Owning GPIL is like owning a 25 years call option on iron ore price. As iron ore price will keep increasing with inflation over next 2 decades, the profits will increase dramatically.

Both are debt free. While, Shyam is expanding capacity, GPIL is also nearly doubling billet capacity within 3 months, and putting a big solar plant that will add 100 cr EBITDA. Over and above that, a big specialty steel plant in next 3 years. plus Hira ferro EBITDA to be added which will become a subsidiary from now on.

I was going through the GPIL technical chart, and I found a pattern which occurs every year/few years. It seems that currently the price is at a peak, after which it may fall around 60-80% and then sky rocket. This is the pattern I have seen in the past. This pattern may not be discontinued due to the changes in some fundamental factors like debt. Feel free to criticize and give me feedback as the best teacher is an honest critic!

This is to be expected I’d say. This Q domestic prices were higher than earlier so GPIL would have sold more domestic than export probably. Export revenues dropping little bit isn’t necessarily a concern. An estimate of domestic vs export ratio would tell if this drop is significant.

not really, today JSW steel reported results with decent fall in margins- because of rise in iron ore price and because of expensive coking coal.

If you don’t own the raw material, your margins will go down.

Dear Manas, JSW’s margins were down for the most part because of rise in coal price. Iron ore price movement actually helped them, it was trending down.

I quote from JSW’s press release: “The EBITDA margin was lower QoQ primarily due to elevated prices of coking coal and higher power cost. Domestic iron ore prices during the Quarter softened in-line with global indices, partly offsetting the cost increase”.

Exactly, GPIL uses majority of power from captive sources, and to the best of my knowledge, I don’t think that cooking coal is such a big cost.

The reason for this is that I haven’t seen them mention coming call either in there Presentation or their Concall. On the other hand if you check the Q2 concalls of Steel players, there are continuous mentions of Coking Coal.

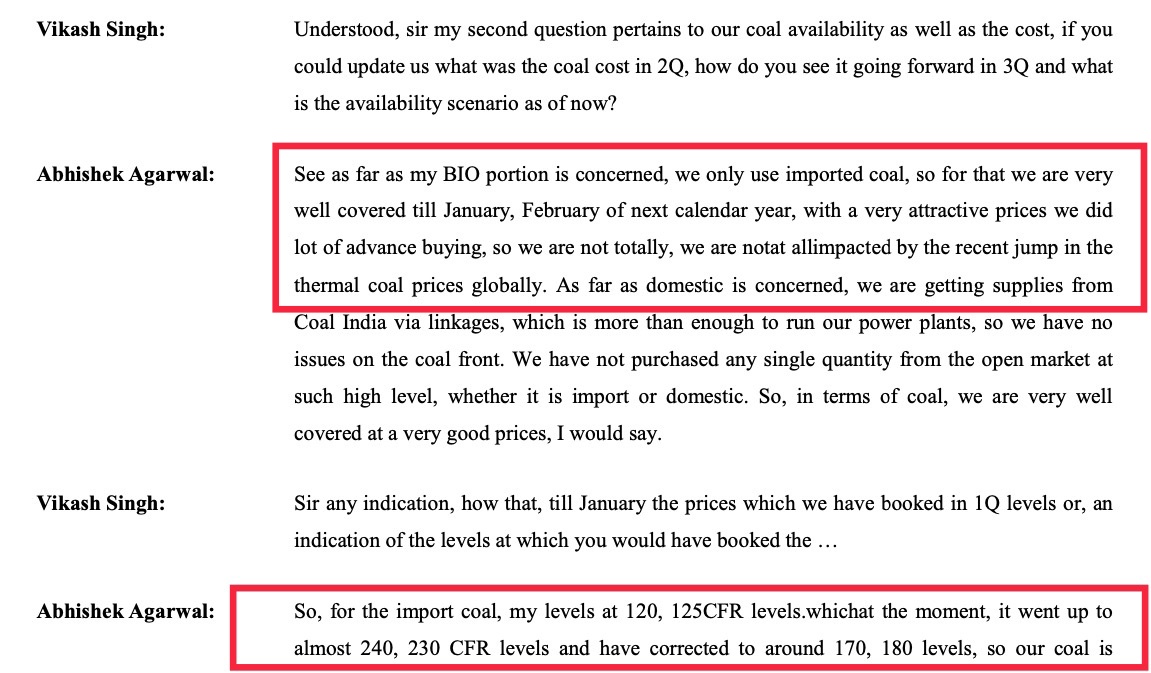

Now, coming to the coal part. If you look at the Concall excerpt attached below, they had already procured coal for up to Feb. Hence, they won’t suffer the margin contraction from this point of view.