metal super-cycle story is intact as long as china is importing metals or not exporting. keep an eye on china and ride on metals. corrections are friend.

2 Likes

This is last 12 years of revenue and EBITDA for GPIL.

There is small blip in 2016 due to ultra-low iron ore prices (big crash actually of metal prices, when broader markets also fell).

Other than 2016, I don’t find big cyclicality in this business.

Please correct me if I am wrong.

Also, both revenue and profit growth over 12 years is more stable and much higher than most non-cyclical companies.

Also, note that USD iron ore prices in 2010-2011 were 20-30% higher from today’s iron ore prices, yet today’s EBITDA is 9x higher, primarily due to capacity expansion.

9 Likes

The industry is trying to reverse the tax also. This tax would kill a vital part of value added steel product export. This is not very good for indian economy. Hopefully they will succeed in getting these taxes down to a reasonable level if not reversing it completely.

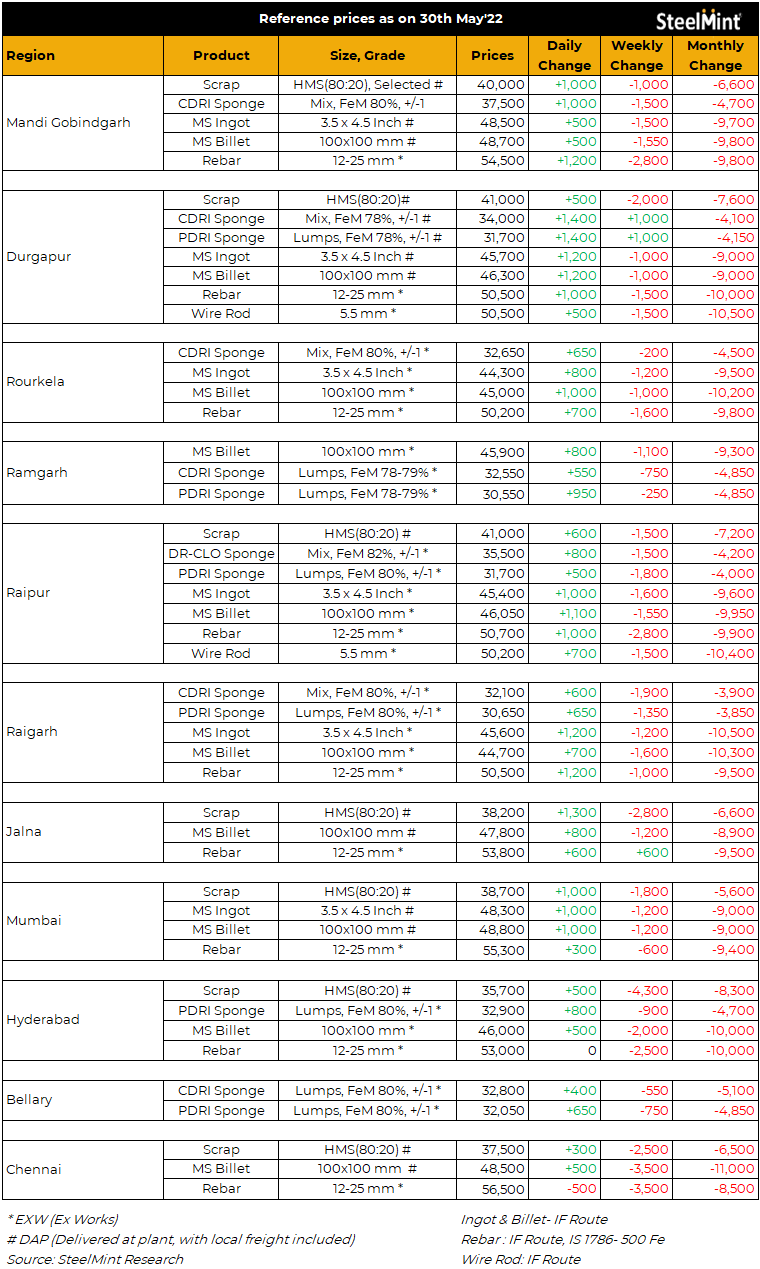

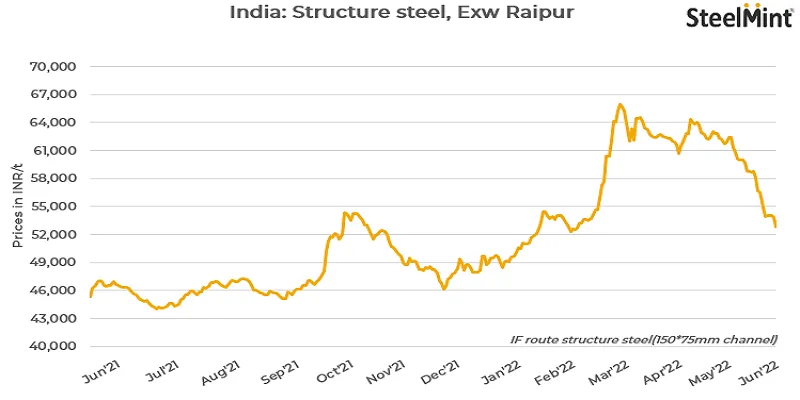

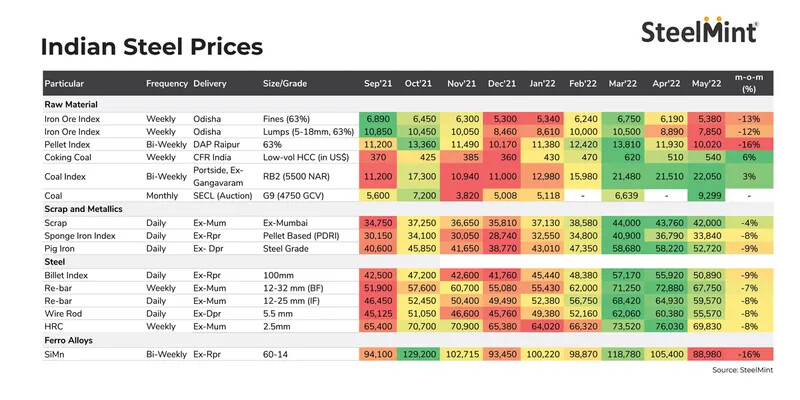

Structural steel prices in Raipur. Latest prices.

This looks like a steep drop- but please note- today’s prices are the peak of 2021 prices. This is after import duty!

7 Likes

Wanted to wait for the concall to post here because management commentary was crucial for so many of us given the circumstances post the imposition of export duties.

General thoughts on the results:

GPIL results were below expectations due to poor showing in sponge iron and billets. However, the numbers are commendable nonetheless and PAT is higher than Q3 on account of gain of 98 cr on sale of GGEL. Full year EBITDA well above management guidance of 1600 cr.

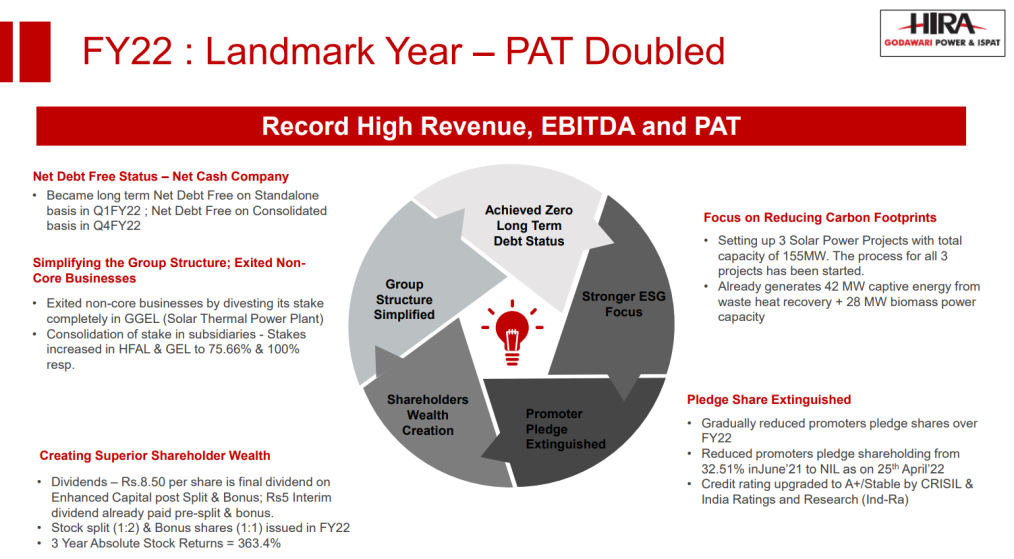

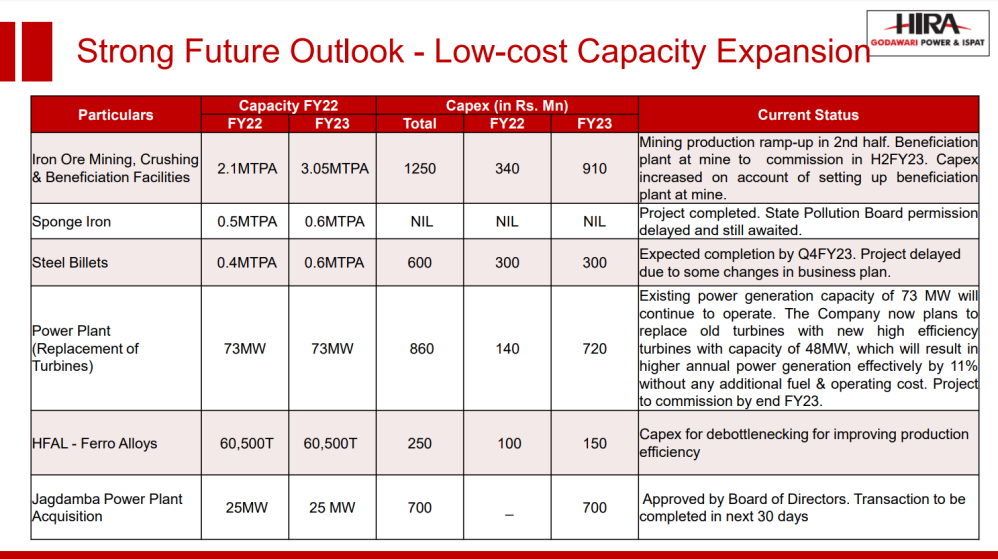

I think it’s a good time to reflect on the year that has been, attaching some slides from the investor presentation that made me smile.

Some takeaways from the concall:

- The poor showing in sponge iron and billets were a result of them reaching their EC limit on sponge iron production resulting in less waste heat power generation which in turn lead to less production of billets. Since the plant was shut anyway, they used the opportunity to undertake a maintenance of the plant. It is up and back to functioning as normal.

- Exports were slowing since Q3 anyway, but Abhishek once again mentioned that they have found domestic buyers in the bigger mills like Tata and JSPL. These deals are at par with export prices.

- Q1FY23 will not see much of an impact of the export duties. There was only one shipment which was scheduled for end of June, but they are trying to amicably work out a solution with the buyers.

- Q1FY23 will also see, at maximum, only around a 10% QoQ jump in coal prices as a result of them being well hedged at lower levels till August.

- They can choose to move to 100% high-grade pellets if they want once they ramp up mining production, probably by the end of the financial year. They will then be able to produce these high-grade pellets at no additional extra cost. They are the only producers of high-grade pellets in India and their product sells at a 2500rs/t premium to regular pellets.

- The USP of high-grade pellets is that they require lesser coking coal in the blast furnace and also generate less slag. This leads to cost savings for steel mills, especially with where coal prices are trading at right now. Indian mills are currently saving around 4000rs/t on coking coal by the use of these pellets and hence are happy to pay some of that as premium.

- A new learning for me personally was the direct correlation between coking coal prices and those of high-grade pellets. Because of the reasons mentioned above, they move in tandem - so when coking coal falls, so does the premium of high-grade pellets.

- Announced acquisition of 25MW power plant for 70 cr on slump sale basis from Jagdamba Power and Alloys Limited (JPAL). This will result in 2.5rs/unit cost savings vs grid prices.

- Total capex for FY23 to be around 500 cr, all funded through internal accruals.

Now, some of my thoughts on the environment at large:

- China reopening + infra spending reaction is playing out as expected. Today China’s most-traded Dalian iron ore futures surged 5%, to the highest level since mid-April. Lack of Indian supply also led to some rise in prices.

- Iron ore was trading near 129$ around the time of imposition of duties, now it’s near 137$. China remains a key monitorable as we all know they make up for around 50% of iron ore demand globally. For all you know, they may once again announce measures to clamp down on iron ore speculators sending prices back down again but this will remain a perpetual risk.

- Indian prices will see support because of the scenario post auction regime. Maybe the fall in prices will be cushioned somewhat by rising prices globally as well. General consensus is that buyers are waiting for prices to stabilize before placing orders. We should know in a few weeks.

- My only fear is that monsoons are coming up, which is when infrastructure work slows down and now with the export duties, steel players may cut production if there isn’t enough domestic demand to suck in all this excess supply and export prices aren’t feasible.

And lastly, @Kumar_manas I am an ardent reader of your comments on this thread. I very much agree with your take on the non-cyclicality of revenues of GPIL. Though one must not ignore the following also:

There may not be a cyclicality in the revenues of the business but as a shareholder, there exists a very real reality of having to sit through far larger drawdowns than businesses in other non-cyclical sectors. Even though the business has steadily grown, the market has always treated it and will probably continue to treat it like a cyclical. Our hope is that the updates over the recent past will merit a re-rating or decent multiples but the market may not oblige. So one has to be mindful of entry and exit as well both to make alpha, and for peace of mind. Anybody who bought at 500 levels just 2 months ago on record-breaking results is now sitting at a 40% loss - obviously the export duties ‘black swan’ didn’t help here but the stock had started its downtrend well before. And you never know where you are in the cycle, especially since it’s been 2 years since the Covid lows and iron ore has gone through multiple cycles since, going from above 200$ to below 100$.

So as much as I love this business, I do have a buy-low-sell-high approach as opposed to the long-term investment approach. I took on this approach after I failed to sell in Oct '21 and learnt the hard way that these stocks mostly don’t care about what results the companies are posting and simply track spot prices. I don’t like having to sit through a 20-40% drawdown every quarter, which has been the case for the past few quarters.

Of course I am in no way suggesting others to do the same - it can be cumbersome tracking iron ore prices, news out of China and every update out of the commodities space but it’s what works for me. This is also in no way a criticism of long-term investing, the major chunk of my investments belong to that category.

Also, owning GPIL is not a 20 year call option but at the very least a 35 year one. ![]()

Disc: Now that I’ve explained my trading ideology with this stock, I’d like to mention that I have started accumulating it again in tranches as I feel the correction along with management commentary has made me confident of a margin of safety. This is not a buy or sell recommendation - I change my view frequently and try to be unemotional about hitting the sell button, both on the way up and down.

28 Likes

No, this was because it had high debt earlier. So, there was operating deleverage earlier- that is a 20% reduction in EBITDA led to 40% fall in profits because of high interest cost.

But going forward, 20% fall in EBITDA will lead to only 15% fall in profits- because there will be positive other income instead of interest cost.

This is what happened with Shree cements too.

Shree cements trades at higher PE than rest of cement players- because it has higher margins because of own limestone mine- similar to GPIL owning iron ore mine.

Eventually, GPIL would follow a similar path in terms of markets drawdown too.

Also, institutional shareholding will gradually increase, free float will reduce.

All this takes time, but it happens!

Also, I have made another important observation here. GPIL pellet sales was only around 600 crores (5 lakh tonne *11.9k selling price) in Q4 out of 1300 cr total sales. A lot of sales is from steel intermediates too like sponge iron, TMT bars etc. It is wrong to assume that GPILs profitability depends on primarily pellet prices.

for example- Q4 pellet prices and sales volume- both were substantially higher than Q3- yet total sales was lower by 100 cr vs Q3 (profit was also lower) because of less sponge iron and billet sales. So- the reverse can also happen. Company can give better results even when pellet prices are down!

21 Likes

Why am I increasing my position in GPIL?

Positive factors-

-

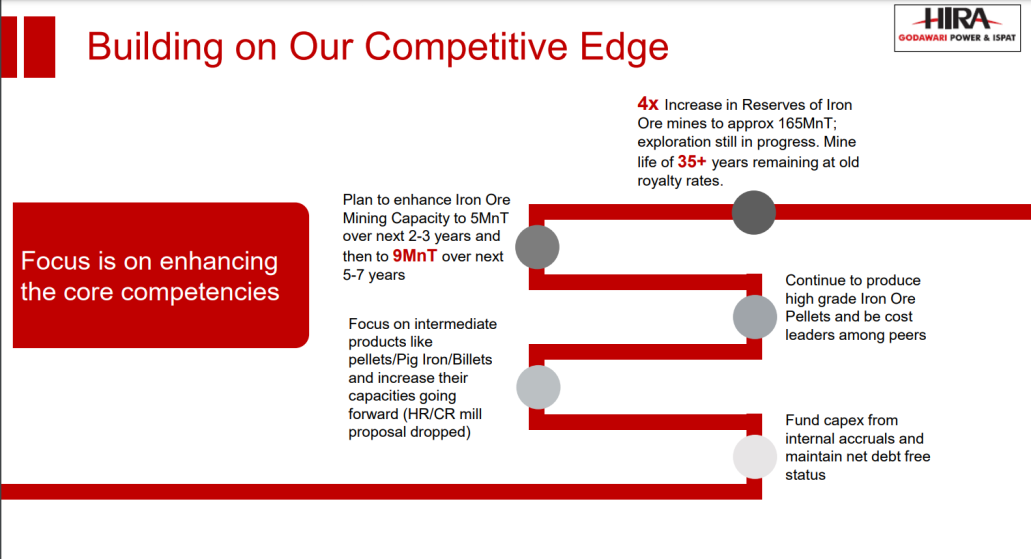

Most important- Increase in mining reserves and doubling of mining capacity to 5mn ton Per annum in 3 yrs, and 4x increase in capacity to 9 mn ton per annum in 6-7 yrs- this is huge.

This is totally new information which was not there a couple of months ago.

Imagine, if NMDC says their capacity will increase 4x in 6 yrs! -

Many new solar plants ad new turbines etc- will directly add to bottomline

-

zero interest cost- and positive other income of interest from cash balance

-

may go for higher dividend/buyback in coming yrs

-

increasing cash reserves- reducing EV

-

Valuations- lower than most PSUs

-

Higher grade pellets- going from 65% to 100% of sales in next 12 months- there is Rs. 2000 per tonne premium here- which directly adds to bottom line.

- EC approval for sponge iron capacity increase can come any day.

- Further increase in billet, bars etc capacity will be done soon. Semi-finished steel is more or less free of export duty. No export duty on billets.

Negative factor-

- Reduction in pellet prices due to export duty- export duty can’t be permanent- already Goa CM has met and even written letters to FM to make export duty on lower grade iron ore to nil.

Soon, odisha and Karnataka CM will join Goa CM.

Such high duties will lead to average quality iron ore accumulating at mines and railway stations- leading to closure of mines, unemployment, reduction in state revenues, and also reduction in production of higher grade iron ore due to poor logistics. also closure of many pellet plants in the country.

So, I guess export duty will be removed in a few months.

Even if it is not removed, it really doesn’t matter that much- pellet revenue in Q4 was 600 cr out of total revenue of 1300 cr. Q4 was abnormal quarter because EC limit of sponge iron was exhausted (as they didn’t get EC approval in time)

In Q3, pellet revenue was 500 cr out of total revenue of 1400 cr.- which is more or less a normal quarter. Once they get EC approval for sponge iron capacity increase, total revenue will increase and percentage share of pellet of total revenue will thus decrease.

Please correct if I am wrong.

A well run pvt company deserves much higher valuation than corrupt and inefficient PSUs in my view.

16 Likes

Only point i would like to put here is " would the growth will be the same? will the price or iron ore will increase from here on? will the new capacities wont took cash off the balance sheet? will they be able to do all expansion on time? will the bottomline will keep on increasing? " If not then do not put new money here because these were the past events on which the stock has already been played out.

If high growth company falters for even one quarters then market punish it severely.

Disc: not invested

1 Like

This is mining capacity. Not sure you have seen a mine or not, but mining iron ore isn’t capital intensive.

Will they do expansion on time- may be before time, or may be a somewhat delayed. This is difference between PSUs and pvt cos. PSUs are pretty inefficient and delay in actually following the plan while pvt cos are fast and efficient.

This stock trades at 3 PE. What punishment can you give to this stock literally?

1 Like

Stagnation in price and IMHO no point in buying cyclicals at PE ratio at least right now.

Yes you are right, i have not seen any mine but why Capital work in progress is 643 crore?

1 Like

Iron ore is now at 145 USD. Indian prices should start moving up sooner or later.

semi-steel and some finished steel don’t have export duty. As deals start happening in those kind of steels, the prices can move up by a good margin.

Also, rupee has fallen 6-7% in last 6 mths. so 145 USD price of today is equivalent to 155 USD price a few mths ago.

7 Likes

This is a very significant event-

A big pellet plant with economies of scale has shut down because it is no longer viable.

Think about the hundreds of small scale pellet plants.

This will lead to- shortage of pellets eventually, no new capex in pellets, unemployment, loss of revenue to state and central govt.

Govt thought that interfering with free markets and imposing export duty will reduce inflation.

But, it doesn’t work like that in free markets.

If prices and profitability comes down, the supply will also come down drastically, as most of pellet companies will close down their plants (as they don’t have mines and high grade pellets like GPIL)

12 Likes

Looks like KIOCL with zero backward integration and worse sourcing iron ore from Jharkhand to Karnataka and no benefaction plant was a sitting duck to get affected, with >95% of its production exported.

https://www.icra.in/Media/OpenMedia?Key=cb02a913-426c-4851-894c-2e2a33aeecc7

With pellet exports around 15% of the domestic production, the other 85% (incl GPIL) may just face profit decrease, we’ll have to see if domestic pellet prices track international prices.

4 Likes

The Domestic hot rolled coil prices corrected further by 3.5% last week to Rs 63,800/tonne. The total correction in domestic HRC prices is now about 13.4%, down from Rs 73,700/tonne a fortnight ago. Prices for coking coal and iron ore have also followed the correction in steel prices. NMDC Ltd. announced a correction of Rs 1,100-1,320/tonne over the weekend in response to dull demand. This was in addition to the Rs 720-750/tonne reduction announced last week. The total correction in iron ore fines is Rs 1,850/tonne. Coking coal prices have also corrected due to the dull demand from Indian mills and improving supply situation. premium high carbon chrome have corrected 17.5% over the last fortnight to $448/tonne.

Latest: Motilal Oswal Report

Motilal_Oswal_Metal_Sector_Update.pdf (1.1 MB)

1 Like

Export ban works in agriculture because govt also has MSP and provides subsidized electricity etc, and also waives off bank loans to farmers.

So, farmers will keep producing more and more wheat irrespective of export ban because they make guaranteed money.

It will backfire big time in steel industry- where pellet plants have already started shutting down.

One should read what happened almost a decade back when govt put only 5% export duty on pellets.

With just 5% export duty, lot of pellet plants shut down and govt had to waive back the duty.

4 Likes

It seems government getting what it wanted . How much of the iron ore was used in the pellet industry for export purposes ![]()

Was it really this much to off set rates to this extent ![]()

Thanks @Kumar_manas, you’ve explained the 5% export duty imposed in early 2014 and removed early 2016 Godawari Power - Any Trackers? - #307 by Kumar_manas.

Apparently there has been a clamor for such duty from small secondary steel mills for nearly an year Secondary Steel Msmes: High iron-ore, pellet prices forcing small secondary steel units to close shops, ET Auto.

Looks like govt didn’t do its homework on second order effects of high iron ore prices from recent auctions. High iron ore prices may have removed a lot of margin elasticity available from the miner to downstream processors.

I can’t understand how a govt entity like KIOCL was allowed to survive with its overheads - the company has a business case only in extreme times with high pellet prices.

45% export duty will lead to closure of most pellet plants I guess.

Logistic cost+buying iron ore at mkt price+high labor cost = better to shut down theplant.

Right now, we have excess supply of pellets in the market because of sudden announcement.

Once this supply is absorbed in a month by the domestic mkt- I guess we are staring at a shortage + unemployment situation as well!

3 Likes