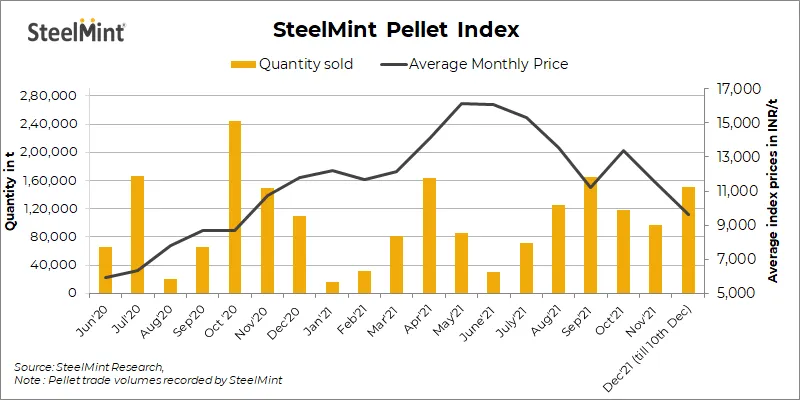

Pellet prices are now (as of today) at 12500/ton, even after the 60% fall in international iron ore prices.

This dissociation between Indian and International prices have started post the iron ore mining auction change.

Earlier Indian prices were at huge discount to International prices. Now, that discount has reduced to minimal!

“So, you can expect close to about Rs. 100 crore additional EBITDA going

forward from the solar”

“The total EBITDA of Hira Ferro Alloys for the

last quarter was Rs. 47.5”

These two will add additional 150-200 crore EBITDA/year (Hira will be added in current quarter, solar will come next year).

NMDC is saying domestic demand good enough for prices to remain stable.

Doesn’t intend to reduce prices despite cut in international prices.

If NMDC doesn’t cut prices, then it will keep the prices stable overall.

State-owned mining company NMDC on Tuesday slashed prices of lump ore. NMDC has revised the rates of lump ore or higher grade ore from Rs 5950 to Rs 5,200 a tonne which is down by almost 13% compared to last month.

How does one consume this information?

We know iron ore & finished products like palette prices are not related for the time being, so the drop in iron ore price is a sort of opportunity loss for Godawari Ispat, as Godawari has captive ores & others might be getting them for higher prices, but since prices have lowered, others are getting it cheaper, so their margins would be expanding, so relatively Godwari’s margin would be declining?

But in real terms there is no effect of iron ore price on Godawari, right?

We have to see what GPIL does with Iron Ore… They are converting Iron ore to pellets. Pellets are used to make spong iron and billets which are finally sold in the market. Lower iron ore price will also reduce the price of final products so GPIL is also going to be affected with that .

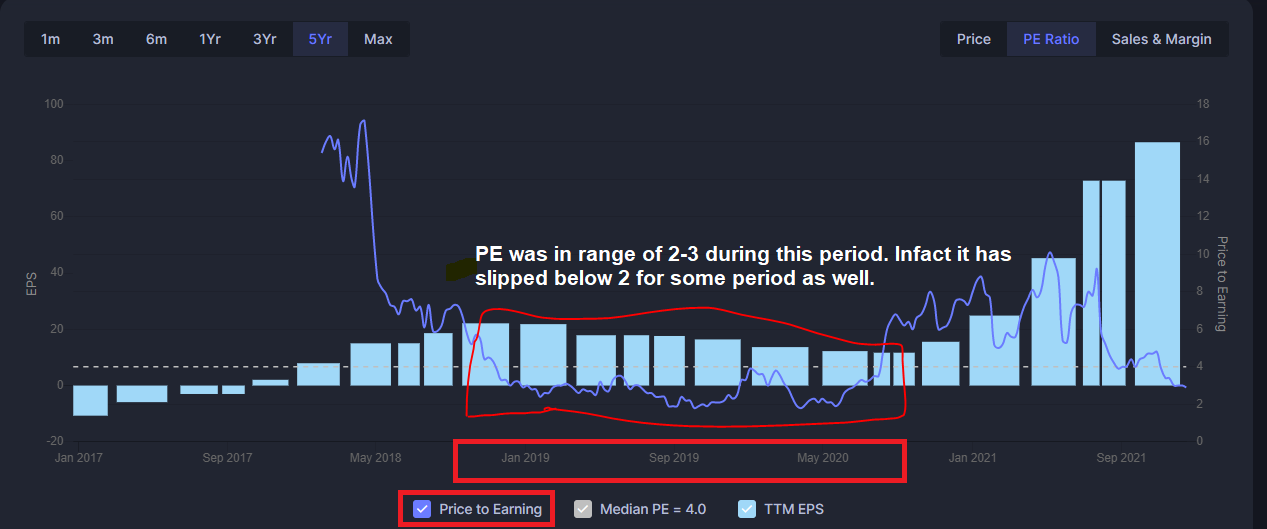

Historically, Avg PE for last 3 years is around 3.4. Inspite of such a low PE valuation, there are no buyers currently

Should we really consider this low PE as an indicator?

Historically, the debt was very high, there was no capex too. Also, the iron ore mining auction rules changed in 2020. Interest costs were very high earlier, now it will be zero.

Whenever it touched 2 PE in the past- it went up 5-10x in next 1-2 yrs. The stock is 12.5x from March 2020 lows, when it went at 2 PE. So, how is it 12.5x without any buyers???

See, one major reason that they are given so low multiples is because of the volatility of their earnings. Hence, they are valued on the basis of sustainable EBIDTA, rather than the immediate one.

The good thing with GPIL is that they are doing CAPEX which will increase their sustainable EBIDTA. The most recent step that will soon come on stream in the next year is the setting up of the Solar power plant for its subsidiary HFAL and for itself. This according to the last Concall will lead to the addition of 100 crores of EBIDTA. And this is will not fluctuate.

Increase in iron ore price (as dollar price increases and rupee continues to depreciate)

Though iron ore price increased in the recent past, however overall export volumes are low for this quarter (Source: Steelmint). Not sure how this will get translated to earnings for GPIL (for the current quarter).

this is because domestic price in October was too good. Pellet for oct was at 13400 and Billet 45-46000, the highest ever. They would have made a killing in domestic mkts in October, so why would they export?