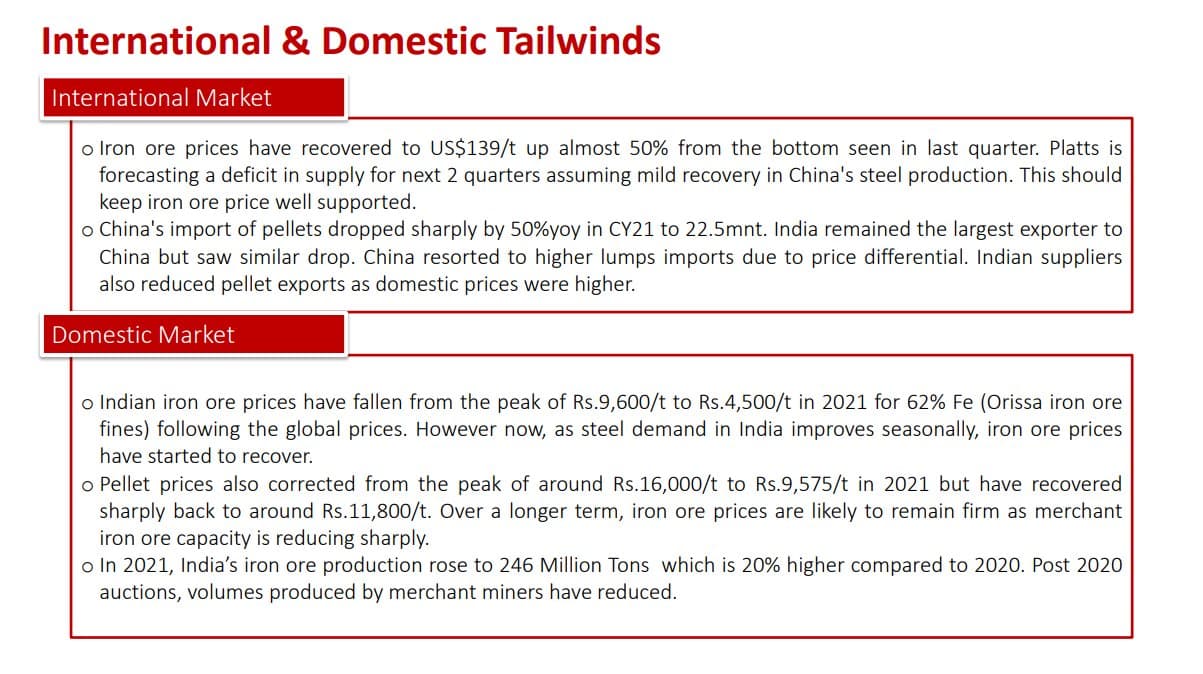

Drop in pellet prices - Pellet prices in Durgapur have decreased, as per SteelMint assessment. The current assessment for pellet (Fe 63%) stands at INR 11,600/t exw Durgapur, down INR 1,300/t compared to the last assessment of INR 12,900/t on 22 March as previous offers were not feasible.

2 Likes

4 Likes

Raipur, Chhattisgarh-based pellets producers have decreased domestic offers by INR 800/t ($11/t) from INR 12,800-13,000/t ($169-171/t) to INR 12,000-12,300/t exw ($157-162/t). Declining sponge iron prices and cheaper landed offers from Durgapur and Odisha have pulled down offers in Raipur, SteelMint notes. However, a sharp correction is unlikely on improved export sentiments.

3 Likes

Stock is in Stage 2.

Moving up in bigger Wave 3.

Currently correcting in wave ( iv ) of Wave ( I ) with in bigger Wave 3 .

Wave (v) whould follow to complete Wave ( I ) and then a correction in Wave (II). Bigger Wave 3 would be completed once we go through impulsive Wave (III), corrective Wave ( IV) , impulsive (V) …and then a correction in Wave 4 and so on.

Keep in cosideration that overall sector movement/trend is also improtant when we track a stock.

Risk Management

One can ride till it does not break 30 week moving average , but if someone really wanna stick for very long term , 40 week moving average can be used as a risk-management tool.

3 Likes

This is pretty great news and increases GPIL value by atleast 50-60% as the iron ore is the key asset it has.

9 Likes

GPIL has been added to the MSCI Index. Hopefully this will lead to market discovery apart from inflows.

Disc: Sold my holdings between 450-500 and am now gradually accumulating again ahead of Q4 results. Expecting iron ore to bounce back in H2 as China comes out of lockdowns and starts up their economy with focus on easing monetary policy and infra spending

11 Likes

Does anyone have any intelligent inputs around this?

7 Likes

If this is true , this will be a disaster for share price of Godawari

Power…

seems to be true…

3 Likes

Relax Chief, its not a such disaster, really depends on how much exports they do now v/s the incremantal increase in domestic demand, Q3’21 they’ve already said that exports have slowed and they have good domestic demand, heres a snap. So yes it will be a short term setback for all metals but not as you painted it!!..Highly export orineted cos will def be majorly negative

7 Likes

Stock hit 20% LC… It is always difficult to invest for long term in such stocks. We don’t know when Govt will change the rule. Though nothing bad as a company but govt policy definitely going to effect the margins and profitability of GPIL. Other side of picture is that there is still problem in respect of high steel price and high Iron ore price.

Once Govt. is interfering it means that Govt is having less hope that steel price will come down of its own. That is why such strict action has been taken.

4 Likes

1 Like

The whole metal pack plunged today and it so happens that GPIL’s circuit is at 20%…did not recover, unlike others that staged some minor recovery…Rs5,000-7,000/t of impact on EBITDA is very much possible on integrated steel players, while for unintegrated steel equities like JSW Steel the impact can be Rs5,000/t…but for GPIL kind of players, depends on the exports as @Tarun_1984 says above. GPIL has always been that kind of stock (it is like a mini crypto like stock)…swings wildly esp when common weaknesses happen…GPIL as a stock is always a friend of volatility !! One has to live with it

PS - no position

1 Like

Not only exports but domestic prices also come into play! Discouraging exports will flood the domestic markets driving prices down. @Rakesh_Arora has done all the math in his thread - please go through it to understand some of the impacts these duties will have on spot prices. Also there are no deadlines mentioned for these new duties so it puts the future of the entire sector in jeopardy. Companies will lose anywhere between 20% to as much as 50% of their EBITDA. And integrated players will fare worse because their costs are fixed.

Disc - Exited my entire position in this today given the circumstances.

5 Likes

Hi Manas,

Any comments on how GPIL margins and Profits will be affected after this regulation from Govt…r u still firm believer in the GPIL story?

Regards.

Jaisish

My thoughts are that Steel companies are going to appeal to Govt to reverse the decision or make some adjustment as all steel companies are going to get impacted badly. It may or may not happen. But per me, there are probability of happening it. I am relating with IRCTC where Govt has to reverse the decision. This is not same case here as Govt is doing it to reduce steel cost and inflation. But there could always be some mid or any other way.

Disc - I own the stock and added more today. Will add some more if stock falls 30-40% more

5 Likes

Funny to see the panic on this esteemed forum.

Let us breakdown GPIL-

- 20% profits are from ferro-alloys (25% if you include the new solar power plant here)

- so 25% profits have zero impact

- around 10% or so profits from billets- as far as I understand, billets are not impacted from this duty thing.

- 65% of profits are impacted in the short term for next 6 months only.

65% of profits from pellets may come down by 30%

Net impact on profits for next 6 months- 20% fall in profits.

Why 6 months?

Because duty has not been imposed on billets and many other steel products.

GPIL can build or buy a billet plant or any other plant, that converts pellets into a product on which duty is not imposed.

GPIL mining license is a 20 years call option on steel prices in India.

Duties will come and go. Govts will come and go. Many small steel companies and small pellet plants may become bankrupt and may shut down because of reduced exports.

But, cash rich GPIL would not be impacted in the long run.

Is stock value based on next 6 months profits or next 10 year profits?

Let us say, next 6 months profits.

How much will the profit fall- by 20%, as detailed above.

Let us take the most pessimistic view and say, pellet profits will fall by 40%, and net profits will fall by 30%.

Most pessimistic view gives annualised EPS of 70-75 from current 100-110 annual EPS.

7 price earning ratio for 70 annual EPS gives Rs. 490 share price. (remember GPIL is now cash rich, debt free, so it deserves 7 pe in a downcycle atleast)

Also, is the EPS of 2030 impacted by these duties put 3 days ago?

Yes, EPS in 2030 should be higher due to these duties (higher than EPS without the duties)- if anyone can explain the reasoning, it would be good for the forum!

14 Likes

How about the upcoming capex? Capital allocation outcomes are unpredictable in the future right?

I did some basic calculations, and found the following-

- Approx surplus cash with GPIL by June 2022- around 900 crores.

- Approx surplus cash with GPIL by end of current FY - around 2000 crores.

- Market cap = 4100 cr, so current EV is 3200 cr and EV by end of FY = 2000 crore only

- Net profit for FY 23 (after duty imposition) may be around 1000 cr, EBITDA of around 1300 cr (standalone EBITDA around 1050-1100 cr only, rest will come from hira ferro alloys and godawari green)

So, company is available at EV/Netprofit = 2, and EV/EBITDA =1.5 (based on FY 23 numbers)

These numbers are after duty imposition.

That’s absurdly cheap!

If we compare this to govt commodity PSUs like MOIL or commodity cos like Rain or HEG, it is way cheap!

Infact, no other company is trading this cheap in the markets!

P.S- these are pretty pessimistic EBITDA numbers. Currently, standalone annual EBITDA is 1900 crs. I have taken it at 1050 cr only. 45% cut in profits!

14 Likes