they largely import. Please note that steel is a small contributor of profits still for GPIL, it is pellets which is main driver and it doesn’t require any coal

8 Likes

Crazy increase in prices continue today.

While prices are up, costs are the same for GPIL. This should lead to higher profits.

4 Likes

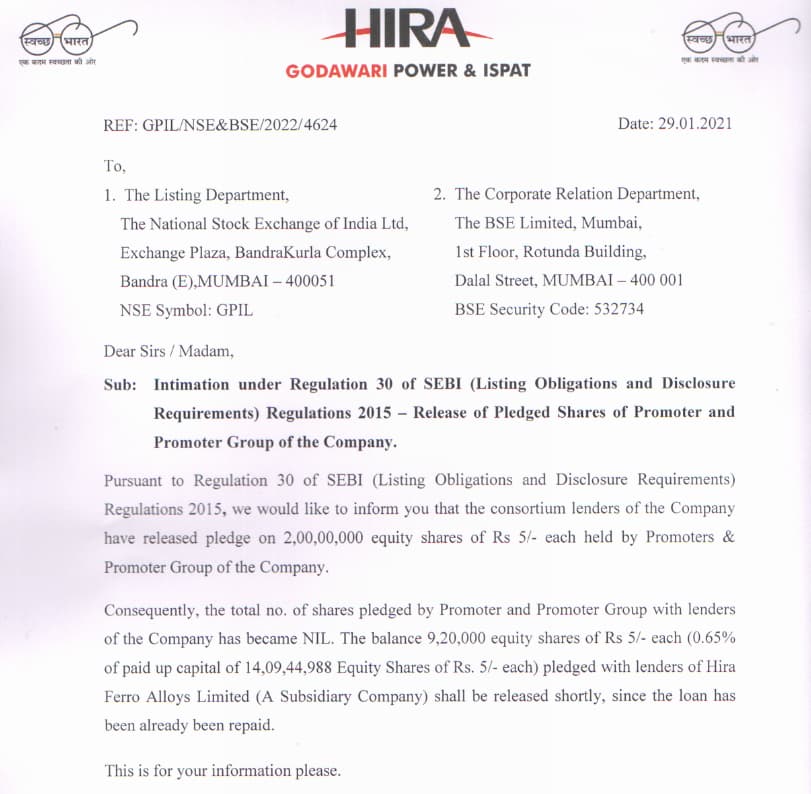

All pledged shares in GPIL are released. Good show. What a turnaround GPIL has seen in the last three years

- Debt significantly reduced

- Pledged shares released

- Dividend Payment

- And all above three happening with huge free cash generation by business

Yes, it is a cyclical business, and I am really happy that management is doing a lot of good things to make things better in this cycle.

Disc: Invested and Biased. Not a buy/sell reco.

Cheers,

Krishna

7 Likes

Vendanta results are out and their iron ore business profit has dropped from 582cr to 383 cr …QoQ

2 Likes

Vedanta’s iron ore business has been facing a lot of problems as a lot of its mine are being closed down and such. Their Goa mine is also closed…

GPIL mainly sells pellets. The prices of pellets have been quite high In the pas quarter. Obviously, iron ore prices have fallen substantially from the past quarters. The fall in the prices have already been discounted by the market.

In my view, the market has discounted has it too negatively.

3 Likes

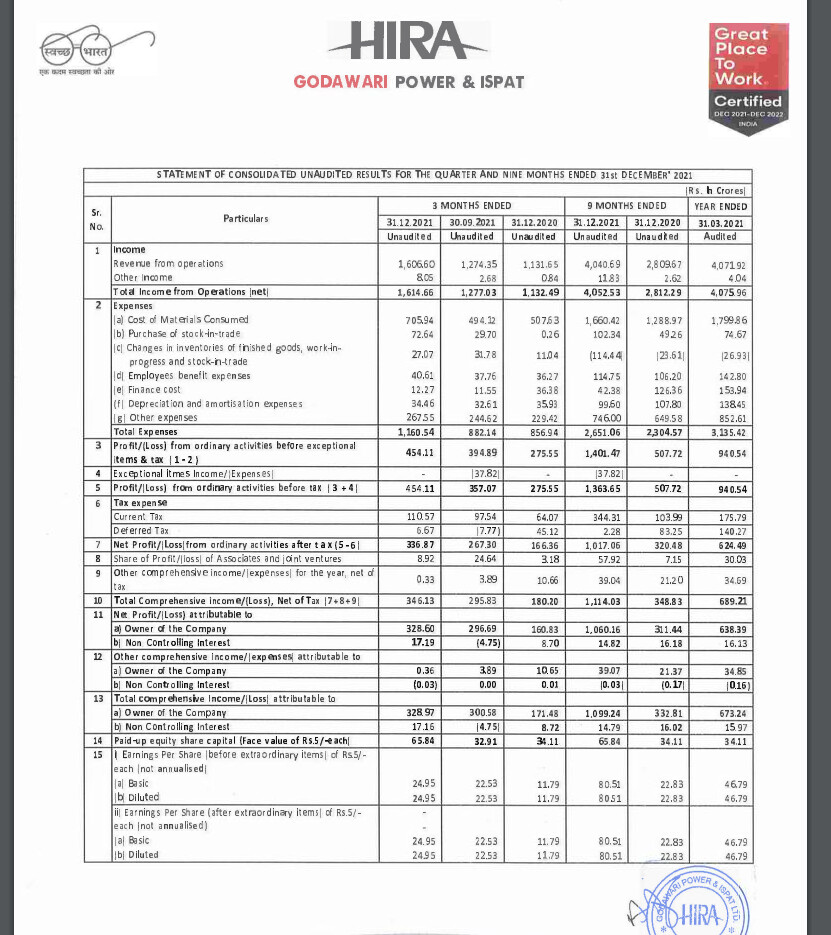

I know many people were expecting profits to go down because pellet prices have fallen.

But, I told many times on this thread that volume increase will make up for the fall in pellet price, and annualised EPS is 100 (this quarter EPS is 25, what a bang on target!!! My estimate = actual EPS)

Basically, it is at PE of 3, debt free, plus mega capex! (expected 25% CAGR growth for 3-4 yrs because of big steel plant)

23 Likes

Hi sir, indeed really great results.

I wanted to know your view on NMDC vis a vis GPIL. On the basis of Q2 results, NMDC is available at a PE of 4 and GPIL at 3.5.

In addition to this the NMDC steel plant is goin to get commissioned within this quarter. Today, the NINL plant of 1 MT capacity was sold for 12000 crs. and thus the NMDC which is of 3 MT (with latest technology) would come out to be 36000 crs. which is nearly 90% of NMDCs current market cap. Can you please share your views on this.

And also please share what in your view could be the valuation of the NMDC plant.

1 Like

NINL plant has Iron ore MINES. Thats the key. that’s why Tata bought it for 12k crore.

Basically, Tata has paid the premium for the mines and not the plant.

NMDC - I have explained in a detailed post on commodity and cyclical thread. Please find it.

12 Likes

Thank you sir, Found your comparison of GPIL and NMDC. Wanted to know about the value of the steel plant that NMDC is going to commision soon?

Good call and consistent work, Manas!

I wasn’t expecting such good nos given the fall in iron ore prices in recent times. This is super execution and performance from the company.

Disc: Continue to be invested in family and client accounts.

18 Likes

Budget_2022-23_SteelMint_Report.pdf (3.0 MB)

Budget takeaways on the iron and steel sector By Steelmint.

2 Likes

1 Like

Don’t believe this is true. Even if it is, it is bullish iron ore.

6 Likes

Could be for long term, but for short term dont you think that this will have a negative effect?

No, not on GPIL. It sells pellets and iron ore which is sold to steel plants. China is the biggest iron ore consumer. So, if their production increases, iron ore prices increase and thus benefitting GPIL.

5 Likes

No one is expecting China’s steel companies to turn carbon neutral even by 2030. The alternative technology is not yet tried and tested and would require billions of dollars of investment. That’s why this post doesn’t make sense longer term or short term. Chinese government has curtailed production through yearly targets and these targets are kept depending on the domestic economic growth being planned. In any case, China has been trying to curb export of carbon intensive materials and steel falls under that. They have taken explicit measures to reduce exports. And steel exports have been falling since 2015. So don’t see any change in view. See comment from Tata Steel on China’s export outlook in Q3 conf call. Same views echoed

11 Likes

China’s steel production is 90% from blast furnace (BF-BOF) and 10% from electric arc furnace. Carbon emission intensity from BF-BOF is way higher than EAF. Even United States steel corporation is guiding for carbon neutrality by 2050. US uses only 30% of BF-BOF for steel making. Doesn’t look like a reasonable target.

4 Likes

Can you please share the link?

2 Likes