Could this indicate the end of the Commodity super cycle?

1 Like

If Chinese steel producers start ramping up production it would be good for GPIL as it is iron ore (mainly pellets) player and China is an iron ore importer. It would be bad for Steel players like JSPL, JSW, Tata steel etc.

Second, if you read the article carefully you will see that they plan in easing the clampdown on Steel production but not go back to their stance of the past. Additionally, they have removed the Export rebate and that discourages exports by Chinese steel players. From what I have read from various reports, China intends to only limit the production to Chinese consumption and not allow Chinese steel exports.

Please read this post by @Rakesh_Arora Sir.

3 Likes

Sorry, but I am a little confused - so this will not affect GPIL right?

Thanks

If China starts producing more stee, they will need more iron ore that needs to be imported as they dint have enough domestic iron ore. So, the demand for iron ore goes up and thus iron ore producers benefit.

GPIL is an iron ore producer.

4 Likes

The Management stated during the interview with CNBC-TV18 that Iron Ore prices are dependent on what happens in China. Based on my limited understanding, I think the recent news coming out of China is positive for GPIL.

Disc: Invested

5 Likes

Any views on this?

2 Likes

I don’t know how is it relevant anymore. You can clearly see their numbers and corroborate it with their cash flows and debt reduction. They have been able to execute their plans and have been able to surpass their guidance.

You trust the management when they walk the talk, and they have been doing that.

11 Likes

Total value of sale is ₹10 lakhs. Insignificant amount compared to total value of company. Any specific reason why you think this sale of shares by promoter group is important?

3 Likes

Well I felt that there would be some reason for the insider selling.

Anyways, thanks

5 Likes

sale of non core 50mw ipp solar plant for ev of 665 cr…i think mgmt had indicated around this valuation in last interview…

they had paid about 57cr to acquire 22% of this company in oct 21…implying valuing the equity at about 260cr…debt was around 350cr (320cr loan plus some wc)…so ev is about 600cr…against which they have struck deal for 665cr…

selling non core asset is a good step. the equity portion of money they receive can get used for its captive solar projects under implementation…

overall sounds like a good move…views welcome…

(please correct if there are any errors in the above numbers).

10 Likes

Divestment from non-core biz is great news! One correction, out of 322 Cr loan, 197 Cr had already been paid in January 2022. So ~540 Cr from the deal can potentially be used for upcoming solar PV capex.

11 Likes

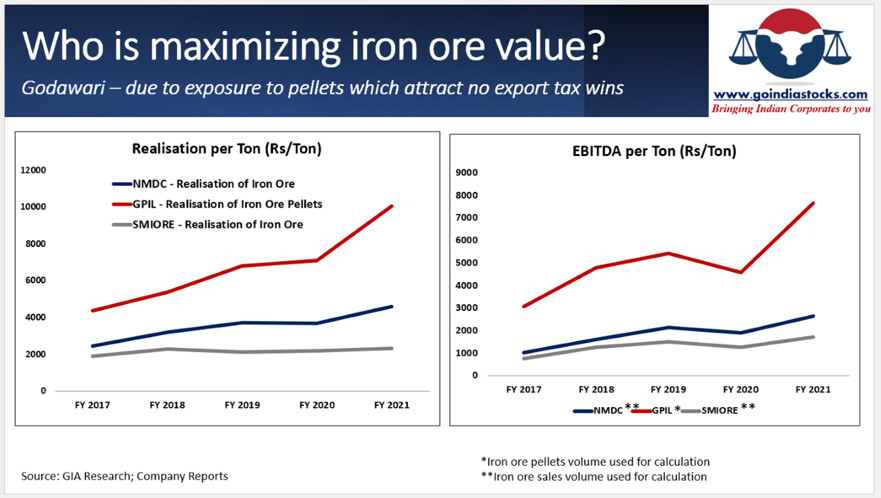

Just a comparison of 3 pure iron ore mining companies on which one maximises the realisation and margin on it’s production. GPIL stands out

Source: Counting the damages...

13 Likes

1 Like

GPIL gets another rating upgrade

5 Likes

They will be increasing stake in Hira Ferro Alloys Limited from 56.45 % to 75.66 %. Cost of acquisition around Rs 100 cr.

Also announced they have completed divestment in Godawari Green Energy Limited and have received around 352 cr from the transaction.

I am expecting a very strong Q4 with pellet realizations averaging above 12500/t. Expecting a good 520-550 crores in EBITDA pre other income. Inviting thoughts and estimates.

Disc: Invested

GPIL_21032022174044_GPILNSEBSE21032022.pdf (513.2 KB)

11 Likes