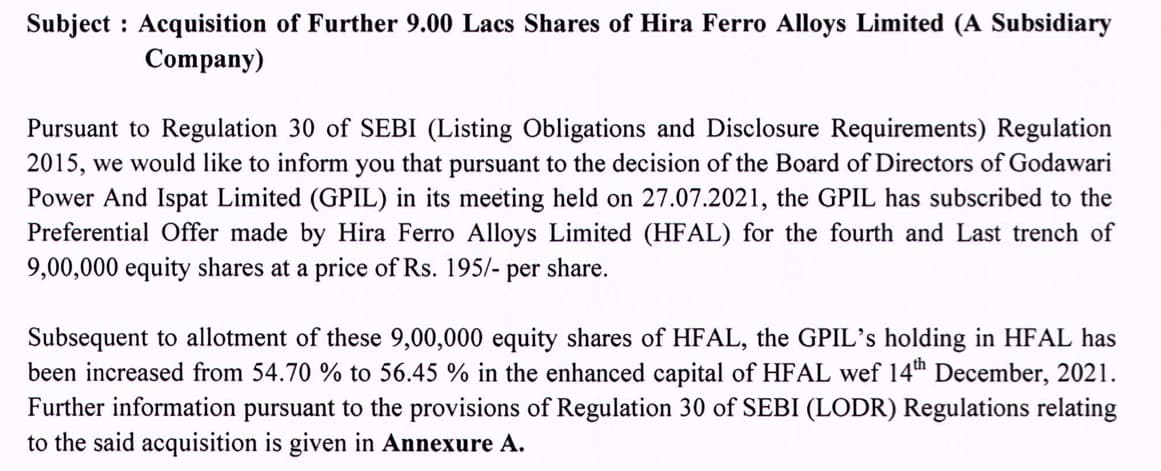

There is clear corporate governance issue with this company. The company is indirectly paying cash to Promoter. It is buying Hira ferro alloys issued preferential shares.

Why not buying Hira ferro alloys existing equity rather than preferential shares.

Why not merging entire Hira ferro alloys (same promoter) 100% equity using fresh GPIL equity (share swap raito). why keeping as a subsidery and holding only 56% in Hira ferro alloys. There is high chance that GPIL will pay more cash (currently valued at 195 rs per share of hira ferro alloys) to buy Hira ferro equity.

If they buy shares of Hira ferro- they will be transferring money from company books to personal books.

They have subscribed to preferential issue- This transfers money to Hira books - which will be used to set up power plant- which will increase profit substantially- and that profit will be added to GPIL profits- since Hira is now subsidiary of GPIL. Money hasn’t gone to promoters at all here.

They have done 2nd instead of 1st, and that is perfectly allright.

“The company has signed a PPA with NTPC Vidyut Vyapar Nigam Limited (NVVN) for sale of power from the 50MW Power

Plant under JNNSM of GoI. The tariff is fixed at Rs.12.20 per unit for a period of 25 years. Due to this long term agreement”

Is gov going to honour this … When new PPAs are being signed at 2.50 Rp per unit … ?

That’s what a PPA means…if NTPC stops honoring the PPAs, why will anyone build a plant based on NTPC PPA terms in the future?

Has NTPC dishonored its PPA with anyone else?

NTPC hasn’t stopped any PPA before completion of 25 years of plant running so far. If it does to any co in the future, that means it is a banana company, and we are a banana republic.

“The Andhra Pradesh government is currently in a legal battle with renewable energy producers with the aim of renegotiating contracted power tariffs and the Punjab Assembly has passed a Bill to renegotiate tariffs under existing PPAs. Solar power tariffs have fallen drastically over the past 5 years leading to power purchased under earlier solar PPAs being significantly more expensive than prices under more recent PPAs.”

State govs are clearly not honouring them…

State govts can do anything they want. They can give free electricity, water, laptops, alcohol.

That’s why state run institutional bonds have a very high interest yield in India. Individual states have no reliability. Any politician can announce any random thing overnight. (demonetisation is also a good example)

However, NTPC is a listed company, and has to honor its agreements. If NTPC stopped honoring PPAs, then lakhs of crores worth power plants will turn into NPAs overnight.

A big chunk of PPAs were signed before 2011- and NTPC has to honor them, unless it wants to become a banana company like our politician run state govts.

recently gov was willing to steal 50% of revenue from IRCTC overnight… So i would not be so confident when dealing with gov… If interest rates raise NTPC which itself is drowing in debt can run into serious problems. Do you happen to know what share of GPIL revenue comes from this PPA?

The PPAs can be exited by NTPC after the 25 yr period ends.

Fortunately, we are not a banana republic yet. have to follow the laws and the agreements.

IRCTC revenue sharing was mentioned in the DRHP prospectus. and revenue sharing happened earlier too. they keep changing the share with time.

The clarification comes after the power industry regulator allowed BSES Delhi distribution companies - BSES Rajdhani Power Ltd (BRPL) and BSES Yamuna Power Ltd (BYPL) - to exit the PPA.

There are many fine prints in PPA and you need to go through it before drawing any conclusion. NTPC would try to exploit any such option,if available in the PPA, which can prevent them from buying electricity at a rate higher then the prevailing rates.

Hypothetically, let us say, it happens! @Ysr does it make a difference at all? Even 5% difference in net profit?

What was GGEL contribution to GPIL profits in last 2 quarters?

GGEL is not an imp part of business and GPIL was planning to sell GGEL to external investors for 600-650 crores just a few months back.

GPIL is primarily only an iron ore, pellet, billet and specialty steel (future capex) business.

And, there is huge jump in billet, sponge iron ore price today.

The billet price today is higher than average of any of the best quarter in last 12 months. Check for yourself.